The white gold paradigm: why commodity cycles trick retail investors

People don't think about this enough: commodity markets are intentionally designed to break your heart. Lithium is not a rare earth mineral, nor is it scarce in the crust of our planet, but building a chemical processing plant that can consistently spit out battery-grade lithium hydroxide with parts-per-billion purity is an absolute nightmare. After the spectacular, almost comedic collapse of spot prices from their historic peak of over eighty thousand dollars per metric ton down to the painful depths of late 2024, the entire sector was left for dead. Yet, the fundamentals didn't vanish.

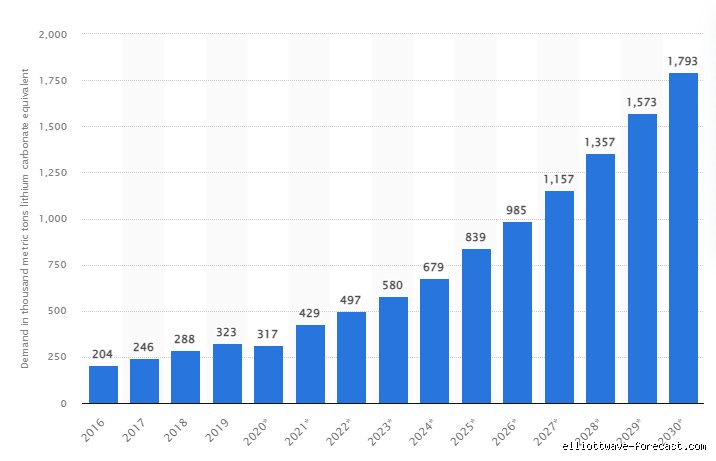

The hidden drivers of the 2026 deficit

Where it gets tricky is looking past the headline data. Everyone tracks electric vehicle adoption curves like a religion, but the growth in stationary energy storage systems has quietly exploded in parallel, jumping an astonishing seventy-one percent in 2025 alone. Data centers powering artificial intelligence clusters need ungodly amounts of backup power, and they are not buying diesel generators anymore. As a result: the market is aggressively pivoting into a structural supply deficit estimated between twenty-two thousand and eighty thousand metric tons. The supply side simply cannot keep up because major miners aggressively shelved their capital expenditure programs during the recent downturn.

The illusion of cheap spot pricing

But wait, if things are so bright, why did global lithium prices pull back slightly last week to around twenty-six dollars per kilogram? That changes everything if you are a short-term futures trader, except that physical supply agreements between major miners and automotive companies rarely reflect these daily spot acrobatics. Chinese converters have been digesting a massive, hidden inventory selloff, which skews public data feeds. Honestly, it's unclear when that specific inventory flush ends, but buying an equity based on the spot price of the current week is a textbook amateur mistake. You are investing in the asset's capability to generate free cash flow over a decade, not a month.

The standard-bearer: why scale is the only structural moat that matters

I am firmly convinced that trying to guess which micro-cap junior explorer will strike it rich in Western Australia is an exercise in futility. In this environment, scale isn't just an advantage—it is survival. When car manufacturers scramble to secure supply chains that comply with stringent local regulatory frameworks like the United States Inflation Reduction Act, they don't call startups. They call companies that own diversified, multi-continental assets.

Albemarle and the western premium advantage

This brings us to Albemarle Corporation, a specialty chemicals giant currently sitting at an impressive twenty-two billion dollar market capitalization. Albemarle owns a piece of the legendary Greenbushes hard-rock mine in Australia, operates brine extraction in the Salar de Atacama in Chile, and runs the only operational lithium mine in the United States at Silver Peak. That geographic footprint gives them a magnificent moat. Because of their domestic extraction capabilities, their product commands a distinct structural premium from automakers desperate to qualify for federal electric vehicle tax credits. Wall Street sentiment has subsequently shifted from extreme caution to an aggressive buy consensus, targeting a fair value of nearly two hundred dollars per share.

Protecting margins with variable-contract architecture

The company has radically altered how it sells its products. Instead of exposing themselves entirely to volatile spot prices or locking themselves into fixed-price contracts that leave money on the table when markets surge, they have transitioned heavily to a variable architecture featuring robust floor-and-ceiling price mechanisms. Take their massive one-hundred-thousand-ton supply agreement with Ford, or their parallel deals with BMW. These agreements ensure that even if the broader commodity market takes another sudden, unexpected dive, Albemarle's cash flow remains completely insulated. Their massive Meishan processing plant in China is now running efficiently, lowering their overall spodumene conversion costs and expanding their margins even while smaller competitors struggle to break even.

Geopolitical realities and the battle for the low-cost crown

Evaluating this sector requires a cold, hard look at geopolitical risk. The lithium world is essentially bifurcated into hard-rock spodumene mining and salar brine evaporation, each carrying vastly different operational profiles and political headaches.

The Chilean dilemma and SQM

Sociedad Química y Minera de Chile, widely known as SQM, is the world's absolute lowest-cost producer of high-grade lithium carbonate. Their operations in the Chilean desert enjoy unparalleled solar evaporation conditions, allowing them to extract the mineral for a fraction of what it costs to dig rocks out of the Australian outback. But the thing is, nationalization fears and shifting regulatory frameworks under Chile's complex national lithium strategy have continuously depressed their valuation. Their stock has taken a punishing thirty-five percent hit over the last year despite their immense volume output. It is a classic value trap: incredible assets wrapped in a layer of persistent sovereign risk that keeps institutional mega-funds at arm's length.

The consolidation wave of the mid-tier majors

Conversely, the corporate landscape is rapidly consolidating to combat this exact type of regional volatility. Look at the massive merger that created Arcadium Lithium, combining complementary brine and hard-rock footprints across multiple continents to build a diversified challenger. This corporate marriage gives them immense leverage when negotiating massive multi-year off-take agreements with global battery manufacturers. Analysts are already predicting an upside move approaching fifty percent over the next twelve months as their combined operational synergies finally begin to show up on the balance sheet. It proves that the era of the independent, single-asset producer is quickly drawing to a close.

Beyond the mines: alternative ways to deploy capital in the battery ecosystem

What if you don't want to own a mining company at all? It is an entirely fair position to take, considering the operational headaches of labor strikes, equipment failures, and environmental permitting delays that plague traditional extraction industries.

The demand-side alternative of specialty manufacturers

You can choose to play the lithium boom from the safety of the downstream technology layer. EnerSys is a prime example of this strategic pivot, trading at a comfortable seven-point-seven billion dollar valuation with an impressive year-to-date growth rate brushing past thirty-eight percent. They don't touch a shovel; they manufacture advanced motive power batteries, defense-sector energy storage systems, and telecommunications backup infrastructure. By letting the miners take the bruising commodity hits on the chin, EnerSys simply purchases raw chemical inputs at market rates, packages them into highly sophisticated engineering solutions, and sells them to corporate clients at steady, predictable margins.

The solid-state gamble

Then there is the wild frontier of pre-revenue technology plays like QuantumScape, which is aggressively burning through cash reserves to commercialize next-generation solid-state batteries alongside Volkswagen. Their technology replaces the standard liquid electrolyte with a solid ceramic separator, promising faster charging times and an elimination of traditional fire hazards. This is an incredibly speculative name that could easily double or drop to zero depending entirely on third-party validation milestones. Experts disagree vehemently on whether solid-state chemistry can ever achieve cheap mass manufacturing efficiency before the end of the decade. For a truly grounded investor, holding through a thirty percent portfolio drawdown on pure laboratory hope is an exhausting way to build long-term wealth.

Navigating the Lithium Minefield: Pitfalls and Illusions

The Spodumene Versus Brine Misconception

Investors often treat all lithium sources as equal. They are not. Hard-rock spodumene mining in places like Western Australia boasts faster commissioning times but demands a ferocious amount of energy to roast the ore at temperatures exceeding 1,000 degrees Celsius. Conversely, South American brine operations rely on solar evaporation, which takes up to 24 months to yield harvestable material. The mistake is assuming a low cash-cost projection on paper translates to immediate market dominance. It does not, because chemical purity profiles differ wildly between a continental deposit and a salar. If you buy a junior miner expecting quick brine returns, you will likely watch your capital evaporate faster than the pond water.

Chasing the Spot Price Ghost

Retail traders obsess over daily Chinese spot prices for lithium carbonate. Why? Because it is a visible ticker. Yet, the issue remains that over 80 percent of global lithium transactions occur via confidential, long-term legacy contracts between major producers and automotive battery consortia. This discrepancy means public spot indices frequently reflect illiquid, marginal transactions rather than the actual realized pricing of healthy operators. Buying a stock simply because the Guangzhou spot price ticked up three percent this morning is an architectural failure of logic. You are effectively valuing a house based on the price of a single loose brick.

The Geopolitical Trap and Processing Prowess

Where the True Refining Monopoly Lives

Every talking head on financial television screams about mining permits in Nevada or Quebec. They are missing the entire chessboard. Extracting the raw mineral is merely the first, mud-covered step. The real choke point is chemical conversion into battery-grade lithium hydroxide. China currently controls approximately 65 percent of global lithium refining capacity. Let's be clear: a mining company with five million tons of high-grade resource in Canada is effectively toothless if it must ship that raw concentrate across the Pacific just to make it usable for an electric vehicle. When hunting for what is a good lithium stock to buy right now, you must audit the firm's localized refining partnerships, not just their acreage.

Direct Lithium Extraction (DLE) Hype

Can we finally bypass the massive evaporation ponds using tech? Wall Street loves the narrative of Direct Lithium Extraction because it sounds like a Silicon Valley software solution. But the problem is that DLE remains an unproven laboratory darling when scaled to industrial proportions. It requires staggering volumes of fresh water and bespoke polymer membranes that degrade rapidly under harsh, salty field conditions. Except that promoters omit these operating expenditures during their glitzy roadshows. True expert advice dictates favoring companies with unglamorous, proven mechanical processing methods over speculative, membrane-dependent startups.

Frequently Asked Questions

Is the current lithium market oversupplied?

The short-term horizon shows a modest structural surplus due to massive lepidolite expansion in China and lepidolite processing facilities ramping up production to over 120,000 tons of lithium carbonate equivalent (LCE) annually. However, this material is highly expensive to refine and carries a brutal environmental footprint, meaning these operations shut down the moment prices dip below eighteen dollars per kilogram. Meanwhile, global demand from energy storage systems and electric vehicle fleets is modeled to scale from roughly one million tons of LCE today to nearly three million tons by 2030. As a result: the apparent oversupply is a temporary inventory indigestion rather than a permanent state of the market.

What is a good lithium stock to buy right now for long-term stability?

For investors seeking to anchor their portfolio without enduring the wild, stomach-churning volatility of junior explorers, a diversified chemical giant like Albemarle or Sociedad Química y Minera de Chile (SQM) represents the safest vector. SQM, for example, operates out of the Atacama desert, which features the highest lithium concentrations and optimal evaporation conditions on earth, allowing them to maintain gross cash costs below five dollars per kilogram of LCE. These entities possess the massive balance sheets required to weather multi-year cyclical downturns that routinely bankrupt smaller competitors. Which explains why institutional capital consistently clusters around these low-cost, tier-one operations during market corrections.

How do solid-state batteries impact the choice of top lithium shares?

A common anxiety is that next-generation solid-state batteries will render current lithium investments entirely obsolete. Is this fear grounded in chemical reality? Not at all, because solid-state architecture actually requires up to up to ten times more pure lithium metal per kilowatt-hour than standard lithium-ion configurations because it replaces the graphite anode entirely. Therefore, an investor trying to determine what is a good lithium stock to buy right now should focus intently on producers capable of delivering ultra-pure, battery-grade metal or carbonate. The tech shift alters the required purity profile of the end product, yet the underlying demand for the raw element remains entirely non-negotiable.

The Verdict on Lithium Speculation

Stop waiting for a clean, risk-free signal to enter the critical minerals arena. Markets do not hand out outsized returns to those who wait for universal consensus, which is exactly why the current atmosphere of pessimism presents a generational accumulation window. We have reached a point where equity valuations have decoupled from the long-term physics of the global energy transition. If you are serious about deploying capital here, pick the low-cost producers with active, cash-generating assets rather than buying into a slideshow of a dry lakebed in South America. Our clear, unhedged position is that ignoring the sector during this cyclical trough is an expensive mistake you will regret by the turn of the decade. The chemistry wins in the end.