The Mechanics of Payouts: What It Actually Means to Reinvest Dividends or Take Them

Every quarter, corporate boards at cash-rich titans like ExxonMobil or Johnson & Johnson sit in boardrooms and decide how much cash to slice off and ship to shareholders. When that money lands, you face a stark choice. You can opt for a Dividend Reinvestment Plan, commonly known as a DRIP, which instantly converts that cash back into fractional shares of the issuing company. Or, you can let the cash accumulate in your brokerage account to buy groceries, pay mortgages, or invest elsewhere. This is where people don't think about this enough.

The Compounding Engine of the DRIP

When you automate the process, you trigger a silent, relentless compounding machine. Think of it as a snowball rolling down a steep hill in a Vermont winter. By bypassing human intervention, every single dollar of your dividend payout goes right back to work, buying more shares, which will in turn yield more dividends next quarter. Because you are buying fractional shares regardless of whether the stock is trading at an all-time high or plummeting during a market panic, you are effectively practicing dollar-cost averaging on autopilot. That changes everything for a long-term portfolio.

The Liquidity Route: Taking the Cash and Walking Away

But what if you choose the alternative? Taking the cash means your brokerage account receives a cash credit, which you can withdraw to your local bank account. It provides instant utility. Except that you lose the compounding momentum. If you leave that cash sitting idle in a low-yield sweep account, inflation quietly eats away at your purchasing power while the broader market marches upward without you. We are far from the days when keeping cash in a standard bank account yielded anything meaningful over the long term.

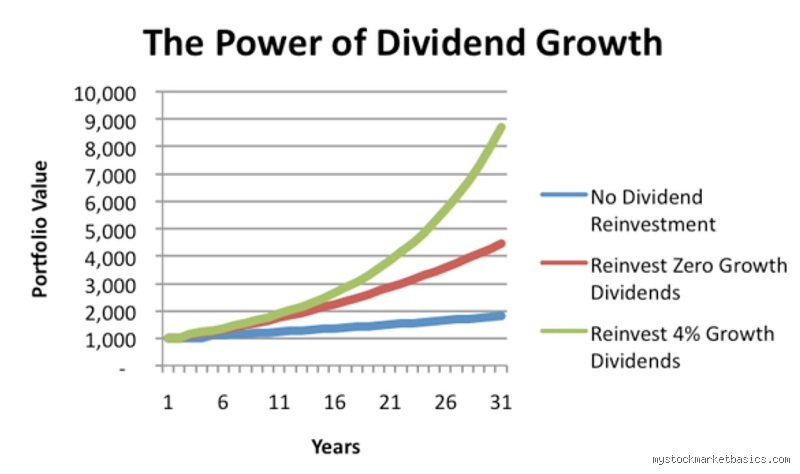

The Mathematical Brutality of Automated Growth Versus Cash Extraction

To truly understand the friction between these two paths, we have to look at the historical data, which paints a staggering picture of wealth divergence. Look at the S&P 500 index over any multi-decade period. Between 1960 and 2023, a massive 69% of the total return of the S&P 500 came from reinvested dividends compounded over time, not just capital appreciation. If you took the cash instead, your terminal wealth would be a pale shadow of what it could have been. Honestly, it is unclear why more investors don't obsess over this gap.

The Real-World Cost of Micro-Withdrawals

Let us look at a concrete example to ground this math. Imagine an investor named Sarah who bought 1,000 shares of Altria Group back in January 2010. If Sarah chose to take her dividends as cash to fund weekend trips, she received thousands of dollars in spending money over the next decade, but her share count stayed exactly at 1,000. But what if she chose to reinvest dividends instead? By 2020, her share count would have swollen drastically due to automated reinvestment, turning her modest stake into a massive income-generating engine. The difference is not a few hundred bucks; we are talking about a divergence of tens of thousands of dollars because of how the math curves upward over time.

Market Volatility Is Actually a DRIP Investor's Best Friend

Where it gets tricky is during a market crash. Imagine the Lehman Brothers collapse in September 2008 or the sudden pandemic panic of March 2020. Most investors panic and freeze. Yet, if your account is set to auto-reinvest, your dividends are automatically buying shares when prices are at rock-bottom discounts. You are accumulating more shares per dollar spent precisely when fear is highest. Is there any better way to remove emotion from investing? When the market eventually recovers, your newly acquired shares turbocharge your portfolio recovery.

Tax Dragons and Friction: The Hidden Costs Nobody Mentions

Here is a sharp opinion that contradicts conventional wisdom: automated dividend reinvestment can sometimes be a massive, bureaucratic headache that costs you money. Many retail investors mistakenly believe that if they reinvest dividends through a DRIP, they do not owe taxes on that money because they never touched the cash. That is a dangerous myth. The IRS views a dividend as taxable income the exact moment it is paid out, regardless of whether it was converted into fractional shares or deposited into your checking account.

The Tax Man Cometh, Reinvested or Not

If you hold these dividend-paying stocks in a standard, taxable brokerage account, you will receive a Form 1099-DIV every single year. You must pay taxes on those qualified dividends at rates up to 20%, depending on your income bracket, plus any applicable net investment income tax. And because you are buying tiny fractions of shares every single quarter at completely different prices, your cost basis becomes a chaotic, multi-layered nightmare. Imagine trying to calculate the exact capital gains on a stock you held for fifteen years with sixty different reinvestment tranches when you finally decide to sell. Hence, doing this outside of a tax-advantaged account like an IRA or a 401k requires pristine record-keeping.

The Psychology of the Phantom Tax Bill

It creates a weird psychological friction. You have to find the cash to pay taxes on income you never actually saw because it was immediately reinvested into more stock. For some, this feels like losing money. This explains why high-net-worth individuals often prefer to take the cash dividends from their taxable accounts to directly fund their annual tax liabilities, keeping their core portfolio clean and avoiding the need to liquidate shares to satisfy the IRS.

Strategic Flexibility: Why the Rigid Choice Might Be a Trap

While the purists argue that you must always reinvest to maximize terminal wealth, the issue remains that rigidity is often the enemy of optimal capital allocation. I believe that blindly reinvesting back into the exact same company can sometimes be an act of profound financial laziness. Just because a company paid you a great dividend this morning does not mean that its stock is currently a good value. What if the stock is wildly overvalued?

The Case for Manual Reinvestment

Consider a scenario where you own shares in a mature consumer staples company like Procter & Gamble. The stock is trading at an all-time high valuation multiple, while the tech sector or energy sector is experiencing a cyclical downturn and offering massive bargains. If you auto-reinvest, you are buying more expensive shares of P&G. But if you take the cash, you can manually accumulate those payouts and deploy them into the undervalued sectors. As a result: you actively optimize your asset allocation rather than letting an automated script dictate your portfolio's future weightings.

The Wisdom of Market-Wide Reinvestment

This approach effectively turns your portfolio into a self-rebalancing ecosystem. You extract capital from your mature, cash-generating holdings and use it to seed new positions or shore up underperforming assets that possess higher future growth potential. Experts disagree on whether the average retail investor has the discipline to do this effectively without letting cash sit idle, but for an active, astute manager, manual deployment beats blind automation nearly every time.

The Blind Spots: Common Misconceptions Dissected

The Myth of "Free" Shares

Many investors witness their share balance climb through automatic setups and assume it is a frictionless, cost-free miracle. The problem is that nothing in high-finance arrives without a receipt. When you reinvest dividends via a brokerage platform, you frequently bypass standard trading commissions, yes. Except that you completely overlook the underlying mechanics of equity dilution and market pricing. If a company distributes a one-dollar payout, its stock price instantly drops by that exact amount on the ex-dividend date. You are not receiving a bonus gift from a benevolent corporate board. Instead, you are merely rearranging deck chairs on your own financial Titanic if that business happens to be deteriorating. Let's be clear: converting cash into sliced-up equity slices does not magically manufacture wealth out of thin air.

The Phantom Tax Trap

Think ignoring the cash payout shields you from the taxman's reach? Think again. A staggering percentage of retail participants fail to realize that Uncle Sam demands his cut regardless of whether those funds ever touch your checking account. Because the IRS views a distributed payout as realized income the exact moment it becomes available, holding these assets in a standard taxable brokerage account triggers an immediate annual liability. Imagine paying taxes on a dividend reinvestment plan using money out of your own pocket while facing a liquidity crunch. It is the ultimate exercise in fiscal irony. If you cycle 10,000 dollars of annual distributions back into a firm, you might still owe up to 20 percent in qualified dividends taxes depending on your specific tax bracket, leaving you with a stealth bill at year-end.

The Velocity of Capital: Elite Allocation Nuances

The Opportunity Cost of Inertia

Blindly compounding your winners sounds like flawless textbook advice until you realize it breeds dangerous portfolio concentration. When you choose to take dividends instead of letting them ride on autopilot, you actively reclaim the steering wheel of your asset allocation. Why should a mature utility company trading at a premium valuation automatically deserve more of your hard-earned capital today? It shouldn't. Sophisticated wealth management requires treating every single distribution as fresh, unallocated dry powder. By gathering this cash, you grant yourself the tactical agility to pivot toward severely undervalued sectors or alternative asset classes. The issue remains that automatic reinvesting forces you to buy more shares of a specific company regardless of its current market valuation, essentially stripping you of your analytical edge.

Frequently Asked Questions

Does choosing to reinvest dividends outperform taking cash historically?

The historical data regarding long-term total returns paints an overwhelmingly clear, undeniable picture. Over a rolling twenty-year period, specifically tracking the S&P 500 index from 2004 to 2024, reinvested distributions accounted for a staggering 42 percent of the market's total accumulation footprint. If an investor initially deployed 10,000 dollars without activating a compounding mechanism, their final portfolio value trailed the active compounding strategy by hundreds of thousands of dollars. Which explains why pure wealth accumulation phases demand that you aggressively automate this process to capture the exponential curve. Of course, this math alters dramatically if the underlying asset enters a terminal secular decline, proving that historical benchmarks cannot fully substitute for ongoing credit analysis.

How does a dividend reinvestment plan impact the cost basis of my portfolio?

Every single automated purchase creates a completely distinct, separate tax lot with its own unique purchase price and specific acquisition date. As a result: calculating your adjusted cost basis over a decade of quarterly distributions transforms into a chaotic nightmare comprising forty individual micro-transactions per stock. Tracking these numbers precisely is vital for when you eventually decide to liquidate a portion of your holdings. Most modern custodians automate this data collection now, yet discrepancy errors still routinely crop up during complex corporate spin-offs or mergers. (Good luck untangling those spreadsheets without a certified public accountant by your side). Therefore, you must maintain impeccable digital records to avoid overpaying capital gains taxes down the line.

Can you change your mind between collecting payouts and compounding them?

Are you permanently locked into a specific distribution strategy once you check a box on your investment dashboard? Absolutely not, as most retail brokerages allow you to toggle between these two distinct modalities with a single digital click. For instance, an investor might spend fifteen years accumulating equity through a strict dividend reinvestment plan to maximize share accumulation. Then, upon hitting their target retirement date, they can immediately flip the switch to distribute cash directly into their bank account to fund daily lifestyle expenses. In short, your strategy should remain highly fluid, shifting dynamically alongside your shifting cash-flow requirements and macroeconomic realities.

The Final Verdict: Breaking the Autopilot Illusion

Wealth accumulation is never a binary choice between two flawless ideals. We strongly believe that the modern obsession with completely hands-off compounding has turned investors into passive passengers in their own financial journeys. If you are under forty and building a foundational nest egg, you should absolutely reinvest dividends to exploit the raw mathematical power of compounding interest. But let's stop pretending that automation is a universal panacea for every market cycle. The moment your portfolio crosses the threshold of self-sustaining significance, you must aggressively seize control of that cash flow to actively hunt for mispriced risks elsewhere. True financial mastery means refusing to let a software algorithm dictate your capital allocation strategy when asymmetric opportunities are staring you right in the face.