Demystifying the Share Split: What Actually Happens When the Pie Gets Sliced?

Wall Street loves a good optical illusion, and share splits are the grandest of them all. When a board of directors announces a split—say, a 7-for-1 or a 10-for-1 maneuver—nothing changes in the corporate machinery. The market capitalization stays identical. The underlying earnings yield remains locked. Yet, the psychological shift among retail traders is seismic because humans are hardwired to prefer buying whole items over fractions.

The Math of Pure Optical Adjustments

Let us look at the raw mechanics. If you hold one share of a tech giant trading at $1,000, and the company executes a 10-for-1 split, you suddenly own ten shares valued at $100 each. Your total investment value remains precisely $1,000. The thing is, your slice of the corporate pie shrunk in size, but you now have more slices. Think of it like cutting a large pizza into sixteen pieces instead of eight; you do not magically get more food, yet the plate looks completely different. For decades, institutional trading desks treated these corporate actions as back-office bookkeeping chores, nothing more. But the retail market views this through a vastly different lens, transforming a simple accounting adjustment into an aggressive buy signal.

The Psychological Anchoring of a "Cheap" Price

Why do we care? Because of human bias. Investors routinely confuse a low stock price with a cheap valuation. When a high-flying stock drops from $900 to $90 overnight via a split, it triggers a powerful cognitive mechanism known as anchoring. Traders remember the old $900 price tag, look at the new $90 sticker, and instinctively perceive the equity as an absolute bargain. It feels attainable now. You can suddenly sell covered calls or buy round lots of 100 shares without emptying your entire retirement account, and that accessibility changes everything.

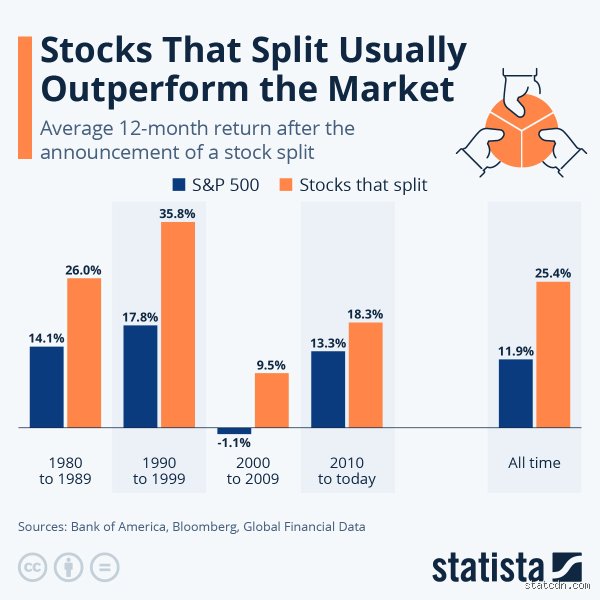

The Post-Split Surge: Unpacking the Hidden Drivers of Capital Appreciation

The historical data is clear, yet people don't think about this enough: companies that split their stock tend to outperform the broader market significantly during the subsequent twelve months. A landmark study by Bank of America Global Research analyzed decades of corporate actions and discovered that split stocks posted an average return of 25.1% in the year following the announcement, compared to just 9.1% for the broader S&P 500 index. That is not a minor statistical anomaly; it is a massive, repeatable performance gap.

The Liquidity Squeeze and Options Market Chaos

Where it gets tricky is inside the derivatives market. When a stock price drops into a double-digit or low triple-digit range, options contracts become exponentially more affordable for the average retail trader. Instead of paying thousands of dollars in premium for a single call option contract on a stock trading at $1,200, a trader might only need $150 post-split. This triggers a massive influx of speculative call buying. To hedge these positions, market makers are forced to aggressively buy the underlying shares, creating a powerful feedback loop known as a gamma squeeze that forces the equity price upward. Retail option volume frequently doubles in the weeks following a split execution, acting as a high-octane accelerant for the share price.

The Institutional Index Inclusion Factor

But we are far from describing just a retail phenomenon. There is another structural catalyst at play here: index tracking. Take the price-weighted Dow Jones Industrial Average, for example. Because the index calculates its value based on share price rather than total market capitalization, an elite company trading at $500 per share wields too much distortive power to be included in the index. When Apple executed its 4-for-1 split in August 2020, or when Amazon did its 20-for-1 split in June 2022, it suddenly made their share prices digestible for price-weighted indices. The issue remains that institutional fund managers benchmarking against these specific indices must adjust their holdings, creating massive institutional buying pressure that props up the stock long after the initial announcement excitement fades.

The Signaling Effect of Corporate Confidence

I am firmly convinced that a split is ultimately a loud, proud signal of corporate health. Boards do not split stocks that are crashing or stagnant. They split equities that have experienced multi-year bull runs and possess strong forward earnings guidance. The announcement itself serves as a public declaration by management that they expect the share price to keep climbing, which explains why the market treats the news as an validation of fundamental strength.

Historical Precedents: Evaluating the Heavyweights of the Split Era

To truly understand how this plays out in the real world, we must examine the specific trajectories of mega-cap companies that weaponized this corporate strategy to fuel their market dominance. The results are rarely uniform, which is precisely why blindly buying every split announcement is a dangerous game.

Nvidia’s Historical Runs in Santa Clara

Look at Nvidia. In May 2021, the AI chipmaker announced a 4-for-1 stock split when the shares were trading around $600. By the time the split took effect in July 2021, the stock had already surged past $750 on sheer anticipation. Fast forward to May 2024, and Nvidia pulled the lever again, announcing a massive 10-for-1 split after crossing the historic $1,000 threshold. On both occasions, the pre-split run-up outperformed the post-split execution phase, proving that savvy investors often sell the news once the actual split occurs.

Tesla’s High-Beta Volatility in Austin

Tesla’s relationship with splits is even more chaotic. In August 2020, Elon Musk’s electric vehicle pioneer announced a 5-for-1 split, sending the stock skyrocketing 81% between the announcement and the actual execution date. It was pure speculative mania. When they did it again with a 3-for-1 split in August 2022, the macroeconomic environment had soured, and the post-split performance was plagued by broader tech sector sell-offs. This proves that a split cannot save a stock if the macroeconomic tide is rolling out.

Strategic Alternatives: Why Some Giants Refuse to Slice the Cake

Yet, some of the most successful corporations on earth completely reject this playbook. They view the entire process as a cheap marketing gimmick that attracts short-term speculators rather than long-term owners.

The Berkshire Hathaway Philosophy in Omaha

Warren Buffett has famously refused to ever split Berkshire Hathaway’s Class A shares, which currently trade at a mind-boggling price of over $600,000 per single share. Why? Because Buffett deliberately wants to maintain a high barrier to entry. He believes that a high stock price attracts long-term, value-oriented shareholders who view themselves as true partners in the business, rather than fickle day traders looking to flip a position for a quick ten percent gain. Hence, the refusal to split becomes a tool for shareholder curation.

The Rise of Fractional Share Trading Technology

Except that the modern fintech revolution has made the traditional stock split somewhat obsolete anyway. With modern brokerage apps allowing investors to purchase as little as $1 worth of any stock, the physical share price matters less than it ever has in market history. If you can buy 0.001 shares of Alphabet or Microsoft with the swipe of a thumb, why should a corporate board spend millions of dollars in legal and administrative fees to adjust their share count? Honestly, it's unclear whether splits will retain their psychological magic over the next decade as fractional investing becomes the global standard, but for now, the market's irrational reaction to these announcements remains a highly profitable inefficiency for those who know how to time the waves.

Common mistakes and dangerous psychological traps

The "cheap stock" illusion

Retail investors look at a $3,000 share price, watch it transform into $30 overnight via a 100-for-1 split, and suddenly experience an overwhelming urge to buy. They genuinely believe the asset just became a bargain. Let's be clear: you are not getting a discount. The total market capitalization of the firm has not budged by a single penny. It is the exact same financial pie, just sliced into microscopic slivers. Yet, the human brain is hardwired to mistake nominal cheapness for actual value. When Apple or Nvidia execute these maneuvers, uneducated capital floods the order books, driving temporary, artificial momentum that usually evaporates once reality reasserts its grip.

Ignoring the post-split hangover

Everyone focuses on the massive announcement rally. But what happens after the initial euphoria fades? Statistically, a pronounced cooling-off period frequently materializes within three to six weeks following the actual distribution of new shares. Investors who chase the asset on the exact day of the split often find themselves holding a heavy bag. Why does this happen? The issue remains that the event itself acts as a classic liquidity catalyst. Institutional players use the localized surge in retail buying volume to quietly distribute their own massive positions, taking profits while enthusiastic amateurs provide the necessary exit liquidity.

Confusing causation with simple correlation

Do stocks usually go up after a split because of the split itself? Absolutely not. This is perhaps the most pervasive misconception on Wall Street. A corporate board only greenlights a division of shares because the underlying business is already firing on all cylinders. The soaring stock price is the symptom of stellar earnings growth, robust profit margins, and dominant market share. The split is merely a cosmetic celebration of that pre-existing operational success. If a failing, deeply indebted enterprise splits its stock to look more accessible, the market will mercilessly punish it anyway.

The liquidity mirage and institutional reality

How market makers exploit your enthusiasm

While the financial press pushes the narrative of democratization, institutional trading desks view these events through a completely different lens. A lower nominal share price alters the entire microstructure of the order book. Bid-ask spreads often widen in percentage terms relative to the absolute stock price, which subtly increases the transactional friction for smaller accounts. Which explains why high-frequency trading firms absolutely love these corporate actions. They profit immensely from the amplified retail volume and increased volatility. For the average investor, this means you are entering an environment specifically optimized to extract micro-pennies from your trades via sophisticated market-making algorithms.

The behavioral arbitrage strategy

If you want to trade these events like a professional, you must invert the common narrative. Instead of buying the actual execution date, seasoned portfolio managers often execute a behavioral arbitrage strategy. They look for fundamentally flawless companies that possess high nominal share prices but have not yet announced any corporate restructuring. By entering these positions early, you capture the true organic business growth. If a split happens later, you reap the announcement bonus as a pure windfall. The problem is that most retail traders do the exact opposite, buying at the absolute peak of public awareness when the risk-reward ratio has become completely unfavorable.

Frequently Asked Questions

Does a forward stock split change the intrinsic value of my investment portfolio?

No, your total economic stake remains completely unchanged. If you own 10 shares of an enterprise priced at $500 each, your total position is worth exactly $5,000. Following a 5-for-1 corporate action, you will suddenly own 50 shares, but the market price will simultaneously adjust downward to $100 per share. The underlying equity value stays mathematically identical at $5,000. Historical data from major market cycles confirms that nominal price adjustments bear zero mathematical relationship to a corporation's discounted cash flows or book value. It is a purely cosmetic accounting modification designed to alter human perception rather than corporate balance sheets.

How do options contracts adjust when a corporation decides to split its shares?

The Options Clearing Corporation automatically restructures all outstanding derivative contracts to ensure absolute economic neutrality. For instance, if you hold a single call option with a strike price of $200 before a 2-for-1 split, your position automatically converts into two separate call options. Each of these new contracts will possess a modified strike price of $100, while the standard underlying deliverable remains 100 shares per contract. Empirical trading metrics indicate that implied volatility frequently spikes during the immediate transition window. This occurs because market participants scramble to reprice their derivative leverage, creating temporary pricing inefficiencies that savvy options traders frequently exploit for short-term gain.

What is the typical historical performance of equities in the year following these events?

Extensive quantitative research covering large-cap equities over the past four decades reveals a fascinating statistical trend. On average, companies that split their shares outperform the broader S&P 500 index by roughly 4.8 percent during the subsequent twelve-month window. However, this outperformance is heavily front-loaded into the first ninety days following the initial public announcement. As a result: the long-term upward trajectory is almost entirely driven by the company's superior underlying earnings power rather than the mechanical split itself. Furthermore, during secular bear markets, this historical premium completely vanishes, proving that macro economic headwinds easily overpower any positive psychological sentiment generated by nominal price reductions.

The definitive verdict on corporate share divisions

Stop treating these cosmetic corporate restructurings as a magical wealth-generation mechanism. The obsession with nominal share prices is a distracting sideshow that diverts your attention away from what actually moves capital markets. We must realize that a stock split is a lagging indicator of past corporate glory, never a guaranteed predictor of future investment returns. If you buy an equity solely because the board decided to chop its shares into smaller pieces, you are essentially gambling on pure psychological momentum. Real wealth is compounded by identifying enterprises with unassailable competitive moats, exceptional return on invested capital, and robust free cash flow. Focus your analytical energy on those hard operational metrics, ignore the media circus surrounding stock splits, and let the superficial nominal math take care of itself.