Decoding the Mineral Monopoly: Production Versus Reserves

To understand who controls the white gold rush, you have to look past the superficial mining statistics. The industry suffers from a fundamental split identity. On one hand, you have the extraction of raw spodumene ore from hard rock; on the other, the solar evaporation of lithium-rich brines. This distinction splits the crown between two hemispheric titans, and frankly, people don't think about this enough when analyzing supply chain vulnerabilities.

The Australian Hard-Rock Heavyweight

Australia does not possess the largest volume of elemental lithium sleeping in its crust, yet it remains the undisputed king of active supply. The country extracted massive quantities of spodumene concentrate primarily from Western Australian mega-deposits like the Greenbushes mine and the Pilgangoora operation. The thing is, digging up rocks is fast. Hard-rock mining requires substantial energy and capital infrastructure, but it bypasses the multi-year waiting rooms required by South American brine evaporation pools. This operational velocity explains why Australian output reached such staggering heights, feeding chemical processing plants across the Pacific almost as fast as haul trucks can dump the ore.

The South American Brine Sleeping Giant

Travel across the ocean to the high-altitude deserts of the Andes, and the entire landscape changes. Chile holds the world's most significant economically viable lithium reserves, estimated at more than 9.3 million metric tons. The Salar de Atacama is essentially a giant subterranean juice box of highly concentrated lithium brine. Yet, Chile's annual production hovered around 49,000 metric tons. Why the discrepancy? Because extracting lithium from salt flats is an exercise in extreme patience. Brine is pumped into gargantuan surface ponds, where operators must wait up to 18 months for the sun to cook off the water. It is cheap, highly profitable, but frustratingly slow to scale up when an automaker demands a million new EV batteries by next Tuesday.

---The Shadow Hegemon: Why Extraction Data Lies About Power

Here is where it gets tricky. If you read a standard commodity report, you might assume Australia and Chile hold all the leverage in the energy transition. But that changes everything when you look at the chemical processing maps. Raw lithium pulled from the ground is completely useless for a battery. It must be converted into high-purity lithium carbonate or lithium hydroxide. And that is where one country holds an absolute stranglehold.

The Refining Choke Point in Mainland China

China mined roughly 41,000 metric tons within its own borders, placing it third in raw extraction. But we are far from a balanced market here. Chinese conglomerates have systematically purchased massive equity stakes in Australian mines and African development projects. Think about Tianqi Lithium owning a massive slice of the Greenbushes mine in Australia, or Ganfeng Lithium expanding its footprint across the Argentinian salars. They import the raw Australian spodumene rock, haul it to domestic coastal refineries, and transform it into the premium chemicals required by cathode manufacturers. They built the industrial apparatus while the West was still debating the environmental optics of open-pit mining.

The Battery Integration Dominance

The real power does not belong to the entity holding the shovel; it belongs to the one running the kiln. Because China refines the vast majority of the world's battery-grade chemicals, western automotive supply chains remain utterly dependent on Chinese industrial goodwill. It is a brilliant, multi-decade geopolitical chess move. By letting Australia handle the messy, water-intensive, and politically sensitive task of digging up the earth, Chinese corporations focused their capital on the high-margin, technologically complex chemical synthesis stage. As a result: every major electric vehicle ecosystem on earth eventually routes its capital through a Chinese processing hub.

---The Corporate Titans Orchestrating the Global Lithium Flow

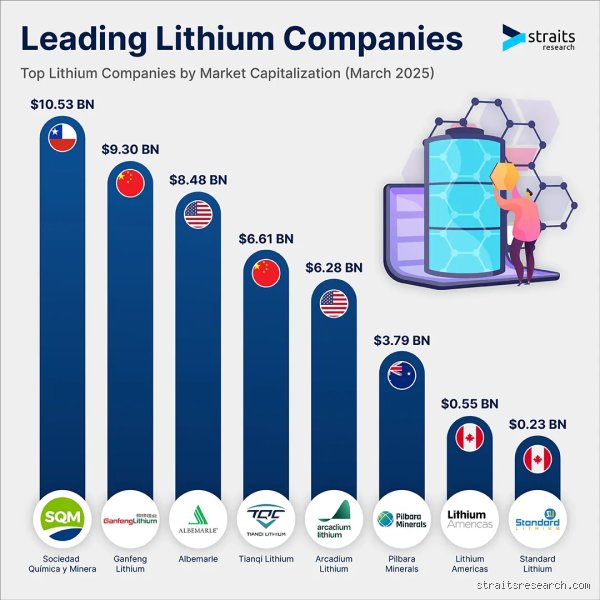

Nations do not actually sign mining contracts; corporate boards do. The corporate landscape is highly consolidated, dominated by an oligopoly of corporate entities that possess the technical know-how to manage these finicky chemical yields. The balance of power among these corporate actors shifted dramatically following high-profile mergers and acquisitions.

The North American and Chilean Dual Sovereigns

For years, Charlotte-based Albemarle Corporation stood as the world's largest corporate lithium producer. Albemarle operates a fascinatingly diverse portfolio, running brine operations alongside state partnerships in Chile's Atacama desert while simultaneously maintaining half-ownership of the Australian Greenbushes mine. Their chief rival on the brine front is Sociedad Química y Minera de Chile (SQM), a corporate entity that operates under strict, often contentious government quotas in the Chilean sun. These two giants essentially dictate the baseline pricing of global lithium brine assets. Honestly, it's unclear whether state intervention will eventually choke their margins, as resource nationalism in Santiago continues to cast a long shadow over future lease renewals.

The Consolidated Challengers

The industry entered a phase of aggressive cannibalization. Major mining conglomerates realized that building a lithium project from scratch is an absolute nightmare. Rio Tinto finalized its massive acquisition of Arcadium Lithium, a deal that instantly transformed the mining legacy house into a frontline lithium superpower with assets spanning from Argentinian brines to Canadian hard rock. Meanwhile, in North America, corporate consolidation led to the birth of Elevra Lithium after Sayona Mining swallowed Piedmont Lithium to unify operations in Quebec. These moves show that the industry is maturing; the wild-west era of speculative junior explorers is giving way to institutional scale.

---Geographic Shifts: The Emergence of the Lithium Triangle

While Australia maintains its current crown, the long-term center of gravity is shifting irrevocably toward a specific, arid pocket of South America. The Lithium Triangle—comprising the high-altitude borders of Chile, Argentina, and Bolivia—contains more than half of the world's identified lithium resources. But exploiting these assets is proving to be a logistical and political minefield.

Argentina's Western-Friendly Boom

Argentina has quickly become the most dynamic frontier in the brine world. Unlike Chile, which treats lithium as a strategic national asset managed tightly by the state, Argentina has historically offered a decentralized, province-led regulatory environment. This pro-market stance attracted a frenzy of foreign capital. Production in Argentinian salars like Hombre Muerto reached 18,000 metric tons and is scaling rapidly. Foreign developers are rushing to build infrastructure before the next macroeconomic swing occurs. Yet, the issue remains: can the country’s fragile electrical grid and remote desert roads handle the massive industrial transport required to ship thousands of tons of white powder down from the Andes?

The Bolivian Paradox

Then there is Bolivia, home to the Salar de Uyuni, an ethereal salt flat holding an estimated 23 million metric tons of lithium resources. It is, on paper, the biggest treasury of lithium on the planet. Want to guess how much commercial battery-grade lithium Bolivia supplied to the global market last year? Virtually zero. A combination of intense political instability, infrastructure deficits, and a stubborn insistence on total state control has kept the Bolivian lithium reserves locked beneath the salt. It serves as a stark reminder to Wall Street analysts: resources in the ground mean absolutely nothing if you cannot find a way to get them to a port.

Common mistakes and misconceptions

The confusion between extraction and processing

You probably think the country pulling the rocks out of the dirt owns the entire supply chain. Except that mining is merely the prologue. While Australia dominates raw extraction, China monopolizes the chemical conversion phase, turning spodumene concentrate into battery-grade lithium hydroxide. It is a massive intellectual blunder to confuse geological abundance with industrial dominance. Greenbushes in Western Australia might be the most prolific mine on Earth, yet its output frequently sails straight to Chinese ports for refining.

The myth of the Lithium Triangle monopoly

South America holds the world's largest resources. Because of this, commentators loudly proclaim that Chile, Argentina, and Bolivia dictate global prices. Let's be clear: resources in the ground mean absolutely nothing if bureaucratic inertia and political nationalism freeze investment. Chile possesses staggering brine reserves in the Atacama desert, which explains why SQM and Albemarle operate there, but rigid government quotas have allowed hard-rock mining elsewhere to steal the crown. The biggest supplier of lithium in the world is not a South American cartel; it is a network of Australian hard-rock crushing operations backed by Asian capital.

Brine versus spodumene processing speeds

Why does Australia outpace the Andes? The problem is time. Evaporating lithium chloride from brine pools takes up to 24 months, leaving operations at the mercy of weather patterns. Hard-rock spodumene mining requires traditional digging and crushing, a much faster route to market. Investors often assume all lithium is created equal, ignoring that direct shipping ore (DSO) bypasses lengthy chemical evaporation entirely.

The geopolitical choke point: Lepidolite and unconventional sources

The hidden Chinese backup plan

Did you know that when global prices skyrocket, Chinese refiners turn to a dirty, low-grade mica mineral called lepidolite? This is the industry's dirty little secret. Western analysts frequently miscalculate the total output of the biggest supplier of lithium in the world because they overlook these costly, high-pollution domestic operations in Jiangxi province. It acts as an emergency pressure valve for the market. (Predicting supply curves without accounting for lepidolite is like counting oil reserves while ignoring fracking). The environmental toll of processing this low-yield mineral is catastrophic, producing vast mountains of toxic slag, yet Beijing tolerates the ecological damage to maintain its fierce grip on global battery supply chains.

Frequently Asked Questions

Which company is the biggest supplier of lithium in the world?

The title belongs to Albemarle Corporation, a US-based specialty chemicals giant, though China's Ganfeng Lithium and Tianqi Lithium operate at a similar gargantuan scale. Albemarle controls a massive 49 percent stake in the unparalleled Greenbushes mine in Australia, alongside extensive brine operations in Chile's Salar de Atacama and Silver Peak in Nevada. In recent fiscal disclosures, Albemarle managed to generate over 7.3 billion dollars in annual revenue, driven primarily by its aggressive lithium segment. This corporate dominance means a single board of directors in Charlotte, North Carolina, influences the trajectory of global electric vehicle production. As a result: their expansion choices dictate whether carmakers face battery shortages or surpluses.

Can recycling replace mining to meet global demand?

The short answer is no, not for the next two decades. The issue remains that the total volume of electric vehicle batteries reaching their end-of-life status today represents a mere fraction of what the market requires for future production. We simply do not have enough old batteries in circulation to create a closed-loop system. Current recycling facilities can extract up to 95 percent of purified lithium from spent cells, but this technological efficiency is irrelevant without raw material volume. Miners must continue blasting rock and pumping brine until the global fleet fully transition to electric power.

Are solid-state batteries going to eliminate the need for lithium?

This is a widespread technological misunderstanding. Solid-state technology changes the architecture of the battery by replacing the liquid electrolyte with a solid alternative, but the energy-carrying chemistry still relies heavily on lithium ions. In fact, many solid-state designs utilize a pure lithium metal anode, which actually increases the intensity of the raw material requirement per pack. Are we going to see a post-lithium world anytime soon? No, because alternative chemistries like sodium-ion only compete in cheap, short-range vehicles due to their vastly inferior energy density. High-performance applications will demand the lightest metal on the periodic table for the foreseeable future.

A realistic outlook on global resource dominance

The global race for white gold is less about geographical luck and more about industrial execution. We must accept the harsh reality that Western nations are decades behind in building the processing infrastructure required to challenge Asian supply chains. Discovering a massive deposit in Nevada or the United Kingdom looks fantastic in corporate press releases, yet building a refinery takes years of permitting battles. The biggest supplier of lithium in the world will remain an alliance between Australian extraction and Chinese chemical engineering. Relying on slow-moving democratic institutions to match the top-down mandate of authoritarian industrial strategy is a losing game. True energy independence requires localizing the dirty, energy-intensive chemical refinement phase, not just bragging about the rocks sitting under our feet.