The Messy Reality Behind Financial Guardrails

Accounting is often masqueraded as an absolute science, like physics or geometry. But honestly, it's unclear why we pretend fiscal tracking is entirely objective when human judgment creeps into every single ledger entry. The truth is that financial records are a mix of strict math and structured guesswork. Back in 1494, when Venetian friar Luca Pacioli codified double-entry bookkeeping, the goal was simple: keep merchants from cheating each other. Today, the stakes are exponentially higher, involving complex international regulations and digital transactions that move at the speed of light.

Why Modern Ledgers Require Rigid Frameworks

Without standardized rules, corporate financial statements would resemble creative fiction. Imagine a tech startup in Austin, Texas, boasting about its massive valuation based entirely on projected user growth rather than actual cash flows—we're far from reality when that happens. The issue remains that investors need a universal language to compare a local bakery with a multinational conglomerate. This is why standardizing what are the 5 basic principles of bookkeeping became a global necessity. It forces companies to speak the same financial dialect, ensuring that a dollar recorded in Chicago matches the economic reality of a contract signed in London.

The Disconnect Between Cash Flow and True Profit

Here is where it gets tricky for the uninitiated business owner. You look at your bank account, see a healthy balance of $45,000, and assume your enterprise is thriving. That changes everything when you realize you owe suppliers $50,000 next week. Cash flow and profitability are distinct beasts altogether. Traditional accounting bridges this terrifying gap by using accrual concepts, moving beyond mere bank statements to reflect actual economic obligations. It is a system designed to prevent self-delusion, though many founders still fall into the trap of celebrating revenue that exists only on paper.

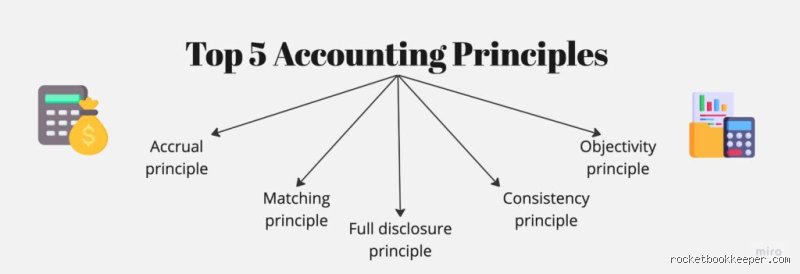

Deep Dive Into Historical Cost and Monetary Consistency

The first concrete pillar dictating our ledgers is the historical cost principle. This rule dictates that an asset must be recorded at its original purchase price, regardless of how much its market value fluctuates over time. If your firm bought a commercial warehouse in Seattle for $250,000 back in 2012, it stays on the books at that exact figure—even if a tech boom drives the local real estate valuation up to $1.2 million today. It seems counterintuitive, right? Why intentionally undervalue your company's net worth on paper?

The Anchor of Verifiable Purchase Prices

The reason for this conservative approach is simple: objectivity. Appraisal figures are fickle, subjective, and prone to manipulation by desperate executives looking to artificially pump up their balance sheets. By sticking to the actual receipt, bookkeeping remains anchored in verifiable truth. But people don't think about this enough: this stability comes at a cost. Relying on historical data means your financial statements can sometimes feel like a vintage photograph—accurate for the moment it was taken, but failing to capture the roaring fire of current market realities.

The Fiction of a Stable Currency Unit

Closely tied to this is the monetary unit assumption, which presumes that the currency you are measuring remains perfectly stable over time. We assume inflation does not exist for the sake of the spreadsheet. Yet, anyone who has run a business through an economic downturn knows that a dollar in 2026 does not possess the same purchasing power as a dollar did a decade ago. Bookkeepers willingly accept this structural flaw because the alternative—adjusting every single line item daily for inflation index changes—would turn corporate accounting into an unmanageable nightmare of shifting goalposts.

Aligning Timing: Revenue Recognition and The Matching Principle

The real magic—and the source of most corporate accounting scandals—lies in the timing of transactions. The revenue recognition principle dictates that you record income the exact moment it is earned, not when the client finally decides to pay the invoice. If your consulting firm delivers a comprehensive marketing strategy to a client in Boston on October 15, you recognize that revenue in October. It does not matter if the client drags their feet and doesn't wire the $15,000 fee until February of the following year; the economic event occurred in autumn.

The Pitfalls of Premature Income Tracking

This creates a fascinating paradox where a company can look wildly profitable on an income statement while simultaneously starving for actual cash. I have seen brilliant agencies collapse because they scaled operations based on massive Q3 recognized revenue, only to find themselves unable to meet payroll in Q4 because their clients were on 90-day payment terms. Which explains why understanding what are the 5 basic principles of bookkeeping requires a parallel mastery of working capital. You cannot pay your electric bill with recognized revenue; you need liquid cash.

Symmetry in the Ledger: Balancing Expenses Against Income

To prevent companies from gaming the system, the matching principle acts as the necessary counterweight to revenue recognition. This directive requires that every single expense incurred to generate revenue must be recorded in the same reporting period as that revenue. Think of it as financial symmetry. If a toy manufacturer in Ohio spends $8,000 on plastic raw materials in November to produce goods sold during the December holiday rush, that material cost must be expensed in December. Matching ensures that your monthly profit margins reflect the true cost of doing business rather than a chaotic roller coaster of disconnected outflows.

Objectivity Versus the Allure of Subjective Estimates

The final pillar holding up this edifice is the objectivity principle, a strict mandate that all accounting data must be clean, impartial, and backed by solid evidence. Your financial records cannot be based on gut feelings, optimistic forecasts, or opinions. Every single entry requires an audit trail—invoices, bank cancellations, receipts, or contracts. If an auditor cannot verify the origin of a transaction, it essentially does not exist in the eyes of regulatory bodies like the IRS or the SEC.

The War Between Fact and Executive Optimism

This principle often puts bookkeepers at odds with visionary founders. CEOs are paid to be optimists, to see value where others see risk, but a great accountant must be a professional cynic. When a manager insists that a piece of proprietary software they developed is worth millions, the objective bookkeeper points directly to the development cost receipts. It creates friction. Yet, this aggressive neutrality is exactly what prevents a business from spinning out of control into fraudulent territory, keeping the enterprise grounded in fiscal reality when market hype threatens to distort judgment.

Common Mistakes and Misconceptions in Financial Tracking

Confusing Cash Flow with Profitability

You glance at the bank balance and assume everything is fine. The problem is, liquid cash frequently lies. Founders often celebrate a massive influx of capital from an invoice, ignoring the reality that those funds must cover the next three months of operational overhead. Cash flow merely tracks when money moves, whereas genuine financial tracking requires measuring revenue when it is earned.

Because you see money in the account, you spend it. Yet, those obligations remain. This disconnect is precisely why profitable companies go bankrupt every single day; they lack the foresight to separate immediate liquidity from actual, long-term net income.

Treating Bookkeeping as a Once-a-Year Tax Chore

Let's be clear: waiting until April to organize your receipts is operational suicide. Many entrepreneurs view the 5 basic principles of bookkeeping as a bureaucratic hurdle meant solely for government compliance. It is not.

When you treat financial logging as an annual post-mortem, you lose the ability to make agile, data-driven decisions. How can you pivot your strategy when your fiscal data is five months out of date? (Spoiler: you cannot.) Cobbling together messy spreadsheets at the eleventh hour leads to missed deductions, duplicated invoices, and massive administrative headaches.

Over-Automating Without Human Oversight

Modern software promises magic. Except that algorithms do not understand the nuanced context of a business transaction. Software frequently miscategorizes a software subscription as office supplies, distorting your ledger accuracy over time.

Automation is a powerful tool, as a result: it accelerates data entry but amplifies systemic errors if left unchecked. You cannot simply plug in a bank feed and walk away; human validation keeps the system honest.

Expert Strategy: The Psychological Ledger

Embracing the Friction of Manual Micro-Audits

Here is an contrarian piece of advice from seasoned financial controllers: introduce intentional friction into your accounting workflow. While everyone else chases frictionless, automated systems, you should dedicate exactly ten minutes at the end of every Friday to manually reconcile your top five largest transactions.

This habit builds an intuitive, psychological connection to your cash reality that automated dashboards completely sanitize. You start to feel the weight of your expenditures. Which explains why founders who maintain this tactile relationship with their numbers consistently report a 14% reduction in discretionary spending within the first fiscal quarter.

It is about developing a visceral gut instinct for your financial health. Do not outsource your intuition to an algorithm. Lean into the mild discomfort of looking at your outflows every seven days, and watch your margins expand.

Frequently Asked Questions

What is the financial cost of poor record-keeping for small businesses?

Neglecting the core framework of financial tracking directly erodes a company's bottom line through avoidable penalties and lost opportunities. The issue remains that disorganized firms miss an average of $5,500 in legitimate tax deductions annually due to lost receipts and unrecorded expenses.

Furthermore, a study by the National Small Business Association revealed that 23% of small enterprises face IRS audit penalties averaging $850 per infraction solely because of sloppy documentation. Poor records also delay loan approvals, costing businesses an estimated $12,000 in lost revenue from stalled growth initiatives. In short, ignoring the 5 basic principles of bookkeeping is an incredibly expensive administrative failure.

Can a service-based business use cash accounting instead of accrual accounting?

Smaller operations frequently adopt cash accounting because it mirrors their actual bank account balance without complex adjustments. This method records revenue only when money hits the palm, which works adequately if your transaction cycle is immediate.

But the moment you introduce net-30 payment terms or upfront client deposits, cash accounting distorts your true financial posture. It leaves you blind to upcoming liabilities and earned but unbilled revenue. While permissible for entities making under $25 million in gross receipts, transitioning to accrual tracking is the only way to scale sustainably.

How long must a business retain its physical financial records and invoices?

The IRS generally requires businesses to preserve supporting documents, invoices, and employment tax records for a minimum period of 7 years. This timeline ensures you can definitively prove all claims if your filings are ever legally challenged or audited.

Failing to produce these documents during an inquiry can result in the retroactive disallowance of deductions, triggering hefty back-taxes. Storing digital copies in a secure, cloud-based archive satisfies these regulatory demands while saving physical office space. Just make sure those digital backups are organized systematically by fiscal year to avoid frantic searching later.

The Verdict on Financial Clarity

The Obsession with perfect software is a dangerous distraction from what actually matters. True financial health stems from a disciplined, almost religious adherence to structural ledger integrity. If you refuse to master the 5 basic principles of bookkeeping, you are essentially operating your enterprise with a blindfold on.

Stop treating your ledger as a historical graveyard of past spending and start using it as an active, predictive compass for future scaling. The data tells a story, provided you are brave enough to read it objectively. Step up, own your numbers, and stop hiding behind your accountant's skirt.