Beyond the Hype: Defining the True Geopolitical Footprint of the White Gold Rush

Lithium is everywhere in the financial headlines, yet people don't think about this enough: it is not actually scarce. The issue remains that extracting it at scale, to a degree of purity that won't cause an electric vehicle battery to catch fire, is an agonizingly slow and capital-intensive nightmare. We are dealing with two entirely different beasts when it comes to extraction methodologies.

Brine Versus Hard Rock Extraction

On one side of the ledger, you have the subterranean brine deposits, predominantly found beneath the surreal, sun-baked salt flats of the South American Lithium Triangle, which encompasses Chile, Argentina, and Bolivia. Here, liquid gold is pumped to the surface into gargantuan evaporation ponds. The sun does the heavy lifting over eighteen months, leaving behind a concentrated sludge. Except that this process is heavily dependent on weather patterns. For instance, heavy rainfall can throw off evaporation rates entirely, disrupting production timelines. On the flip side of the coin lies hard-rock mining, chiefly spodumene ore extraction in Western Australia. It is faster but brutally expensive, requiring traditional open-pit mining, crushing, and intensive chemical roasting. Which explains why the market is so volatile; you are constantly balancing the turtle-paced, weather-dependent brine operations against the high-octane, carbon-heavy hard rock refineries.

The Realities of Refining Purity

Where it gets tricky is the refining stage. Mining the stuff is only half the battle. Converting raw spodumene or technical-grade carbonate into battery-grade lithium hydroxide or high-purity lithium carbonate requires precision chemical engineering. If a refinery allows even microscopic traces of iron or sodium to slip through, the entire batch is useless for tier-one automotive manufacturers. Honestly, it's unclear to many casual observers why a country can sit on massive reserves and still produce next to nothing. It is because building the chemical infrastructure to achieve 99.5% purity takes years and billions of dollars. That changes everything when you look at market control. It is not about who has the rocks; it is about who has the factories.

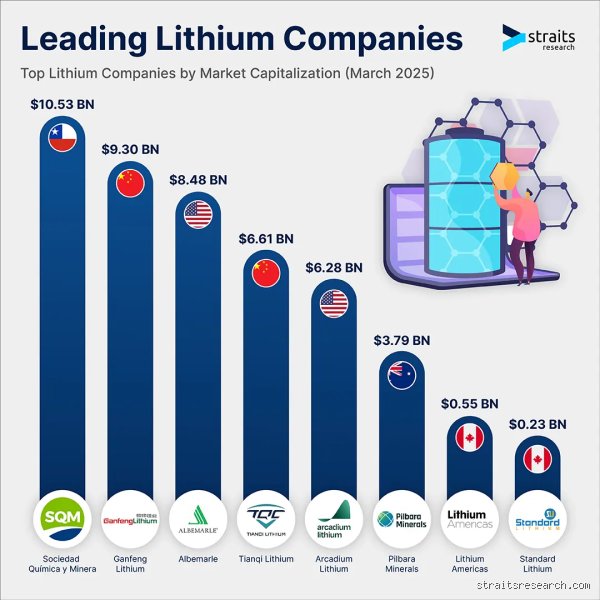

The Undisputed Kingpins: Inside the Top Corporate Extractors

The corporate hierarchy at the top of this food chain has morphed from a loose collection of industrial chemical companies into a hyper-aggressive oligopoly. These entities do not just dig holes; they control joint ventures across multiple continents, weaving a web of ownership that makes true independence a myth in this sector.

Albemarle Corporation: The American Heavyweight

Operating out of Charlotte, North Carolina, Albemarle Corporation sits comfortably at the apex of global production, commanding roughly 19% of the global market share. This company is a masterclass in geographic diversification. They do not rely on a single jurisdiction. Instead, Albemarle operates the ultra-pure Salar de Atacama brine operations in Chile while simultaneously holding a massive 49% stake in the legendary Greenbushes hard-rock mine in Western Australia. Talk about covering your bases. To process this raw material, they have constructed a sprawling web of conversion plants across China, Europe, and the United States, including their highly advanced facility in Kings Mountain. They are the primary supplier for legacy automotive suppliers, feeding battery cells directly to entities like Panasonic. By balancing low-cost Chilean brine with high-volume Australian spodumene, Albemarle has insulated itself from localized political shocks, though they remain heavily exposed to the broader commodity price swings that characterize this volatile market.

SQM: Chile’s Brine Behemoth

Then we have Sociedad Química y Minera de Chile, universally known as SQM. Based in Santiago, they control the richest lithium brine deposit on the planet in the Atacama Desert. Their cost structure is the envy of the entire mining world because the Chilean sun evaporates their brine at an astonishing rate. Yet, their corporate structure is an absolute soap opera of competing geopolitical interests. Did you know that China's Tianqi Lithium actually owns a massive 22% stake in SQM? That reality creates an incredibly tense dynamic, especially as Western governments push for supply chains completely decoupled from Beijing. Furthermore, SQM has been forced to navigate Chile's shifting political landscape, leading to a monumental joint venture with state-owned copper giant Codelco to secure their operating leases through 2060. They are aiming for an annual production capacity of 240,000 metric tons of lithium carbonate equivalents, making them an indispensable pillar of global supply, even if they have to share the driver's seat with the Chilean government.

Ganfeng Lithium: China’s Integrated Powerhouse

If Albemarle is the king of extraction, Ganfeng Lithium is the emperor of the supply chain. Based in Jiangxi, China, Ganfeng is completely vertically integrated. They do not just mine; they refine, they manufacture battery cells, and they recycle them. I took a look at their asset portfolio recently, and it is staggering. They have bought their way into the Goulamina mine in Mali, brine projects in Argentina, and hard-rock deposits in Australia. They are targeting an eye-popping compound capacity of 300,000 tonnes of lithium carbonate equivalent. Because they supply premium lithium hydroxide directly to Tesla and BMW, their operational health directly impacts the production schedules of global electric vehicle assembly lines. They represent China's dominant strategy: secure the raw material at the source, process it domestically, and sell the high-value components back to the rest of the world.

The Aggressive Contenders: Shifting Alliances and Consolidation

The boundary lines between the top tiers of production are constantly shifting, driven by a frantic wave of mergers, acquisitions, and unexpected corporate pivots that rewrite the leaderboard every few quarters.

Tianqi Lithium and the Greenbushes Nexus

Chengdu-based Tianqi Lithium is another Chinese colossus, but their crown jewel sits thousands of miles away in Western Australia. Through a joint venture with Albemarle, Tianqi controls the Kwinana refinery and the massive Greenbushes mine, which happens to be the highest-grade hard-rock lithium deposit in existence. This brings us to a critical nuance: while Australia produces over 50% of the world's raw lithium, a staggering portion of that material is spoken for by Chinese capital before it even leaves the port. Tianqi’s aggressive expansion strategy nearly bankrupted them during the market crash a few years back, yet they managed to hold onto their core assets. They have proven that in this game, raw volume and resource grade trump short-term balance sheet anxieties every single time.

Rio Tinto’s Massive Structural Leap

The newest entrant to the top tier did not get there by drilling new holes; they simply bought the competition. Mining supermajor Rio Tinto completely transformed the industry landscape by executing a massive, all-cash acquisition of Arcadium Lithium for 6.7 billion dollars. This single move absorbed the combined assets of Livent and Allkem, instantly giving Rio Tinto a pre-packaged lithium empire. As a result: Rio Tinto now commands premier brine operations at the Salar del Hombre Muerto in Argentina alongside spodumene assets in Canada. They are aggressively deploying billions to build out the Rincon brine project, signaling that the traditional diversified mining giants are no longer content to leave the battery space to specialty chemical companies. This structural leap changes the dynamics of the entire market, bringing institutional mining discipline and absurd amounts of capital to a sector previously defined by niche players.

The Supply Chain Battlefield: Geographic Realities Versus Market Expectations

The market likes to pretend that lithium is a frictionless global commodity, but the physical reality on the ground is a fragmented, logistically fragile mess that defies simple economic modeling.

The Dominance of the Australian-Chinese Axis

When you look at the raw data, the math seems simple: Australia digs up the rock, and China refines it. This axis is responsible for a massive chunk of global battery manufacturing. But this setup is fraught with systemic vulnerabilities. Shipping thousands of tons of heavy spodumene concentrate across the ocean just to roast it in Chinese kilns is an incredibly carbon-intensive process, which completely undermines the green ethos of the electric vehicle market. Western automakers are desperate to break this dependency, but the infrastructure simply does not exist elsewhere. Building a conversion plant in Europe or North America takes years of regulatory approvals and faces fierce local opposition. Hence, the Australian-Chinese axis remains dominant, not because people love the geopolitical implications, but because it is the only supply chain that actually functions at peak efficiency today.

The South American Dilemma

Meanwhile, the South American brine producers face a completely different set of structural bottlenecks. The Lithium Triangle holds the world's largest resources, yet getting that lithium out of the ground and to market is an administrative nightmare. Governments in the region are increasingly looking to nationalize resources or demand higher royalties, creating a highly unpredictable regulatory environment. Environmental concerns are also reaching a boiling point. Local communities are rightfully angry about the massive amounts of water used in the evaporation processes in hyper-arid deserts. Experts disagree on the exact long-term impact on local water tables, but the social license to operate is shrinking rapidly. You cannot simply double production in the Atacama or Hombre Muerto without triggering massive environmental and political pushback, meaning that South American brine cannot be viewed as a magic safety valve for surging global demand.

Common mistakes and misconceptions about global lithium giants

The illusion of country of origin

You probably think a company's headquarters dictates where the white gold gets extracted. That is a massive trap. Take Ganfeng Lithium, a Chinese titan that dominates the processing landscape. Except that its actual mining footprint spans from the rugged terrains of Australia to the high-altitude salt flats of Argentina. We confuse corporate registration with geological reality. Consequently, tracking who controls the reserves requires looking past the shiny corporate office and diving straight into the joint-venture paperwork of remote brine operations.

Brine versus hard rock efficiency

The market loves a simple narrative, yet the geological divide between spodumene mining and brine evaporation fractures this simplicity entirely. Investors frequently assume that all lithium production carries the same cost basis and environmental footprint. Let's be clear: it does not. Chilean brines boast incredibly low extraction costs but require years of solar evaporation. In stark contrast, Australian hard-rock mining delivers rapid output but demands heavy, energy-intensive crushing processes. (And let's not even start on the massive chemical processing discrepancies between the two methods).

Equating raw capacity with battery-grade output

Why do so many analysts get the supply crunch wrong? The problem is that announced capacity rarely equals battery-ready material. A company might announce an output of 100,000 metric tons of lithium carbonate equivalent, but if the purity levels fail to meet strict cathode specifications, that material is utterly useless for electric vehicles. It ends up downcycled into industrial glass or ceramics. Because refining technical-grade lithium into high-purity hydroxide requires a completely different level of chemical wizardry, many junior miners collapse before reaching commercial viability.

The hidden geopolitical bottleneck and expert advice

The downstream refinery monopoly

Look beneath the surface of the top 5 lithium producers and you will uncover a unsettling asymmetry. Mine ownership is reasonably diversified across continents, but the processing bottleneck remains tightly coiled around a single nation. China refines over half of the world's battery-grade lithium. This means that even if an American or European firm extracts the raw ore, the rock typically takes a long voyage across the Pacific just to be purified. It is an absurd logistical dance.

How to evaluate future market dominance

If you want to anticipate which mega-producers will survive the next decade of price volatility, stop looking at current extraction volumes. Focus instead on direct lithium extraction technologies. DLE promises to bypass the slow evaporation ponds entirely, sucking lithium from brine in hours rather than months. Albemarle and SQM are throwing billions at these chemical innovations. My advice is simple: back the producers that are morphing into high-tech chemical processors, rather than those operating as mere quarry diggers.

Frequently Asked Questions

Which companies currently comprise the top 5 lithium producers globally?

The global hierarchy is anchored by a mix of Western chemical conglomerates and Chinese mining giants that dictate the pace of the energy transition. US-based Albemarle leads global supply, closely followed by Chile's Sociedad Química y Minera, which leverages the massive, low-cost Salar de Atacama. China's influence is solidified by Ganfeng Lithium and Tianqi Lithium, both of which hold massive stakes in prime Australian assets like the Greenbushes mine. Finally, Mineral Resources Limited, an Australian mining services powerhouse, rounds out this elite group due to its rapid scaling of hard-rock operations. Together, these five corporate entities controlled roughly 60 percent of global lithium output as we entered the mid-2020s.

How does the geographic distribution of lithium reserves affect these top producers?

The physical location of the lithium reserves creates distinct operational advantages and vulnerabilities for the market leaders. Australia provides the bulk of hard-rock spodumene, which allows companies like Tianqi to ramp up production faster than brine operations can manage. Meanwhile, the Lithium Triangle across Chile, Argentina, and Bolivia holds more than half of the world's identified resources in expansive salt flats. This geographic concentration forces producers to navigate complex local water rights and shifting political regimes. As a result: companies are increasingly forced to diversify their portfolios across different hemispheres to mitigate localized geopolitical shocks.

Will recycling replace the need for these massive lithium mining corporations?

The short answer is absolutely not within the next two decades. While battery recycling is scaling up rapidly, the volume of electric vehicles reaching their end-of-life today is a mere drop in the bucket compared to the sheer tsunami of demand coming from new manufacturing plants. Current estimates suggest recycled material will cover less than 10 percent of global demand by the early 2030s. The major producers know this, which explains why they are investing in recycling as a secondary compliance mechanism rather than a replacement for raw extraction. Millions of tons of virgin ore must still be pulled from the earth before a closed-loop circular economy becomes even remotely viable.

A definitive look at the lithium oligopoly

The race to secure the foundation of the modern energy grid has mutated from a standard commodities boom into a fierce, hyper-politicized chess match. We are no longer dealing with a free market driven solely by supply and demand curves. Governments are actively intervening, subsidizing local supply chains, and rewriting trade pacts to break foreign monopolies. This nationalist shift means the established titans will likely maintain their iron grip on the market, as building a compliant chemical supply chain from scratch takes nearly a decade. Do not expect new independent players to easily disrupt this hierarchy. The capital requirements are simply too punishing, and the technical hurdles of refining battery-grade material are too steep for newcomers to conquer. Ultimately, the future of global transport remains firmly shackled to the boardroom decisions of these few dominant corporations.