The anatomy of a corporate slice: What happens when a stock splits?

Let’s get one thing straight right out of the gate. A stock split is a cosmetic event, an accounting illusion that alters the share count while leaving the market capitalization utterly untouched. Think of it like a pizza cut into eight slices instead of four; you still have the exact same amount of food, but the individual pieces just look more manageable. When Nvidia executed its 10-for-1 split on June 7, 2024, investors suddenly held ten times as many shares, while the price per share dropped to one-tenth of its previous value. Did the company magically become ten times more valuable overnight? Far from it.

The accounting mechanics under the hood

The thing is, people don't think about this enough: the cash flowing through the business, the debt obligations, and the net income remain static. If a company boasts a market value of $100 billion with 500 million outstanding shares trading at $200 each, a 2-for-1 split simply shifts the ledger to 1 billion shares trading at $100. The total valuation stays locked at that identical $100 billion mark. Yet, the psychological impact on retail investors who previously viewed a triple-digit stock price as an insurmountable barrier is profoundly real, which explains why boards of directors bother with the administrative headache of authorization votes in the first place.

The psychological catalyst: Why market perception defies mathematical reality

Here is where it gets tricky for the average investor trying to time the market. Retail traders frequently confuse a cheaper nominal stock price with a cheaper valuation—a classic cognitive bias that Wall Street loves to exploit. But wait, if the intrinsic value is unchanged, why do we consistently witness a surge in buying volume the moment the new ticker price reflects on brokerage apps? It comes down to basic human behavior and accessibility.

The retail liquidity illusion

Historically, a high per-share price kept smaller accounts on the sidelines, particularly before the widespread adoption of fractional share trading by modern brokerages. When Apple rolled out its 4-for-1 split in August 2020, the pre-split price hovering around $500 plummeted to roughly $125, suddenly putting the tech giant within reach of millions of casual accounts looking to allocate leftover paycheck cash. That changes everything for momentum traders who thrive on volume. But we're far from it being a guaranteed win, because this sudden influx of retail capital often creates a temporary, sentiment-driven bubble that can pop just as quickly as it inflated.

The signaling effect from the C-suite

I firmly believe that the real value of a split lies not in the math, but in the confidence it telegraphs from the executive suite. Management teams rarely split a tanking stock; they split shares that have experienced a massive, multi-year run-up, signaling to the broader market that they expect this upward trajectory to sustain itself over the long haul. Except that sometimes this confidence is misplaced, leading to a painful hangover for anyone who bought at the post-split peak without checking the balance sheet first.

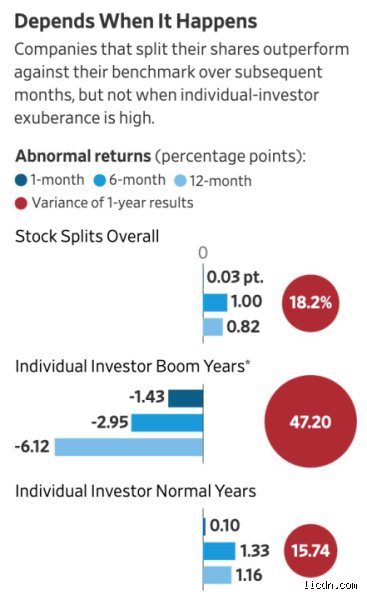

Historical evidence: Do post-split stocks actually outperform the S&P 500?

Data tells a far more compelling story than mere theory. According to extensive historical market research from Bank of America Global Research, companies that announced stock splits between 1980 and the present day outperformed the broader market by a significant margin over the subsequent twelve months. Specifically, post-split equities notched an average 25.4% return in the year following the announcement, compared to a modest 9.1% for the S&P 500 index during those same observation windows. That is a massive statistical anomaly.

Deconstructing the outperformance data

But let's look closer at those numbers before we run off to dump our life savings into the next split candidate. Is it smart to buy a stock after it splits based entirely on this historical edge? The issue remains that this outperformance is highly skewed by a handful of mega-cap tech winners—like Amazon, Alphabet, and Tesla—which were already fundamentally dominant enterprises firing on all cylinders before their respective splits occurred. The split didn't cause the growth; the explosive growth caused the split. If you bought Tesla after its 3-for-1 split in August 2022, you quickly realized that macroeconomic headwinds and rising interest rates matter infinitely more than how many shares are floating around the Nasdaq system.

The alternatives: Fractional shares versus waiting for the dip

With modern financial infrastructure moving at lightning speed, the traditional arguments favoring stock splits are losing their teeth. Fractional shares have revolutionized how the average person interacts with the stock market, rendering the nominal price of a single share practically irrelevant for anyone utilizing a modern fintech platform. Why stress over whether to buy a stock after a split when you can simply invest $10 into a $3,000 share of Chipotle right now?

The institutional playground

The institutional desks—the massive pension funds and algorithmic market makers handling billions of dollars out of Manhattan offices—could not care less about whether a stock trades at $50 or $5,000. They trade based on total dollar volume and enterprise value metrics. As a result: the post-split frenzy is almost exclusively a retail phenomenon, meaning that if you buy during the immediate post-split euphoria, you are frequently catching the tail end of a pump engineered by institutional players who are more than happy to sell their expensive blocks to eager, less-informed retail buyers chasing the headlines. Honestly, it's unclear why more investors don't just wait for the inevitable cooling-off period that typically follows the initial three-week post-split media circus.