Beyond the Hype: What Defines a True Global Lithium Heavyweight?

People don't think about this enough: digging lithium out of the earth is only a fraction of the battle. The thing is, raw spodumene ore or unrefined salar brine is essentially useless to a battery manufacturer building cells for a high-performance electric vehicle. It needs to be cooked, washed, and chemically transformed into ultra-pure molecules. We are talking about strict battery-grade specifications where even a few parts per billion of iron contamination can cause an entire production run of cells to short-circuit or explode.

The Extraction Versus Refining Divide

Where it gets tricky is looking at raw volume versus chemical sophistication. A company can mine millions of tons of rock in Western Australia, yet remain entirely dependent on third-party chemical facilities in mainland China to convert that rock into lithium hydroxide. This reality changes everything when calculating true market dominance. True heavyweights are vertically integrated. They possess the extraction assets—whether that means pumping ancient brines from beneath South American salt flats or blasting pegmatite rocks—and pair them with downstream conversion plants capable of turning out white powder that meets the microscopic tolerances of automakers.

The Consolidation Wave of 2025 and 2026

Market dynamics have shifted brutally over the last few years. Following a devastating price correction where lithium carbonate plunged from historic highs, the industry underwent a massive shakeup that purged over-leveraged junior developers. But out of that carnage came a fierce wave of corporate consolidation. The most glaring example is Rio Tinto's colossal US$6.7 billion all-cash acquisition of Arcadium Lithium, a mega-transaction that instantly swallowed up assets across Argentina, Canada, and Australia. In short, the barrier to entry has become astronomically high, leaving the playground entirely to the deep-pocketed elite.

The Upstream Blueprint: How Brine Exploitation and Hard-Rock Mining Split the Market

Geology dictates corporate strategy in this game, splitting the top producers into two distinct operational camps. You either pump liquid from the desert or you crush granite in a mill. Honestly, it's unclear which side will ultimately win the long-term cost curve debate, as both methods carry intense, distinct geopolitical and environmental liabilities that keep corporate executives awake at night.

The low-cost crown belongs unconditionally to South American brine operations. This brings us to the famous Lithium Triangle spanning Chile, Argentina, and Bolivia. Here, companies pump mineral-rich saltwater from subterranean aquifers into immense surface evaporation ponds. The sun does most of the heavy lifting over a period of 18 months. As a result, operations situated on the Salar de Atacama enjoy production costs that are roughly half of what it takes to process rock. Yet, the issue remains that these operations are incredibly water-intensive in some of the aridest places on Earth, creating friction with local indigenous communities and regulatory bodies.

The Spodumene Counter-Attack

But what if you cannot wait two years for the sun to evaporate your brine? Enter hard-rock mining, dominated heavily by Western Australia's pegmatite deposits. Miners extract a lithium-bearing mineral called spodumene through traditional open-pit mining. It is fast, predictable, and capital-intensive. The Greenbushes mine in Western Australia stands as the absolute gold standard of this method, yielding a high-grade concentrate that is shipped overseas. And because the industrial processing of hard rock bypasses the long evaporation phase, it allows companies to scale up output rapidly when market demand spikes unexpectedly, though it requires a massive amount of fossil-fueled energy to bake the stones at temperatures exceeding 1,000 degrees Celsius during initial refining stages.

The Geopolitical Chessboard: Why Refining Capacity Trumps Raw Reserves

Let us look at the numbers cleanly. While Australia digs up the most raw tonnage and Chile sits on the largest accessible economic reserves, China controls over 50 percent of the global capacity to refine those raw materials into battery-grade chemicals. That single statistic explains the quiet panic echoing through Western boardrooms and government offices. It is an asymmetric distribution of industrial power that makes Western car manufacturers deeply uncomfortable.

The Western Firewall Strategy

To push back, the United States and Europe have thrown billions of dollars at creating localized supply chains. The 2022 Inflation Reduction Act completely rewrote the rules of the game by tying consumer EV tax credits directly to the sourcing of battery minerals from countries with which the US has a free trade agreement. But we're far from self-sufficiency. Building a mine in North America or Europe takes an average of seven to ten years due to stringent environmental permitting and local opposition. Consequently, Western legacy producers have been forced to aggressively expand their domestic footprints to capture the "security of supply" premium that automakers are suddenly willing to pay.

The East Asian Refining Stronghold

Meanwhile, Asian chemical giants continue to enjoy massive structural advantages. Their processing hubs are deeply integrated with existing cathode and battery cell gigafactories, minimizing logistics costs and supply chain friction. Because they built these facilities a decade ago—back when Western mining executives were still dismissing electric vehicles as a niche hobby for environmentalists—their capital costs are entirely amortized. This allows them to withstand prolonged periods of depressed commodity prices that would completely bankrupt an emerging Western developer trying to build a refinery from scratch in a high-cost jurisdiction.

Diverging Technical Pathways: Lithium Carbonate vs. Lithium Hydroxide

The battle for corporate supremacy is also fought at the molecular level. When processing lithium, a company must choose whether to optimize its facilities for lithium carbonate or lithium hydroxide production. This is not just a matter of chemical preference; it determines exactly which segment of the automotive market a company can serve.

Lithium carbonate is the traditional workhorse of the industry. It is the natural output of most brine operations and serves as the foundational chemical for Lithium Iron Phosphate (LFP) batteries. These batteries are cheaper, exceptionally durable, and do not require expensive cobalt or nickel. Because Chinese automakers have mastered LFP technology for mass-market, budget-friendly electric vehicles, global demand for pure carbonate has remained incredibly resilient. If a producer wants to feed the high-volume, mass-adoption EV wave, carbonate is the product of choice.

The High-Nickel Hydroxide Frontier

Yet, the landscape changes entirely when you shift toward premium, long-range electric vehicles favored by Western consumers. These vehicles rely on high-nickel chemistries like Nickel-Manganese-Cobalt (NMC 811). The problem is that synthesizing these specific cathodes requires a lower thermal processing threshold, which makes lithium carbonate chemically incompatible with the manufacturing process. You must use lithium hydroxide instead. Hard-rock spodumene miners have a natural advantage here, as converting spodumene concentrate directly into hydroxide is often more economically viable than doing so from brine. It is a premium product that commands a higher margin, though the chemical itself has a notorious shelf-life problem—absorbing ambient carbon dioxide if left exposed to the air—meaning it cannot be easily hoarded or stored in warehouse reserves for extended periods without degrading.

Common Misconceptions Blocking Your View

The Illusion of the Pure-Play Gigantic

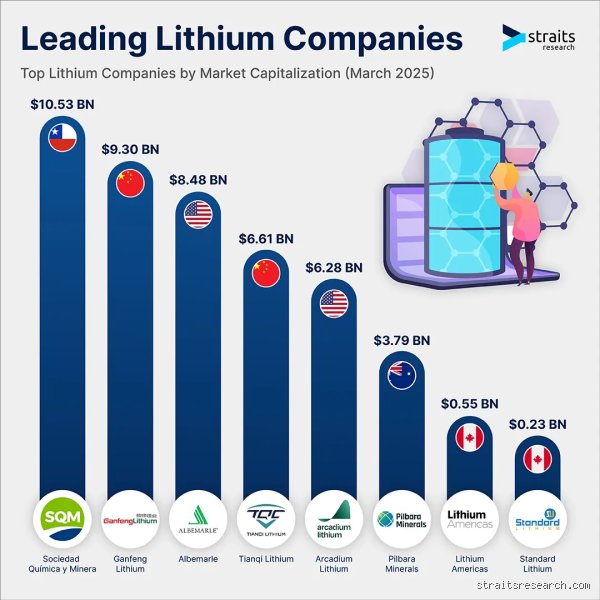

You probably think investing in the titans means betting solely on white petroleum. The problem is, the market frequently conflates mining footprint with pure commodity exposure. Take a giant like Albemarle, which dominates the global output metrics alongside peers like SQM or Ganfeng. But let's be clear: these behemoths operate complex, multi-tiered chemical empires rather than simple extraction pits. They process specialty catalysts and bromine alongside battery-grade salts. If you purchase shares expecting a direct correlation to raw spodumene spot prices, you will get blindsided by legacy industrial supply chain cycles. Because a corporation is among the top 5 lithium companies by volume does not mean its balance sheet mirrors the volatile whims of London Metal Exchange futures.

The Brine Versus Hard-Rock Binary Trap

Wall Street loves a simple dichotomy, pitting South American salar evaporation against Australian pegmatite mining. Investors treat this like a ideological war. Yet, the operational reality behaves much more fluidly. Hard-rock proponents mock the two-year lead times of Chilean brine pools, claiming they lack the agility to meet sudden automotive demand spikes. Conversely, brine defenders point to the punishing capital expenditure required to crush hard spodumene ore into submission. Who wins? Neither on their own. The market increasingly rewards hybrid giants that straddle both geologies to hedge geographic risk. Except that analysts still write reports as if these extraction methodologies exist in completely isolated ecosystems.

The Recycling Myth Disrupting Near-Term Math

Will urban mining render traditional extraction obsolete by next Tuesday? Absolutely not. Enthusiasts look at closed-loop battery recycling initiatives and assume primary extraction will soon collapse into irrelevance. The math simply fails to compute. Even if we miraculously reclaimed every single spent cell from early-generation electric vehicles today, the aggregate volume would satisfy less than 15 percent of the projected 2030 global manufacturing demand. (And that is assuming perfect metallurgical recovery efficiency, which remains a pipe dream). Scrap cannot fill an empty pipeline when total EV production is scaling exponentially.

The Geopolitical Monopoly No One Talks About

The Midstream Bottleneck and Tollbooth Economics

Where is the real power held? You might focus on where the physical rock gets pulled from the dirt, whether that is the Salar de Atacama or Western Australia. That is a mistake. The true chokehold lies in the chemical conversion capacity, a domain where Chinese refining infrastructure remains functionally unchallenged. A company can mine millions of tons of raw concentrate, but it must ultimately ship that material to specialized facilities to create high-purity carbonate or hydroxide. As a result: Western nations find themselves scrambling to construct localized supply chains, realizing that owning the mine means nothing if you lack the toxic, energy-intensive chemical plants required to finish the job. If you want to identify who the top 5 lithium companies really are, stop looking at mining claims. Look at who controls the crystallization reactors.

Expert Advice: Follow the Off-Take Integration

Stop hunting for micro-cap juniors boasting about unproven deposits in remote jurisdictions. Instead, we must monitor the binding off-take agreements signed by Tier-1 automotive manufacturers. When an automotive behemoth secures a direct equity stake or a ten-year supply guarantee with an established producer, they are validating that asset's chemical viability. That is your buy signal. The market favors integrated entities that manage the entire pipeline from raw brine extraction to battery-grade precursor chemicals, bypassing traditional commodity brokers entirely.

Frequently Asked Questions

Which geographic regions currently dominate global production?

The vast majority of global extraction concentrates within a handful of geopolitically diverse territories led by Australia, Chile, and China. In recent market assessments, Australia secured its position as the top producer by extracting over 86,000 metric tons of content, primarily from robust hard-rock spodumene operations. Chile followed closely, leveraging its low-cost brine reserves in the Atacama desert to yield approximately 44,000 metric tons. Meanwhile, China maintains a dual advantage by producing roughly 17,000 metric tons domestically while aggressively securing equity stakes in African and South American assets. This geographic concentration creates a fragile supply chain vulnerable to localized regulatory shifts and trade disputes.

How does the rise of sodium-ion batteries impact the top 5 lithium companies?

Sodium-ion alternatives represent a viable alternative for stationary energy storage and low-range urban vehicles, but they pose no immediate existential threat to high-performance mining giants. The underlying physics dictates that sodium possesses a significantly lower energy density than its lighter counterpart, making it bulky for long-range automotive applications. Consequently, established chemical producers view sodium as a welcome relief valve for the lower-end market rather than a competitor. This diversification allows premium grade material to be reserved exclusively for high-margin, long-range electric vehicles. The issue remains one of market segmentation rather than outright displacement.

What environmental regulations present the greatest risk to future supply?

Stringent environmental oversight centers primarily on water scarcity in arid regions and the carbon footprint of heavy industrial processing. In the South American Lithium Triangle, communities frequently challenge the massive water evaporation rates required by brine operations, which can divert critical resources from local water tables. European markets are simultaneously introducing strict battery passports that mandate full traceability of carbon emissions from the mine site to the assembly line. Hard-rock facilities face intense scrutiny regarding the fossil-fuel energy required to roast spodumene at temperatures exceeding 1000 degrees Celsius. Producers failing to adopt renewable energy or direct extraction technologies risk losing their preferred supplier status with major automakers.

Beyond the Hype: A Clear-Eyed Verdict

The global transition away from fossil fuels is locked in, but the financial trajectory of the extraction sector will be anything but smooth. We are witnessing a brutal consolidation phase where under-capitalized juniors vanish while diversified chemical conglomerates solidify their dominance. Do not get blinded by temporary spot price collapses or sensationalized headlines about alternative chemistries. The modern industrial complex requires unprecedented volumes of high-purity battery materials, and a select few entities possess the technical expertise to deliver them at scale. Which explains why investing in this space requires looking past raw tonnage to evaluate geopolitical insulation and processing sovereignty. In short, stop treating this sector like a traditional speculative mining rush; it is an industrial chemical arms race where the winners take everything.