The Evolution of Double-Entry Ledger Mechanics: Where It All Began

Accounting is not merely a modern corporate headache. Around 1494 in Venice, a Franciscan friar named Luca Pacioli codified a system that merchants had been whispering about for decades. He did not invent it, but his documentation revolutionized commerce. The thing is, before Pacioli’s system took root, tracking wealth was a messy, single-entry affair where mistakes went unnoticed until a business was already bankrupt. Merchants literally guessed their profits based on the cash in their pockets—we are far from that primitive guessing game today.

The Architecture of the Account Classifications

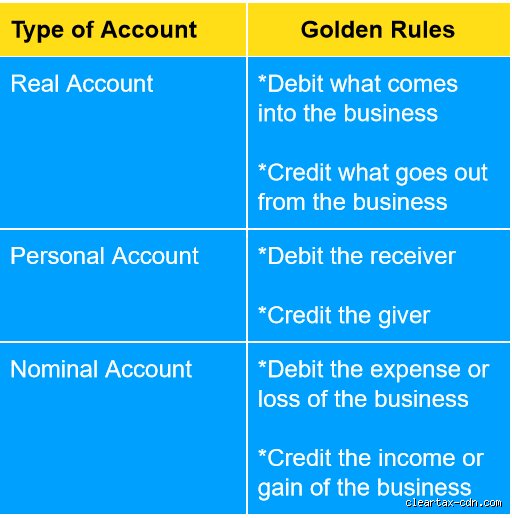

Before you even touch a ledger, you must realize that everything in business fits into three distinct buckets. Personal accounts track your dealings with living, breathing human beings or legal entities like Acme Corp. Real accounts handle the tangible stuff—machinery, buildings, hard cash—and the intangible ones like patents. Finally, nominal accounts capture the fleeting, ephemeral nature of expenses, losses, and revenues. If you misclassify a piece of manufacturing equipment as an expense, your entire balance sheet warps into pure fiction.

Why Manual Principles Persist in a Cloud-Based World

People don't think about this enough, but modern enterprise resource planning systems like SAP or NetSuite are just Pacioli’s brain wrapped in slick user interfaces. Software breaks down. When a junior accountant inputs an invoice incorrectly, the automated system will happily balance a completely erroneous entry. Understanding the underlying mechanics allows you to spot the ghost in the machine. I have seen multi-million-dollar discrepancies that took weeks to untangle, all because an automated script confused a liability with an equity draw during a routine system migration.

Decoding Rule One: The Realm of Real Accounts and Tangible Assets

Let us strip away the jargon and look at the first pillar, which dictates that you debit what comes in and credit what goes out. This specific doctrine applies strictly to real accounts, which encompass everything from cold hard cash in a bank vault in Manhattan to the delivery trucks idling outside a warehouse in Frankfurt. When assets change hands, this rule dictates the precise direction of the financial flow.

The Internal Friction of Asset Acquisition

Imagine your company buys a new delivery van on March 15, 2026, for $45,000 in cash. The van is coming into the business, so the vehicle account receives a debit. Conversely, cash is walking out the door, which necessitates a corresponding credit to the cash asset account. It sounds simple on paper. Yet, where it gets tricky is handling the hidden transaction costs like registration fees or delivery charges—do they count as part of the asset or a separate expense? Traditionalists argue for capitalization, but modern practices occasionally diverge depending on regional tax laws.

The Nuance of Depreciation and Disposal

Assets do not stay pristine forever. As machinery ages, its value deteriorates, creating an accounting paradox where the physical asset remains, but its book value shrinks. When you eventually sell that old van for scrap metal, you must reverse the initial entry process entirely. This is where many novice bookkeepers stumble. Because they forget to credit the original asset account for its historical cost while simultaneously accounting for accumulated depreciation, the ledger ends up permanently distorted.

Decoding Rule Two: Personal Accounts and the Human Element of Debt

The second fundamental guideline shifts our focus away from physical objects and toward relationships, establishing that you must debit the receiver and credit the giver. Personal accounts represent individuals, vendors, customers, and institutions like JPMorgan Chase. This rule governs credit transactions, which form the absolute lifeblood of modern corporate commerce where cash rarely changes hands immediately.

Managing Credit Transactions Without Losing Track

Suppose a long-term client, Smith & Sons Ltd, purchases $12,000 worth of raw steel from your warehouse on credit. Under this specific framework, Smith & Sons is the receiver of the goods, which means their account is immediately debited. You have not received a single cent of physical money yet. But you have acquired a legal claim on their future cash, known as an account receivable. Months later, when they finally send a wire transfer to settle the debt, they become the giver, resulting in a credit to their personal account and a corresponding debit to your bank account.

The Problem of the Uncollectible Debt

What happens when a client vanishes into thin air or files for bankruptcy? The issue remains that you cannot indefinitely carry a dead asset on your books. When a personal account defaults, you must aggressively write it off, converting that dead receivable into a nominal loss. Honestly, it's unclear why some firms delay this painful process, though it usually stems from a desire to make quarterly earnings look artificially inflated to shareholders.

The Structural Divergence: Real Accounts Versus Nominal Accounts

A major point of confusion for anyone entering the financial sector is the inherent friction between real accounts and nominal accounts. Real accounts are permanent fixtures that survive the closing of the fiscal year, carrying their balances forward into the next chapter of the company's life. Nominal accounts, however, are intentionally wiped clean at midnight on the final day of the accounting cycle, their contents poured directly into the retained earnings pool.

The Temporal Nature of Expenses and Revenue

Think of nominal accounts as temporary buckets designed to measure performance over a specific, limited window of time. The third rule—debit all expenses and losses, credit all incomes and gains—rules this domain completely. When you pay a $5,000 monthly office rent bill, that money is gone forever; it does not create a lasting asset like buying a building would. Hence, it is recorded as a debit to rent expense. That changes everything when analyzing profitability, because if you accidentally mix these up with real accounts, your net income figures become utterly meaningless overnight.