The Hidden Mechanics of the Insurance of Insurance Companies

Most corporate risk managers look at premium costs but ignore the plumbing. Reinsurance is simply insurance for insurance companies, a mechanism where a primary insurer—the ceding company—transfers a chunk of its liability portfolio to a reinsurer. But people don't think about this enough: without this secondary market, a single Category 5 hurricane hitting Miami would instantly bankrupt dozens of domestic carriers. By spreading the financial shock across global balance sheets from Zurich to Bermuda, the industry maintains liquidity. The issue remains that the interface between these layers is notoriously complex, governed by bespoke contracts that blend actuarial science with high-stakes corporate finance.

Why the Underwriting Floor Needs a Backstop

Let us look at the numbers. The global reinsurance capital market hovered around $570 billion in recent years, a massive war chest designed specifically to absorb aggregate losses. When a primary insurer writes policies for thousands of coastal homes, it creates a dangerous geographic concentration of risk. If a catastrophic event occurs, the cash outflow can easily exceed the primary carrier's liquid reserves. Here, the reinsurer steps in, acting as a financial shock absorber that injects liquidity precisely when the ceding company's solvency ratio is threatened. But the thing is, this relationship is not a simple charity pool; it is a hard-nosed commercial transaction driven by strict capital requirements like Europe's Solvency II directive.

The Friction Point: Ceding Commission and Underwriting Authority

Where it gets tricky is the alignment of incentives. When an insurer passes risk downstream, it often receives a ceding commission from the reinsurer to cover administrative and acquisition costs. This creates a moral hazard. Why should the primary insurer care about strict underwriting standards if the reinsurer picks up the pieces? To fix this, modern agreements use complex profit-sharing clauses and strict retention limits. It is a delicate dance of trust and data verification, which explains why reinsurers employ some of the most cynical, data-driven minds in the financial world to audit the books of their ceding partners before signing off on a single dollar of coverage.

Diving Into Facultative Structures: The Bespoke Risk Selector

When analyzing what are the four types of reinsurance, we must start with the most granular approach: facultative reinsurance. This is a transaction-by-transaction arrangement where the reinsurer evaluates a single, specific policy—such as a $200 million offshore oil rig in the North Sea or a historic skyscraper in Manhattan—and retains the absolute right to accept or reject that specific risk. There is no blanket coverage here. It is the artisan tailoring of the reinsurance world, highly labor-intensive and incredibly specific. Yet, despite its high transactional costs, it remains an indispensable tool for primary insurers who find themselves holding a hot potato that exceeds their standard underwriting guidelines.

The Freedom of Individual Risk Assessment

Think of facultative coverage as a selective shield. A local insurer might have a fantastic commercial property portfolio, except that one of their long-term clients decides to build a massive, high-hazard chemical processing plant in Houston. The insurer does not want to lose the entire account, but keeping that explosive liability on their own books would be suicidal. By using a facultative certificate, they can isolate that specific chemical plant, shop it around to global reinsurers, and secure a dedicated layer of protection just for that single asset. It is expensive, sure, but it allows the primary carrier to maintain its customer relationship without jeopardizing its entire corporate stability.

The Operational Burden of Case-by-Case Underwriting

But we are far from an efficient market when it comes to this specific method. Because every single contract requires manual review, negotiation, and pricing, the administrative drag is immense. Actuaries must pour over blueprints, historical weather data, and specific engineering reports. (And heaven forbid the corporate client changes the building design midway through construction!) This administrative bottleneck is precisely why facultative placement is reserved for the outliers—the massive, irregular, or extraordinarily hazardous risks that simply refuse to fit into neat, standardized corporate boxes.

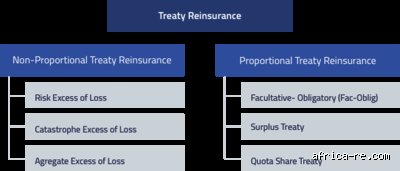

Treaty Reinsurance: The Automated Bulk Absorption Engine

If facultative underwriting is a scalpel, treaty reinsurance is a massive industrial earthmover. This second structural type involves a broad, overarching contract where the reinsurer agrees to automatically accept a pre-defined category of risks written by the primary insurer. For example, a treaty might dictate that the reinsurer will cover 30% of every single homeowners' policy the ceding company writes in the state of California over a twelve-month period. There is no case-by-case vetting. The reinsurer trusts the primary company's underwriting guidelines blindly, binding themselves to thousands of individual policies with a single signature, which completely changes everything regarding operational scale.

The Power of Forward-Looking Portfolio Alignment

This automation offers unprecedented speed. Primary underwriters can aggressively write new business on the ground, knowing instantly that every policy hitting their system is automatically backed by global capital. For instance, during the massive construction boom in Phoenix in 2024, local insurers could rapidly issue thousands of commercial liability policies because their treaty contracts automatically absorbed the excess exposures. The reinsurer does not get a say in individual cases; they are locked into the portfolio's destiny for better or worse.

When Underwriting Blindness Leads to Systemic Loss

Is this hands-off approach actually safe? Honestly, it's unclear until a major catastrophe hits and the data rolls in. If the primary insurer's ground-level agents get sloppy and start approving substandard risks just to chase market share, the treaty reinsurer gets dragged into the abyss right along with them. This systemic vulnerability explains why treaty contracts are packed with strict underwriting boundaries, geographical limits, and mandatory audits. Reinsurers will routinely send teams of forensic accountants to the ceding company's headquarters to ensure that the risks being funneled into the treaty actually match the parameters agreed upon during the initial negotiation phase.

Proportional vs Non-Proportional: The Financial Allocation Divide

To fully grasp what are the four types of reinsurance, one must understand that facultative and treaty contracts are always executed through either a proportional or a non-proportional financial framework. This is the crossroads where the actual math of loss-sharing is determined. In a proportional setup—often called quota share or surplus lines—the reinsurer takes a fixed percentage of the premiums and, in return, pays that exact same percentage of all incurred claims. It is a symbiotic partnership of shared fate. Non-proportional reinsurance, conversely, operates on an excess-of-loss basis where the reinsurer only pays if a claim, or an aggregate pool of claims, breaches a specific, high-dollar threshold.

Proportional Dynamics and the Search for Premium Volume

Consider a 40/60 quota share proportional treaty. If the primary insurer collects a $1,000 premium for a commercial auto policy, they pass $600 directly to the reinsurer. If that same vehicle crashes and causes $50,000 in property damage, the reinsurer cuts a check for $30,000 without argument. This structure is beautifully simple, making it highly attractive for younger insurance companies that need to conserve cash and rapidly boost their writing capacity without violating regulatory leverage ratios. As a result: the primary company gets to act much larger than its balance sheet would normally allow, leaning heavily on the deeper pockets of its global partner.

The Excess-of-Loss Threshold and Catastrophic Protections

Non-proportional structures throw this symmetry out the window. Here, the reinsurer says: "We will not give you a dime for ordinary claims, but if a single disaster costs you more than $5 million, we will cover the next $20 million of that loss." This is where things get fiercely competitive. The premium paid for this excess coverage is not a clean percentage of the base policy; it is an independently calculated price based on complex probabilistic catastrophe modeling. Sharp opinion dictates that non-proportional layers are the true battleground of modern risk management, where reinsurers place massive bets against mother nature, relying on complex mathematical simulations to ensure they do not misprice the catastrophic layers that could obliterate their quarterly earnings.

Common Pitfalls and Misconceptions in Risk Transfer

The Illusion of Total Indemnity

Many primary underwriters believe purchasing reinsurance completely absolves them of the original policy liability. Let's be clear: it does not. The primary insurer remains solely liable to the policyholder. If your reinsurer becomes insolvent after a catastrophic hurricane, you still have to pay the claims. This is why credit risk management is a major part of evaluating reinsurance partners.

Confusing Facultative and Treaty Mechanics

Another frequent blunder involves treating treaty agreements like facultative placements. Treaty reinsurance automatically covers an entire block of business, meaning individual risk underwriting is bypassed. Conversely, facultative certificates require specific negotiation for every single policy. Mixing these up leads to dangerous coverage gaps or expensive administrative overhead. Why do smart actuaries still make this mistake? It usually comes down to poor communication between the underwriting and risk management departments.

Mispricing the Retention Limit

Setting the retention limit too low drains premium income unnecessarily. Set it too high, and a single bad quarter wipes out your capital surplus. In 2024, a mid-sized property insurer collapsed because they retained a 15% share of a commercial property portfolio rather than the modeled 5% safety threshold. They misjudged their aggregate exposure to convective storms, which explains their rapid insolvency.

Advanced Capital Optimization and Expert Advice

The Arbitrage of Retrocession Markets

Reinsurers need their own protection, a mechanism known as a retrocession treaty. This creates a complex global secondary market where risk is sliced, diced, and packaged. As an expert, my advice is to look closely at where your reinsurer buys its own retrocession. If they are over-leveraged in the collateralized catastrophe bond market, their long-term stability during a prolonged hard market is highly questionable.

Leveraging Parametric Triggers

Traditional indemnity contracts require long, painful claims adjustment processes. To optimize your capital, consider blending standard structures with parametric reinsurance. Instead of proving actual losses, payment triggers automatically when a specific metric is met, such as wind speeds exceeding 130 miles per hour. This injects liquidity into your balance sheet within days rather than months.

Frequently Asked Questions

What are the four types of reinsurance and how do they impact an insurer's combined ratio?

The four types of reinsurance—facultative, treaty, proportional, and non-proportional—directly dictate the volatility of an insurance company's combined ratio. Proportional structures, like a 40% quota share, reduce the ratio by lowering the net retained premium while providing a ceding commission that offsets internal acquisition expenses. Non-proportional arrangements, such as excess of loss, protect the ratio against catastrophic spikes by capping the maximum loss from a single event at a predetermined retention level, say 5 million dollars. Data from global rating agencies indicates that insurers utilizing an optimized mix of these four types of reinsurance maintain combined ratios that are 8% more stable than peers relying solely on quota share agreements. As a result: strategic deployment of these instruments is a requirement for capital stability.

How does inflation affect non-proportional reinsurance treaties?

Inflation acts as a silent killer on excess of loss layers because of an effect known as severe claim leveraging. If an insurer retains a 1 million dollar limit and a claim inflates from 900,000 dollars to 1.2 million dollars, the primary insurer's loss remains capped at 1 million, but the reinsurer suddenly faces a 200,000 dollar liability. This represents an infinite percentage increase for the reinsurer on that specific policy. Because of this dynamic, reinsurers aggressively adjust attachment points upward during inflationary cycles to protect their margins. Yet, many primary carriers fail to index their retention limits, leaving themselves exposed to high frequencies of smaller claims that previously would not have breached the treaty threshold.

Can a startup insurance company survive without utilizing proportional quota shares?

Surviving as an insurance startup without a robust quota share agreement is virtually impossible due to strict regulatory capital mandates. New entities lack the deep surplus pools required to absorb the initial premium strain caused by upfront customer acquisition costs. A typical 50% quota share treaty allows the startup to pass half of its underwriting risk and premium to a highly rated global partner. In return, the startup receives a ceding commission, which frequently ranges between 20% and 30% of the ceded premium. The issue remains that without this immediate capital relief, statutory leverage ratios would prevent the startup from writing new business before its first anniversary.

A Definitive Stance on Modern Risk Engineering

The global insurance landscape has outgrown the simplistic view that reinsurance is just an expensive corporate safety net. It is a dynamic capital deployment tool that determines whether an insurance company can scale or if it will fail under the weight of systemic volatility. Relying on legacy models to structure these complex agreements is no longer viable. We must stop viewing reinsurance as a passive annual purchase and instead treat it as a core component of active capital optimization. If you fail to aggressively negotiate and structure your corporate protections using sophisticated predictive analytics, you are essentially gambling with your solvency. The future belongs to insurers who can masterfully balance these risk mechanisms to out-underwrite their competition.