The Anatomy of a REIT and Why the IRS Views It Differently

Wall Street sells REITs as effortless income. You buy a share of Vanguard Real Estate ETF (VNQ) or a single stock like Realty Income Corp (O) in April 2024, sit back, and watch the monthly checks roll into your Charles Schwab account. Except that changes everything when tax season hits. A normal corporation pays taxes at the corporate level, and then you pay taxes again on qualified dividends at a lower capital gains rate. REITs bypass this completely.

The 90 Percent Rule and the Tax Pass-Through Illusion

Because federal law mandates that these entities distribute at least 90% of their taxable income to shareholders annually, the IRS treats them as pass-through entities. The issue remains that this untaxed corporate income lands squarely in your lap as ordinary income. Have you ever wondered why your standard brokerage statements arrive so late in February? It is because REIT accountants are frantically calculating what percentage of your 2025 distribution was actual profit and what percentage was just paper depreciation being handed back to you.

Ordinary Income vs. Return of Capital

This is where people don't think about this enough. A single payment from a REIT can be sliced into three distinct tax buckets: ordinary dividends, capital gains, and Return of Capital (ROC). Ordinary dividends get taxed at your standard federal bracket, which could be as high as 37%. Conversely, the Return of Capital portion isn't taxed today at all; instead, it reduces your cost basis in the stock, deferring the tax hit until you sell the asset. It is a brilliant mechanism, yet it turns your bookkeeping into a living nightmare over a ten-year holding period.

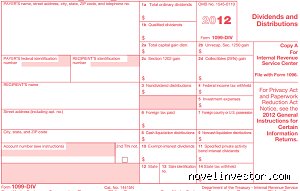

Navigating Form 1099-DIV: Where the Numbers Actually Land

When your brokerage finally publishes your consolidated 1099 in mid-February, your eyes must instantly dart to Form 1099-DIV. Do not just look at the total summary. You need the granular breakdown because each box dictates a completely different destination on your 1040.

Box 1a and the Schedule B Destination

Total ordinary dividends live in Box 1a. If your total ordinary dividend income across all investments exceeds $1,500 for the tax year, you are legally required to list the payer’s name and the exact amount on Schedule B, Part I. But wait. Look closely at Box 1b for qualified dividends. With traditional stocks like Apple or ExxonMobil, Box 1a and Box 1b match almost perfectly. With REITs? Box 1b will almost always be zero or a shockingly low number. Why? Because the underlying earnings were never taxed at the corporate level, meaning you cannot claim the preferential 0%, 15%, or 20% capital gains tax rates. You are paying full freight.

The Section 199A Deduction Jackpot in Box 5

Here is where it gets tricky, and frankly, where most DIY taxpayers leave massive amounts of money on the table. Look at Box 5, labeled Section 199A dividends. Thanks to the Tax Cuts and Jobs Act of 2017, investors can deduct up to 20% of their qualified business income, including REIT dividends. If you have $5,000 listed in Box 5, you don't just copy that onto Schedule B. That specific figure must migrate over to Form 8995 or Form 8995-A to calculate your qualified business income deduction before it ever touches Line 12 of your Form 1040. Honestly, it's unclear why the IRS didn't build a direct bridge between these forms, leaving millions of self-preparers completely oblivious to a deduction that slashes their taxable REIT income by a fifth.

Unrecaptured Section 1250 Gains in Box 2b

Sometimes a REIT sells a skyscraper in Chicago or a logistics hub in Atlanta for a massive profit. When that happens, you might see an amount pop up in Box 2b, which represents Unrecaptured Section 1250 gain. This reflects the real estate depreciation that the trust claimed in previous years. When you see a number here, it has to find its way to the Unrecaptured Section 1250 Gain Worksheet in the instructions for Schedule D. It is taxed at a maximum rate of 25%, which is better than ordinary income rates but worse than long-term capital gains. We are far from a simple copy-and-paste job here.

The Impact of Account Type on Your Reporting Strategy

The entire conversation shifts dramatically based on the virtual walls surrounding your investments. Where to put REITs on a tax return becomes a completely irrelevant question if you played your cards right during the asset allocation phase of your portfolio construction.

The Blissful Isolation of Roth and Traditional IRAs

If your REIT shares reside inside a tax-advantaged wrapper like a Traditional IRA, a Roth IRA, or a 401k managed through Fidelity, your April workload drops to zero. The 1099-DIV won't even be generated by your broker. You do not report the dividends, you do not fill out Schedule B, and you do not worry about Section 199A deductions. The income grows completely shielded from the IRS. I strongly advocate for keeping high-yield mortgage REITs like Annaly Capital Management (NLY) strictly inside retirement accounts for this exact reason, though conventional financial wisdom often screams that you should maximize foreign tax credits in those accounts instead.

The Taxable Brokerage Account Burden

But if you hold those same shares in a standard, taxable margin account because you want access to the liquidity? Every single dollar must be accounted for. Every line of that 1099-DIV must be systematically cross-referenced with your tax software. As a result: an investor holding $50,000 worth of commercial property trusts in a taxable account might find themselves filling out four additional tax schedules just to accommodate a few hundred dollars in quarterly distributions.

Comparing Publicly Traded REITs with Private Placement Real Estate Funds

It is worth stepping back to look at how these liquid public trusts stack up against their private, non-traded cousins. The tax documents they generate look like they belong to entirely different planets.

1099-DIV vs. Schedule K-1

Public REITs give you a clean, albeit complicated, 1099-DIV. Private real estate syndications or funds, such as those you might find on crowdfunding platforms, do not use Form 1099 at all. Instead, they issue a Schedule K-1 (Form 1065). While a 1099 arrives in February, a K-1 can routinely be delayed until late March or even September if the partnership files for an extension. A K-1 requires you to report passive income and losses across Schedule E, which is an entirely different beast than the Schedule B reporting used for public REITs. The compliance costs alone for handling three or four K-1 forms can quickly wipe out the yield advantages that private placements claim to offer over public markets.

Common Pitfalls and Misinterpretations

The Illusion of Ordinary Dividends

You glance at Box 1a of your Form 1099-DIV and assume everything belongs in standard investment income. That is a massive blunder. REIT distributions are not corporate dividends. Because these entities pay minimal corporate-level tax, Uncle Sam demands his pound of flesh from you instead. Labeling these as qualified dividends will immediately trigger an IRS automated underreporter flag. The problem is that software defaults often blindly dump these amounts onto Schedule B without separating the components. You must audit every line manually. If you fail to separate the non-qualified portions, you face a swift correction notice with penalties attached.

Ignoring the Return of Capital Mirage

Box 3 of that same form contains a ticking financial time bomb disguised as free cash. Nondividend distributions represent a return of your original capital, which means they are not currently taxable. Great news, right? Except that they silently erode your cost basis in the security. If you do not adjust your purchase price downward by this exact figure every single year, your future capital gains calculations will be completely wrong. Think your brokerage tracks this perfectly over twenty years? Let's be clear: they frequently drop the ball during mergers or account transfers, leaving you to piece together the forensic paper trail during a sale.

The Section 199A Breakthrough and Advanced Strategies

Unlocking the Section 199A Deduction

Did you know that Congress handed real estate investors a massive tax gift that many completely overlook? The Tax Cuts and Jobs Act introduced the Section 199A deduction, allowing individuals to exclude a chunk of their income from taxation. Specifically, you can deduct up to 20% of qualified REIT dividends directly on Form 1040, Line 15. The beauty of this mechanism lies in its accessibility. Unlike standard pass-through businesses, this deduction bypasses the complex wage and property limitations entirely. It applies whether you itemize deductions or take the standard path. Yet, millions of dollars vanish every season because self-directed filers do not know where to put REITs on a tax return to claim this specific benefit.

How do you actually capture it? The magic happens on Form 8995. You migrate the total from Box 5 of Form 1099-DIV straight to Part I of this form to calculate the final deduction. Can you imagine leaving a fifth of your real estate investment earnings exposed to the highest marginal tax brackets out of pure formatting negligence? (It happens more often than expensive CPA firms care to admit). If your total taxable income exceeds $191,950 for single filers, you must migrate to the far more complex Form 8995-A. Tracking these limits requires vigilant quarterly monitoring.

Frequently Asked Questions

Do foreign REITs qualify for the same advantageous tax treatments?

No, international property trusts do not receive identical treatment under the domestic tax code. If you hold Australian Property Units or British property trusts, those distributions fail the Section 199A deduction criteria entirely because they operate outside US jurisdictions. As a result: you will generally report these on Schedule B as ordinary income, completely ineligible for the 20% deduction. Furthermore, foreign governments frequently withhold statutory taxes ranging from 15% to 30% directly at the source. You must file Form 1116 to claim the Foreign Tax Credit to mitigate this double taxation, provided your total foreign taxes paid exceed the $300 single filer threshold. The issue remains that navigating international real estate tax treaties creates an administrative nightmare for average retail accounts.

What happens if my REIT shows a net operating loss on Form K-1?

Private or non-traded real estate trusts often utilize Form K-1 rather than the standard Form 1099-DIV, which introduces the restrictive passive activity loss rules. When your investment generates a net negative figure, you cannot use that loss to offset your salary, active business earnings, or standard portfolio income. Instead, these losses are strictly quarantined on Form 8582. They remain suspended in perpetual limbo until the specific trust generates positive passive income or you completely liquidate your entire interest in the property. Because of this structural lock, holding debt-heavy private trusts inside a taxable environment can severely restrict your current-year tax deduction strategies.

Is it better to hold these trusts in a Roth IRA to avoid the paperwork?

Sheltering these high-yield assets inside a Roth IRA eliminates the vast majority of your annual filing headaches. Because qualified retirement accounts are inherently tax-exempt, you do not need to worry about where to put REITs on a tax return since those annual Form 1099-DIV details are not reported on your individual filing. But a hidden trap known as Unrelated Business Taxable Income can completely ruin this strategy if you invest in master limited partnerships or certain leveraged private trusts. Should your aggregate UBTI across all retirement accounts exceed a strict $1,000 threshold, your IRA custodian must file Form 990-T. This forces the account itself to pay corporate-level taxes that top out at a staggering 37% rate on minimal income.

A Definitive Verdict on Real Estate Trust Taxation

Blindly trusting tax software to handle specialized real estate portfolios is a recipe for financial self-sabotage. The unique taxonomy of these real estate distributions requires manual oversight, meticulous form matching, and a deep understanding of Section 199A protocols. We must recognize that the tax code actively rewards precision while ruthlessly punishing administrative laziness. If you own these assets, take control of your asset location by prioritizing tax-advantaged accounts to shield ordinary income rates. When holding them in taxable accounts, verify every line of Form 8995 personally. In short, stop treating these dynamic investments like standard corporate stocks, or you will willingly overpay the government every April.