The Long, Painful Road to a Unified Global Balance Sheet

Before January 1, 2023, the global insurance sector was, frankly, a regulatory Wild West. Under the old interim standard, IFRS 4, a multinational giant like Munich Re or AXA could bundle its liabilities using historical assumptions that were sometimes decades old, leading to numbers that were completely incomparable across borders. Think about it. How can an investor accurately compare a life policy issued in Frankfurt with one written in Tokyo if both use entirely different discount rates and local legacy GAAP rules?

The Illusion of Predictable Profits

The thing is, the old system allowed companies to book profits upfront, hiding the true long-term risk of policies that might not mature for forty years. It was a comfortable illusion. Actuaries would lock in assumptions at inception, and unless things went catastrophically wrong, those numbers stayed frozen in time. But the economic reality of the 21st century—marked by prolonged periods of ultra-low interest rates and unexpected climate shocks—exposed this static approach as dangerously detached from market truths. IFRS 17 shatters this historical cost complacency by demanding a continuous, concurrent re-evaluation of every single contract portfolio.

Why the Transition Cost Billions and Sparked Industry Rage

This was never going to be a cheap software patch. Estimates suggest the global insurance industry spent well over $15 billion combined just to get their data pipelines ready for the official launch date. Why? Because the granularity required by the International Accounting Standards Board (IASB) meant pulling data from legacy IT systems built during the Cold War. Some experts still disagree on whether the staggering compliance cost was actually worth the trouble, and honestly, it’s unclear if smaller regional players will ever fully recover from the operational drain.

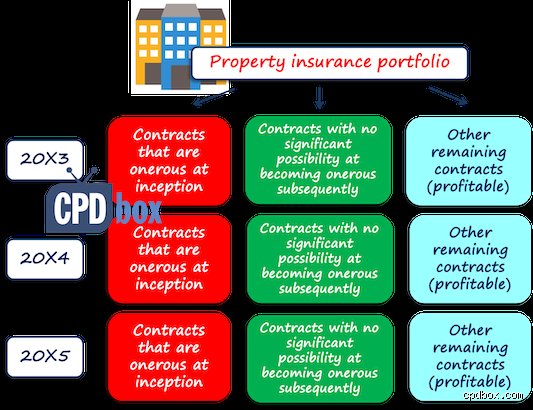

Diving into the Engine Room: The Three Core Valuation Models

Where it gets tricky is the actual calculation architecture. The IASB did not just introduce one way to look at a balance sheet; they built a complex, multi-tiered logic system designed to catch different types of risk profiles. You cannot look at a three-year car insurance policy the same way you look at a whole-of-life annuity, which explains why the standard introduces three distinct measurement models.

The General Measurement Model: The Default Beast

The General Measurement Model (GMM)—or the Building Block Approach as the purists prefer to call it—is the foundational pillar of IFRS 17. It relies on four distinct components: explicit estimates of future cash flows, a discount rate that reflects the time value of money, a explicit risk adjustment for non-financial risk, and the highly controversial Contractual Service Margin (CSM). That last element is the real game-changer. The CSM represents the unearned profit of a group of insurance contracts that the company will gradually release into the income statement as it provides insurance coverage over the years. If a portfolio looks like it will be loss-making from day one? You must recognize that onerous loss immediately. No hiding, no smoothing, no deferring.

The Premium Allocation Approach: A Welcome Life Raft

Thankfully, the rulemakers threw a bone to short-term insurers. If a contract is twelve months or less—think your typical annual home or auto policy—insurers can opt for the simplified Premium Allocation Approach (PAA). It looks a bit more like the old unearned premium model we all grew up with, except that you still have to discount those liabilities if claims take years to settle. But make no mistake: the PAA is not an automatic escape hatch, and the qualification criteria are deceptively rigid.

The Variable Fee Approach: For the Complex Wealth Managers

Then we have the Variable Fee Approach (VFA), designed specifically for direct participation contracts like unit-linked funds or with-profits policies common in the UK and European markets. Here, the policyholder effectively invests in a pool of assets, and the insurer takes a cut. Under the VFA, the Contractual Service Margin is dynamically adjusted to reflect changes in the insurer’s share of the fair value of those underlying assets. It sounds elegant in theory, but in practice, tracking these moving parts in real-time is an absolute nightmare for valuation teams.

The Radical Shift in Income Statement Presentation

Forget everything you know about traditional insurance income statements. The top-line metric that everyone used for a century—Gross Written Premiums—has been completely banished from the face of the primary financial reports. People don't think about this enough, but that changes everything for equity analysts who used to rank companies purely on premium volume.

The New Metric in Town: Insurance Revenue

Instead of Gross Written Premiums, we now have Insurance Revenue, which represents the expected claims and expenses provided during the period, plus the systematic release of the CSM profit margin. If a policyholder deposits money into an investment-linked policy, that savings component is strictly excluded from revenue. It is treated exactly like a bank deposit. After all, you wouldn't call it revenue when a customer puts money into their savings account, would you? This clean separation between pure insurance protection and pure investment components means the top line of major insurers suddenly looked significantly smaller on paper after 2023, even though their underlying economics remained unchanged.

How IFRS 17 Realigns Insurance with Global Banking Standards

To understand the bigger geopolitical picture, you have to look across the aisle at the banking sector. For years, banks have operated under IFRS 9, which forces them to look at financial instruments through a lens of current market prices and expected credit losses. IFRS 17 bridges the gap between banking and insurance accounting, bringing a unified philosophical approach to the entire financial services industry.

The Volatility Paradox

Yet, this alignment introduces a massive dose of earnings volatility. Because liabilities are now discounted using current market interest rates rather than artificial, locked-in assumptions, the balance sheet moves violently with every wiggle of the bond market. To mitigate this, companies must carefully coordinate their IFRS 17 liability measurements with their IFRS 9 asset valuations. If you misalign the two, your corporate earnings will look like a rollercoaster, even if your actual business is as stable as a rock. The issue remains that this artificial volatility can spook retail investors who don't understand the underlying mathematics, forcing corporate communications teams to spend hours explaining that a paper loss is not a real-world disaster.

Common mistakes and misconceptions about the standard

The illusion of a mere IT upgrade

Many executives looked at the new insurance contracts framework and assumed their actuarial software just needed a patch. They were wrong. This regulatory shift dismantles the entire accounting pipeline, requiring data granularity that legacy databases simply cannot compute. IFRS 17 implementation requires immense architectural overhauls because you must track profitability at a cohort level rather than aggregating entire portfolios. The problem is that finance teams and IT specialists speak entirely different languages. Actuaries produce stochastic distributions; accountants demand balance sheets that tie out to the penny. If you treat this transition as a simple software installation, your systems will likely crash under the sheer weight of millions of daily cash flow calculations.

Confusing CSM with immediate profit

Let's be clear about the Contractual Service Margin. It is not an open checkbook for your current quarter. Some analysts mistakenly believe that writing billions in new premiums translates directly to an immediate spike in the bottom line under IFRS 17 rules for insurance entities. Except that the framework explicitly forbids this. The CSM represents unearned profit that must be systematically released over the coverage period as services are provided. If an insurer writes a twenty-year life policy with a projected margin of ten million dollars, they cannot recognize that gain today. It trickles into the income statement slowly. And what happens if the risk profile deteriorates next year? The group becomes onerous, forcing the company to recognize the entire loss instantly on the income statement, creating massive earnings volatility.

The hidden volatility trigger and expert advice

The discounting trap in volatile markets

Everyone talks about the transparency of the balance sheet, yet the market risk embedded in the discount rates remains a ticking time bomb. Under the historical approach, insurers could lock in assumptions and smooth out market fluctuations over decades. Now, IFRS 17 financial reporting requirements dictate that fulfillment cash flows must be discounted using current, market-consistent rates at every single reporting date. This means a minor fifty-basis-point drop in long-term sovereign bond yields can overnight inflate your insurance liabilities by hundreds of millions of dollars. Which explains why your net income might swing wildly from one quarter to the next, even if your underlying underwriting quality remains perfectly stable.

Expert advice: Embrace the Premium Allocation Approach where possible

Is there a way to escape this mathematical nightmare? Our strongest recommendation for compliance teams is to aggressively leverage the Premium Allocation Approach for short-duration contracts. The PAA is a simplified measurement model, closely resembling the old unearned premium reserve method. If your coverage period is twelve months or less, you qualify automatically. But here is the secret weapon: even for longer contracts, if you can prove that the PAA output does not materially differ from the complex General Measurement Model, you can use it. Do the math early. Investing in a rigorous materiality assessment can save your organization thousands of hours of actuarial modeling, drastically reducing operational overhead.

Frequently Asked Questions

How does the standard impact Key Performance Indicators like the combined ratio?

The traditional combined ratio used by property and casualty insurers has been completely disrupted. Under IFRS 17 accounting standards, insurance revenue excludes investment components and deposits, which slashes the denominator of your traditional metrics by up to thirty percent in certain savings-heavy products. Furthermore, claims are now discounted, meaning a long-tail liability line will show a significantly lower initial loss ratio than under old frameworks. Finance teams must completely recalibrate their internal dashboards because a historical target of ninety-five percent might now equate to an eighty-eight percent ratio under the new math. As a result: comparing a company's performance across the 2023 transition boundary requires a complete rebuilding of historical data sets.

What is the treatment of reinsurance contracts held?

Reinsurance can no longer be net against gross insurance liabilities on the face of the balance sheet. The standard demands that reinsurance contracts held be accounted for entirely separately from the underlying direct insurance contracts, using distinct assumptions and cash flow projections. This separate measurement means that if a direct portfolio becomes onerous, you must recognize the loss immediately, while the offsetting reinsurance recovery can only be recognized if the reinsurance contract itself covers those specific losses. The issue remains that a mismatch in contract boundaries between your direct business and your treaty reinsurance can create artificial losses. Why? Because the timing of recognition for reinsurance cash flows does not perfectly mirror the underlying risk release, forcing CFOs to explain complex accounting asymmetries to frustrated board members.

How does this framework alter the volatility of equity for life insurers?

Equity volatility has intensified dramatically due to the market-consistent valuation of long-term liabilities. When interest rates fluctuate, the valuation of insurance liabilities moves in the opposite direction, creating a direct impact on the equity bridge unless an organization utilizes the Other Comprehensive Income option. By electing the OCI option, an insurer can divert the impact of discount rate changes away from the profit and loss statement and park it directly in equity reserves. But this is merely a cosmetic fix (an accounting band-aid, if you will) because the underlying economic volatility remains exposed to savvy market analysts. Life insurers holding vast portfolios of long-duration annuities are experiencing equity fluctuations of up to fifteen percent quarter-over-quarter solely due to macro shifts rather than operational performance.

A definitive perspective on the new era

We need to stop viewing this standard as a burdensome compliance exercise imposed by overzealous regulators. It is an brutal, unforgiving mirror reflecting the true economic reality of long-term insurance risks. For decades, the insurance industry hid behind opaque local accounting rules that allowed weak performers to mask structural deficits through clever reserve smoothing. This framework strips away that comfort blanket, forcing corporate leaders to confront asset-liability mismatches in broad daylight. The transition phase is undoubtedly painful, expensive, and chaotic. Yet, the long-term benefit is a standardized global language that finally allows investors to compare an insurer in Munich directly with one in Tokyo without an army of forensic accountants. We believe the companies that embrace this transparency to optimize their product pricing, rather than just fighting the compliance clock, will dominate the global capital markets for the next generation.