The Mechanics of Corporate Share Multiplication: Why Companies Slice the Pie

Most retail investors misunderstand how the stock market handles ownership slices. When a board of directors meets in a sleek room in Manhattan or Cupertino and decides to slice their equity thinner, they are not creating wealth out of thin air. They are just changing the denominator. But why bother? The issue remains that high absolute stock prices scare off regular folks who do not want to use fractional share brokerages. If a single share of a booming tech giant hits $900 on the Nasdaq, a small investor might hesitate to jump in. By executing a 3 for 1 split, that barrier vanishes as the price plummets to $300 per share. It feels affordable. Yet, the underlying market capitalization of the business stays entirely untouched. I find it amusing how millions of dollars in trading volume can shift just because human brains prefer buying whole numbers over fractions.

The Optical Illusion of Affordability

Let us look at the psychological landscape. When a company announces this move, the market usually rallies, which explains why so many rookie traders chase the news. They see a cheaper price tag and think it is a discount—except that it is not. Where it gets tricky is tracking the actual market sentiment post-announcement. History shows that liquidity improves dramatically after these corporate events. More people can trade the options contracts, which require 100-share blocks, hence creating a genuine surge in daily trading volume. It is a brilliant marketing stunt disguised as corporate finance.

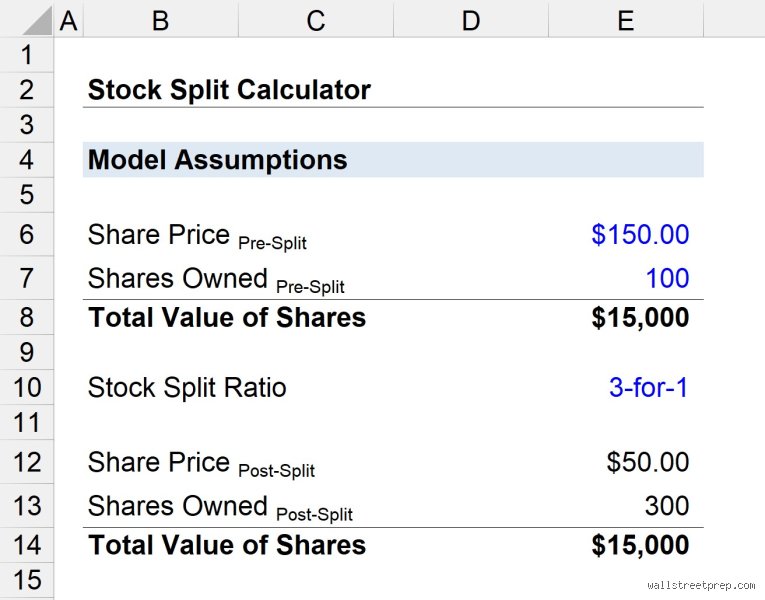

Behind the Math: Tracking a 100 Shares 3 for 1 Stock Split in Real Time

Let us map out the exact ledger adjustments during a 100 shares 3 for 1 stock split scenario using concrete historical numbers to ground the theory. Imagine you bought equity in a thriving enterprise on June 14, 2024, right before their corporate restructuring took effect. Your brokerage account statement shows exactly 100 units of stock, trading at a premium price of $600 per share. Your total principal investment equals a clean $60,000. Then, the split date passes. Suddenly, your portfolio screen looks completely different. You now hold 300 shares. But the price has dropped to $200 per share. Did you lose money? No. Did you gain wealth? Absolutely not. The multiplication is perfectly balanced by the division, keeping your total account equity locked at that exact same $60,000 value. It is exactly like taking a crisp twenty-dollar bill from your wallet and swapping it for four five-dollar bills; you do not suddenly have more cash to buy dinner, but your pockets certainly feel heavier.

The Journal Entries on Wall Street

The company’s accounting department faces a strict balancing act. The par value of the common stock drops to one-third of its original designation on the balance sheet. Simultaneously, the capital surplus accounts remain untouched because no new capital was raised from outside investors. Because of this rigid mathematical symmetry, institutional investors rarely bat an eye when these splits occur. They care about enterprise value and free cash flow yield, not the arbitrary number of outstanding shares floating around the ecosystem. But for retail option traders who rely on accumulating 100 shares to write covered calls, this tripling of position size completely transforms their premium-generation strategies.

The Impact on Dividends and Earnings Per Share

What happens to your quarterly payouts? If the firm previously distributed a dividend of $1.50 per share annually, that distribution undergoes the exact same division process. Your new payout becomes $0.50 per share. Since you now hold three times as many shares, your total annual passive income remains identical at $150. The same logic applies to Earnings Per Share (EPS). If the company reported an EPS of $9.00 before the split, the post-split EPS adjusts to $3.00. People don't think about this enough when they look at historical charts; if you do not adjust past data for splits, the company’s growth trajectory looks like a terrifying financial collapse.

Market Liquidity and the Hidden Agenda of the Boardroom

Corporate executives do not wake up and decide to alter their capital structure without a calculated motive. When a board triggers a 100 shares 3 for 1 stock split, they are often hunting for admission into elite, price-weighted stock indices. Take the famous Dow Jones Industrial Average, for instance. Unlike the S&P 500, which weights companies based on their total market value, the Dow calculates its daily movements based strictly on share price. If a company's stock price gets too high, it would completely dominate the index, making its inclusion impossible. By chopping the price down through a split, management can position their stock for a prestigious index inclusion. That changes everything for institutional fund managers who are forced to buy the stock once it joins the benchmark.

The Retail Trader Frenzy

There is another angle to consider here: employee compensation. Silicon Valley startups and multinational conglomerates alike pay their top talent in Restricted Stock Units (RSUs). If the stock price ascends to astronomical heights, distributing granular bonuses becomes a logistical nightmare for human resource departments. Splitting the stock allows for smoother compensation packages. But honestly, it's unclear if this genuinely helps long-term talent retention or if it just keeps the accountants sane. Experts disagree on whether the subsequent short-term stock pump is caused by retail FOMO or these structural corporate benefits.

How a 3 for 1 Split Diverges From Other Corporate Actions

To truly grasp a 100 shares 3 for 1 stock split, we must compare it to its financial cousins. A standard forward split is often confused with a reverse stock split, which is a completely different beast altogether. When a struggling penny stock tries to avoid getting delisted from the New York Stock Exchange because its price fell below $1.00, it executes a reverse split. It consolidates shares to artificially inflate the price. That is usually a massive red flag signaling distress, whereas a 3 for 1 forward split is almost universally a victory lap celebrating immense corporate growth.

Comparing Splits to Stock Dividends

Then we have stock dividends, which sound similar but operate under different legal frameworks. In a stock dividend, the company distributes additional shares to shareholders, but they fund this by shifting money from retained earnings into paid-in capital. As a result: the accounting treatment is completely distinct, even if the end user’s brokerage account looks identical. In short, while a stock split is a pure administrative reorganization of equity, other methods of share dilution or consolidation alter the fundamental structure of the corporate treasury.

Common Myths Shattered: Where Retail Investors Stumble

The Illusion of Sudden Affluence

You wake up, glance at your brokerage account, and notice your share count skyrocketed from 100 to 300 overnight. For a fleeting second, your brain screams that you just tripled your net worth. It is a beautiful delusion. Let's be clear: a 100 shares 3 for 1 stock split does not inject a single cent of real value into your portfolio. Think of it as slicing a single, decadent chocolate cake into three separate pieces instead of eating it whole. The volume of cake remains identical. Your actual equity slice stays exactly the same size. Investors frequently mistake liquidity for intrinsic value creation, which explains why amateur traders often flood forums with confused panic when the nominal price drops by two-thirds.

Chasing the Post-Split Ghost

Another classic blunder involves the desperate scramble to buy a stock immediately before the split date. Why do people do this? They falsely assume that the corporate announcement acts as a guaranteed catalyst for an endless upward trajectory. The problem is that the market efficiently prices in this psychological circus weeks in advance. Historical data indicates that the real momentum usually happens between the initial announcement and the actual execution date, not after. If you purchase shares at the absolute peak of the hype cycle, you might find yourself holding an overvalued asset. The underlying mechanics of a triple share multiplication event do not alter corporate cash flows, debt obligations, or revenue streams.

The Hidden Mechanics: An Institutional Perspective

Liquidity Voids and Options Market Distortions

While the financial press treats these corporate actions as mere psychological theater for retail investors, institutional desks view them through a completely different lens. The issue remains that a 100 shares 3 for 1 stock split radically alters the options landscape. Suddenly, your standard options contracts—which represent 100 underlying shares—undergo a massive transformation. The strike prices are divided by three, while the number of contracts you hold is multiplied by three. This sudden influx of contracts can temporarily disrupt local liquidity pools. High-frequency trading algorithms must immediately recalibrate their risk parameters to handle the new nominal pricing structure, which sometimes triggers brief pockets of heightened volatility. Did you know that options market makers frequently adjust their spreads wider during the exact transition window to shield themselves from this exact algorithmic chaos?

Frequently Asked Questions

Does a 3-for-1 split trigger an immediate capital gains tax liability?

Absolutely not, because the internal revenue service does not view this structural adjustment as a taxable realization event. When your 100 shares morph into 300 shares, no capital has changed hands, nor have you received any cash distributions. Your total cost basis is simply redistributed across a larger pool of equities, meaning if your original 100 shares had a cost basis of $150 per share, your new 300 shares will carry a adjusted cost basis of exactly $50 per share. As a result: you will only owe taxes when you eventually decide to sell these newly minted shares and realize a concrete capital gain or loss. Maintaining meticulous records of these adjusted cost bases is paramount for accurate portfolio tracking over long-term horizons.

How does this specific corporate action alter future dividend payments?

The total cash amount flowing into your bank account from dividends remains completely unchanged despite the dramatic surge in your overall share count. If a corporation previously distributed a dividend of $1.50 per share annually on your original 100 shares, they will seamlessly recalibrate the payout to exactly $0.50 per share on your new 300 shares. Consequently, your annual passive income remains perfectly static at exactly $150.00 in total cash received. Companies do this to prevent their cash reserves from being completely obliterated by the tripling of outstanding shares. Any deviation from this exact mathematical recalibration would signal a major, unexpected shift in corporate dividend policy.

Can fractional shares participate in a 100 shares 3 for 1 stock split?

Modern brokerage infrastructure easily processes these adjustments for fractional holdings, yet the exact execution depends entirely on your specific broker's internal policies. If you happened to own 100.5 shares prior to the split, the integer portion effortlessly converts into 300 shares while the fractional component scales up to 1.5 shares. Except that certain legacy brokerages refuse to hold fractional units post-split and will instead automatically liquidate that 0.5 fraction, distributing the cash equivalent directly to your account balance. (This automated cash-in-lieu liquidation process can actually trigger a tiny, unexpected taxable event for that specific fractional sliver). You should always review your firm's specific terms regarding corporate actions to avoid minor accounting surprises.

The Final Verdict on Share Tripling

Let us stop pretending that stock splits are revolutionary financial miracles. They are administrative, psychological cosmetic surgeries designed to make high-flying equities look more palatable to the investing masses. We firmly believe that fixating on a 100 shares 3 for 1 stock split as a core investment thesis is a dangerous distraction from what actually matters. Look at the balance sheet, examine the free cash flow, and ignore the numerical smoke and mirrors. If a company is fundamentally flawed, tripling the share count merely creates three times as many pieces of junk. Conversely, if the enterprise is a compounding machine, the split is just a polite invitation for smaller investors to join the ride. Treat these events as the corporate housekeeping chores they truly are, and your portfolio will be far safer in the long run.