Let us be real for a second. The stock market loves a good illusion, and corporate boardrooms know exactly how to play the crowd. When a company slices its stock, nothing tangible changes inside the business. Think of it like cutting a large pizza into eight slices instead of four; you still have the same amount of cheese and dough, yet the market somehow acts like you just received a free extra topping. This psychological quirk is precisely why the question of whether it is good to buy shares after split keeps trading desks awake at night.

The Mechanics of the Cut: Why Companies Chop Their Equity

To understand the real mechanics, we have to look past the flashing green lights on your broker app. When Nvidia executed its high-profile 10-for-1 split on June 7, 2024, the chip giant did not suddenly manufacture billions of dollars in new microchips overnight. Instead, they simply readjusted the denominator of their equity equation. The share price dropped from a hefty $1,200 range to a much more digestible $120, a move specifically engineered to open the gates for small-time investors who do not have access to fractional trading platforms.

The Liquidity Mirage

This is where it gets tricky for the average retail trader. A lower nominal price tag inherently boosts liquidity because trading volume spikes when a asset becomes accessible to the masses, which explains why daily turnover often jumps by nearly 30% in the immediate aftermath of these corporate announcements. More participants mean tighter bid-ask spreads. But does that mean the underlying company is actually worth more? Not at all, except that the sudden influx of capital frequently creates a short-term price squeeze that confuses valuation models.

The Boardroom's Hidden Signal

Management teams rarely split a stock that is crashing. I view these announcements as an implicit vote of confidence from the executives themselves, a corporate signal suggesting they expect the upward trajectory to continue. When a board votes to split, they are essentially bragging. They are telling Wall Street that their stock has grown so expensive that it requires intervention, which acts as a powerful marketing tool that attracts fresh institutional capital alongside the retail crowd.

Valuation Realities: What Changes and What Stays Exactly the Same

We need to talk about capitalization because people don't think about this enough when calculating their potential returns. Your ownership stake in the enterprise remains entirely unchanged. If you owned 0.01% of Apple before their 4-for-1 split in August 2020, you owned exactly 0.01% after the dust settled, meaning your claim on the company's net earnings did not budge a single millimeter. Market capitalization is the ultimate truth machine here, keeping valuation anchored regardless of how many pieces the equity pie is sliced into.

Earnings Per Share and the Dilution Fallacy

Do not confuse a stock split with a secondary offering. Because no new capital is being raised and no existing shares are being diluted, the net effect on your portfolio's intrinsic value is zero. The company's trailing twelve months (TTM) earnings per share (EPS) drops proportionally to the split ratio, matching the price decline perfectly. If a stock tracking at $400 with an EPS of $20 splits 4-for-1, the new price becomes $100 and the EPS shifts to $5. The price-to-earnings (P/E) ratio stays perfectly static at 20x, proving that that changes everything when it comes to visual perception, but changes absolutely nothing regarding fundamental worth.

The Option Market Ripple Effect

Where things actually shift is in the derivatives sandbox. Standard options contracts govern exactly 100 shares of the underlying equity, meaning that pre-split, controlling an option on a $1,000 stock required a massive capital outlay of $100,000 in notionally controlled value. Post-split, that same contract controls a much more manageable $10,000 chunk. This massive reduction in premium costs opens the floodgates for retail options speculation, driving up implied volatility and creating a chaotic trading environment that can whip the underlying stock around unpredictably.

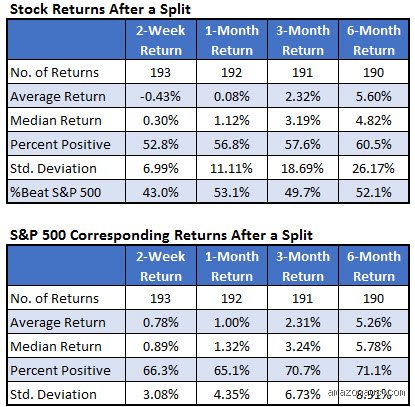

The Post-Split Timeline: Analyzing Historical Performance Trends

If we look at the historical data compiled by Bank of America Global Research over the past several decades, a fascinating pattern emerges that contradicts the pure academic theory of market efficiency. Companies that announce splits have historically generated average returns of 25.4% in the 12 months following the announcement, compared to a modest 11.9% for the broader index. That is a massive outperformance gap. Yet, the timing of your entry point during this cycle dictates whether you actually capture that alpha or end up holding a bag of overvalued equity.

The Announcement Bump vs. The Execution Slump

The biggest gains usually happen before the split even occurs. The moment the press release hits the wires, algorithmic trading systems and momentum chasers bid the price up in anticipation of the event. By the time the actual split date rolls around—often three to four weeks later—the excitement has already been fully priced into the equity. What happens next? Frequently, a classic "sell the news" correction takes place, where early investors lock in their gains, causing the stock to drift sideways or pull back during the initial days of trading under the new price structure.

The Six-Month Window of Opportunity

The real sweet spot for long-term investors usually opens up around three to six months after the split execution. Once the initial speculative froth blows off and the options volume normalizes, the stock begins tracking its fundamental metrics once again. If the business is genuinely healthy, the increased liquidity and broader shareholder base provide a solid floor for the next leg up. Institutional funds that were hesitant to buy into a retail-driven hype cycle often use these mid-term cooling periods to accumulate larger positions at a more reasonable valuation.

Direct Purchase vs. Waiting: Strategic Entry Point Alternatives

Is it better to buy shares after split or should you try to front-run the announcement entirely? The issue remains one of risk tolerance and capital preservation. Buying beforehand means paying a premium for the hype, while waiting means risking missing out on the initial momentum spike. Honestly, it's unclear which strategy works best across every market cycle, as macro conditions like prevailing interest rates and overall market sentiment heavily influence how investors react to these corporate announcements.

The Dollar-Cost Averaging Pivot

Instead of trying to time the exact date of the split, smart money often utilizes a staggered entry system. By deploying 50% of your intended capital two weeks before the split and reserving the remaining 50% for a month after the execution, you effectively hedge against the short-term volatility. This strategy mitigates the risk of buying at the absolute peak of the retail hype cycle while ensuring you still have skin in the game if the stock decides to pull an unstoppable rally right out of the gate.

The Post-Split Reality Check

Look at Tesla's 3-for-1 split in August 2022 as a cautionary tale. The stock rallied aggressively heading into the split, fueled by retail enthusiasm and manic options buying. But macroeconomic headwinds and broader tech sector liquidation soon took over, dragging the stock down significantly in the months that followed. This proves that a split cannot save a stock when the macro environment turns hostile; hence, assessing the broader economic landscape is far more important than staring at the nominal price of a single share.

Common mistakes and misconceptions that drain portfolios

The "cheap stock" optical illusion

Retail investors routinely fall into a psychological trap: they mistake a lower nominal share price for actual, mathematical value. Let’s be clear: a 4-for-1 split that drops a stock from $400 to $100 does not make the company a bargain. You own a smaller slice of the exact same pie. Yet, the temptation to buy shares after split lingers because human brains inherently prefer holding one hundred units of an asset rather than twenty-five. This cognitive bias triggers artificial, short-term demand spikes. Market capitalization remains entirely unchanged by these cosmetic adjustments, a reality that eager buyers frequently ignore until the initial post-split hype evaporates.

Chasing the immediate post-announcement surge

Another classic blunder involves timing the market based on the split calendar. Statistically, the largest price appreciation occurs between the initial corporate announcement and the actual execution date. By the time the split takes effect, institutional algorithms have already extracted the alpha. If you buy shares after split purely expecting an immediate, explosive upward trajectory, you are essentially catching the tail end of a exhausted trend. The issue remains that retail capital arrives late to the party, buying at local tops right when early insiders decide to harvest their gains.

Ignoring underlying corporate health

A stock split is a corporate action, not a business model. A struggling enterprise with deteriorating cash flows cannot engineer a fundamental turnaround by merely slicing its equity into smaller pieces. Because a split signals management confidence, it can easily mask operational decay. Think of failing tech companies in the early 2000s that split their stock right before plummeting into bankruptcy. Except that today's market is even faster at punishing businesses that rely on financial engineering rather than genuine revenue growth metrics.

The liquidity premium and institutional rebalancing

The hidden mechanics of the order book

Why do giant corporations bother with this administrative chore? The answer lies in market microstructure and options market liquidity. Lower absolute prices dramatically reduce the capital required to trade option contracts, since a single call or put controls exactly 100 shares of the underlying equity. When a stock trades at $1,000, one options contract requires $100,000 of nominal exposure, which prices out most retail derivatives traders. As a result: post-split environments see an explosion in options volume, which forces market makers to buy shares to hedge their positions, creating a subtle, systemic tailwind that few casual observers understand.

The retail fractional share paradox

In an era where modern brokerages offer fractional investing, does lowering the share price still matter? Surprisingly, yes. Even though you can technically buy $5 worth of any stock, major institutional funds and certain traditional retirement accounts operate under strict mandates that forbid trading fractional units. Furthermore, the psychological satisfaction of owning whole shares still drives significant volume. But is this behavioral quirk enough to sustain a long-term bull run? Not without robust fundamental catalysts backing up the underlying business operations.

Frequently Asked Questions

Does historical data support buying shares after a split?

Yes, historical empirical evidence suggests an upward trend, though it requires nuanced interpretation. Bank of America Global Research analyzed market cycles over several decades and found that companies implementing splits posted an average total return of 25.4% in the twelve months following the announcement, compared to just 9.1% for the broader S&P 500 index. Apple’s 2020 split serves as a prime example, where the equity experienced a massive surge in liquidity and retail participation immediately following its 4-for-1 execution. However, this outperformance is typically concentrated in the first six months, after which the stock’s trajectory reverts to its standard correlation with corporate earnings. (We must acknowledge that past performance never guarantees future market returns, especially during macroeconomic downturns).

How does a split impact dividend payments and yields?

A stock split has zero direct impact on your total dividend income or the net percentage yield. If a company pays an annual dividend of $4.00 per share and undergoes a 2-for-1 split, the payout is automatically adjusted to $2.00 per share. You now own double the amount of equity certificates, meaning your aggregate cash distribution stays perfectly identical. For instance, when Microsoft executed its numerous splits during its rapid expansion era, the total yield remained pinned to its broader capital allocation strategy rather than the shifting volume of outstanding equity. Investors who buy shares after split expecting a sudden windfall of passive income are fundamentally misunderstanding corporate accounting mechanics.

What is a reverse split and should investors avoid it?

A reverse split is the exact opposite mechanism, where a company consolidates outstanding equities to artificially inflate a dangerously low share price. This maneuver is usually a desperate attempt to avoid being delisted from major exchanges like the NYSE or Nasdaq, which typically require a minimum $1.00 closing price. While a forward split signals corporate health and an soaring stock price, a reverse split is almost universally a red flag indicating severe operational distress. Statistically, the vast majority of corporations executing reverse actions underperform the market significantly over the subsequent two-year window. In short, while a standard split invites optimistic accumulation, a reverse split should prompt immediate scrutiny or outright divestment.

The definitive verdict on post-split investing

Let's stop pretending that a corporate cosmetic change alters the intrinsic value of an enterprise. Buying an equity simply because it underwent a split is an intellectual shortcut that frequently leads to mediocre portfolio performance. True wealth accumulation requires analyzing balance sheets, free cash flow generation, and competitive moats. If the company was an overvalued mess at $800, it remains an overvalued mess at $100. We firmly believe that a split should only be viewed as a secondary confirmation of management’s optimism, never as the primary thesis for risking your capital. Look past the psychological illusions of the price tag and focus entirely on whether the business possesses the pricing power to dominate its industry over the next decade.