The Invisible Oligopoly Dominating the Battery Supply Chain

Everyone talks about Tesla, BYD, and the grand promises of a fully electrified future. But who feeds the beasts? The reality of the mining sector is far grittier than the sleek, minimalist showrooms of electric vehicle brands. We are dealing with a handful of chemical giants operating in geopolitical hotspots, balancing volatile spot prices against the insatiable hunger of gigafactories. It is a high-stakes poker game played with heavy machinery.

Brine Versus Hard Rock: The Great Extraction Divide

Where it gets tricky is understanding that lithium is not just dug out of the ground like coal. You either pump it out of subterranean, hyper-saline lakes in the High Andes, a process that takes eighteen months of solar evaporation, or you blast it out of spodumene pegmatite rocks in places like Greenbushes, Western Australia. Albemarle, an American chemical giant based in North Carolina, has mastered both. They operate the Silver Peak mine in Nevada—honestly, it’s a drop in the bucket compared to global demand—but their real crown jewels lie in the Salar de Atacama in Chile and the massive spodumene deposits down under. Yet, the industry remains split down the middle by these two radically different extraction methods, each carrying its own massive environmental baggage and capital expenditure profile.

The Shadowy Grip of Chinese Refining Dominance

Mining the raw material is only half the battle. Because what good is raw spodumene concentrate or lithium chloride brine if you cannot convert it into battery-grade lithium hydroxide or carbonate? This is where Chinese players like Ganfeng Lithium and Tianqi Lithium entered the fray, executing a brilliant, decades-long chess strategy. They bought up massive equity stakes in Western mines—Tianqi famously paid 4.1 billion dollars in 2018 for a slice of SQM—while building out unparalleled domestic refining capacity. The Western world is currently scrambling to build its own processing plants, but we're far from it, considering China still processes over sixty percent of the world’s battery-grade chemicals.

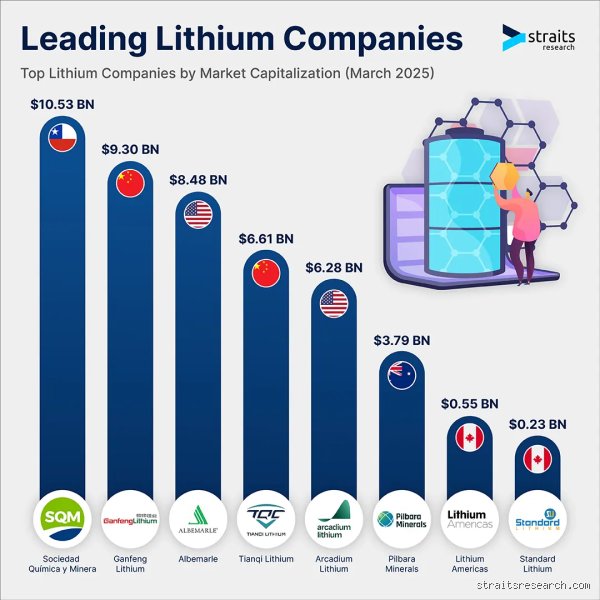

The Heavyweight Champions: Breaking Down the Industry Leaders

Let us look at the actual balance sheets and operations of the giants that dictate the pace of global electrification. The landscape shifted dramatically in early 2024 when Livent and Allkem merged to form Arcadium Lithium, a multi-billion-dollar entity created specifically to survive the brutal cyclical downturns of the commodity market.

Albemarle and the American Ambition

Albemarle behaves like the traditional blue-chip corporation it is, anchoring its strategy in long-term supply contracts with automotive OEMs. In 2023, they generated billions in lithium-related revenues, flexing their muscle across multiple continents. But the thing is, even a giant can stumble when prices crash by over eighty percent, as they did during the recent market correction. They had to scale back expansion plans in Australia and cut capital expenditure. That changes everything for junior miners who were hoping for Albemarle to buy them out, proving that even the biggest player on the board is at the mercy of the spot market.

SQM and the Geopolitical Tightrope of Chile

Sociedad Química y Minera de Chile, or SQM, operates over one of the most lucrative geological anomalies on Earth: the Atacama desert. Their cash costs are the envy of the entire mining world because the Chilean sun does the heavy lifting of evaporating the water for free. Genius, right? Except that the Chilean government decided to shake things up by introducing a national lithium strategy, forcing SQM into a complex partnership with state-owned copper giant Codelco through 2060. It is a stark reminder that political risk in South America is never truly off the table.

Ganfeng: The Ultimate Ecosystem Player

Unlike Western companies that focus purely on extraction, Ganfeng has integrated itself vertically throughout the entire lifecycle. They own stakes in the Mount Marion mine in Australia, the Cauchari-Olaroz brine project in Argentina, and they even recycle batteries. This massive diversification allows them to absorb shocks that would bankrupt smaller exploration companies. Analysts often argue whether a pure-play miner or a diversified chemical processor is the better bet, but looking at Ganfeng's footprint, the integrated model seems remarkably resilient.

The Geopolitics of Where Lithium Extraction Actually Happens

Geography is destiny in the mining world. You cannot choose where the geological anomalies occurred millions of years ago, which explains why the global map of lithium production looks so incredibly lopsided. It is a tale of two distinct regions: the Lithium Triangle in South America and the rugged outback of Western Australia.

The Lithium Triangle vs. the Australian Outback

Chile, Argentina, and Bolivia form the famous Lithium Triangle, holding more than half of the world's known resources. But resources do not equal production. Bolivia has struggled for years with infrastructure and political ideology, producing negligible commercial volumes. Argentina, however, is a different story altogether. Under a more pro-market administration, Argentina has become a wild-west frontier for lithium investment, with companies like Arcadium Lithium and various Chinese consortiums rushing to bring brine projects online. Contrast this with Australia, which focuses almost entirely on hard-rock spodumene mining. Australia is the world's largest exporter of raw lithium units, sending the majority of its dense rock straight to Chinese ports for processing. It is faster to scale up than a brine project, but the energy requirements for crushing and roasting rock are astronomical.

Beyond the Big Five: Are Alternative Producers Gaining Ground?

Is the current oligopoly safe from disruption? Not necessarily. People don't think about this enough, but the sheer volume of capital pouring into alternative extraction technologies could rewrite the corporate leaderboard by the end of the decade.

The Direct Lithium Extraction Disrupters

Enter Direct Lithium Extraction, or DLE. This technology promises to bypass the massive evaporation ponds entirely, using adsorption or ion-exchange membranes to pull lithium directly from brine water in a matter of hours rather than months. Oil majors like ExxonMobil and Chevron have noticed. ExxonMobil purchased drilling rights in the Smackover Formation in Arkansas, aiming to become a major domestic supplier by 2030 using DLE. If these oil giants successfully apply their fracking and fluid-handling expertise to lithium brines, the traditional mining companies will face a brand-new breed of competitor. But experts disagree on whether DLE can scale efficiently without destroying local freshwater aquifers, meaning the technology remains a massive, unproven gamble on a commercial scale. Hence, the old guard sleeps soundly for now.

Common Mistakes and Misconceptions About Lithium Production

The Illusion of the Monopoly

You probably think China digs up all the world's white gold. It does not. While Chinese refineries dominate the chemical conversion phase, the actual raw extraction tells a completely different story. Australia sits comfortably on the throne of raw hard-rock mining, while Chile commands the largest brine reserves. The problem is that we conflate processing dominance with geological ownership. Western media panics daily about supply chains, yet the physical rocks are far more geographically dispersed than public narrative suggests. Albemarle and SQM retain massive extraction footprints outside of Beijing's direct control.

Brine Versus Hard Rock Is Not a Simple Choice

Is traditional spodumene mining worse than evaporative brine harvesting? Investors love simple binaries. Except that ecology refuses to cooperate with Wall Street's neat boxes. Hard-rock mining in Western Australia requires immense energy to crush solid pegmatite structures. Conversely, South American brine pumping uses solar evaporation, which sounds pristine. But what about the local water tables in the Atacama Desert? It is a trade-off. Direct Lithium Extraction (DLE) technologies promise to disrupt this binary entirely, though commercial scaling remains painfully slow. Let's be clear: there is no such thing as zero-impact mining.

Every Lithium Ion Is Not Equal

Battery manufacturers cannot just throw raw technical-grade lithium carbonate into an electric vehicle assembly line. The distinction between battery-grade carbonate and high-purity lithium hydroxide matters immensely. Hydroxide is favored for high-nickel NMC batteries because it synthesizes at lower temperatures. Carbonate rules the surging Lithium Iron Phosphate (LFP) market. Companies that produce lithium must constantly recalibrate their chemical refining facilities to match these shifting automotive preferences. If a miner cannot hit 99.5% purity thresholds consistently, their product is essentially worthless for premium automotive contracts.

The Hidden Bottleneck: Tailings, Waste, and Geopolitics

The Invisible Cost of Refining Residue

What happens when you process thousands of tons of pegmatite? You get mountains of waste. For every ton of lithium hydroxide produced from hard rock, miners generate roughly thirty tons of aluminosilicate waste material. Managing these tailings facilities represents a massive operational headache that executives rarely discuss in glossy investor brochures. Why do you think so few refining plants open in strict jurisdictions like Western Europe?

Expert Advice: Look to the Pilot Plants

If you want to track where the market is moving, ignore the massive multi-billion-dollar announcements. Watch the demonstration facilities. Junior miners frequently claim they will become the next major player to produce lithium chemical derivatives at scale. But moving from a laboratory bench to a ten-thousand-ton commercial facility is a engineering nightmare. (We have seen dozens of junior exploration companies go bankrupt trying to bridge this exact gap). Watch the current development of geothermal brine projects in the Upper Rhine Valley or the Salton Sea; their success depends entirely on pilot facility uptime, not press releases.

Frequently Asked Questions

Which countries produce the most lithium globally?

Australia leads global extraction by a wide margin, accounting for roughly 52% of total worldwide production through its massive hard-rock spodumene operations like Greenbushes. Chile follows closely in second place, contributing approximately 25% of global output utilizing the massive brine resources of the Salton de Atacama. China secures the third spot with around 13% of domestic mine production, though its domestic chemical refining infrastructure handles over 60% of the world's battery-grade material. Argentina represents the fastest-growing brine jurisdiction, currently capturing nearly 6% of global market share as new projects in the Lithium Triangle come online. Zimbabwe and Brazil comprise the remainder of the significant global producers, though their total combined output hovers around 3% of the international aggregate market.

How long does it take to bring a new lithium mine online?

Developing a brand-new lithium asset from initial geological discovery to commercial production typically requires anywhere from eight to twelve years. Brine operations usually demand longer lead times than hard-rock mines because the evaporation process itself requires eighteen to twenty-four months of processing time before chemical conversion can even begin. Environmental permitting, indigenous community consultations, and complex hydrological modeling frequently delay project timelines by multiple years across North America and South America. Furthermore, securing the specific engineering expertise required to construct high-purity chemical conversion plants adds another layer of operational friction. As a result: supply deficits cannot be solved overnight by simply injecting capital into early-stage exploration ventures.

Will recycling replace the companies that produce lithium?

Spent battery recycling will not displace primary extraction companies for at least another two decades because the volume of electric vehicles reaching end-of-life status remains far too low. Current recycling facilities primarily process manufacturing scrap from gigafactories rather than consumer automotive packs. Experts project that by 2035, recycled material will satisfy only 15% to 20% of total global demand for battery manufacturing. Primary mining operations must expand dramatically to establish the initial global inventory of circulating technical-grade material. The issue remains that we cannot recycle what we have not yet dug out of the ground.

Beyond the Hype: The Sovereign Resource Reality

The global rush to secure battery metals has transformed a niche chemical sector into a fierce arena of geopolitical competition. We are witnessing the death of the open commodity market for battery minerals as resource nationalism takes hold from Santiago to Harare. Western automakers are frantically bypass traditional supply networks to sign direct offtake agreements with miners, desperate to comply with strict regional sourcing mandates. This frantic scrambling underscores a harsh reality: software cannot replace physical geology, no matter how much venture capital you throw at the problem. The future belongs not to the companies with the flashiest algorithms, but to the entities that control the physical conversion assets. Western nations will fail to secure supply chains unless they build domestic refining capacity rather than just subsidizing battery assembly plants. In short, owning the mine is meaningless if you still rely on overseas competitors to bake the cake.