The DNA of Ledger Balancing: What is the Golden Rule of Bookkeeping Anyway?

Go back to Venice in 1494. A Franciscan friar named Luca Pacioli codified double-entry bookkeeping, and honestly, the core math has not changed a single bit since the Renaissance. The entire global economy rests on a deceptively simple equation: assets equal liabilities plus equity. Where it gets tricky is how modern business owners mistake digital data feeds for actual accuracy. You see a transaction download from a bank API into QuickBooks and assume everything is fine, right? We are far from it.

The Real Meaning of Debits and Credits

Forget standard English definitions where debit means losing money and credit means getting a limit increase on a plastic card. In the realm of professional accounting, debit simply means left and credit means right. That is it. If you purchase a high-end espresso machine for a cafe in downtown Chicago on March 12, 2026, you debit your equipment account because you received an asset. But you must credit cash or accounts payable because that value had to originate from somewhere. Every action has a reaction.

Why Modern Automation Conceals Costly Human Errors

People do not think about this enough: AI-driven accounting platforms are incredibly efficient at duplicating mistakes at lightning speed. If an entry-level clerk maps an invoice incorrectly in January, the software will happily replicate that blunder across 12 consecutive months of financial reporting. The system will technically balance—the math works—but your tax liability will be completely skewed. A balanced ledger does not automatically mean an accurate ledger, and that changes everything for an auditor.

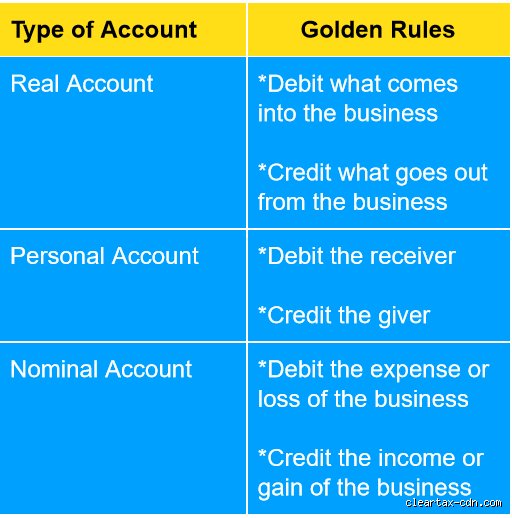

Deconstructing the Three Pillar Rules of Classical Accounting

Traditional accounting education breaks this ecosystem down into three distinct operational guidelines that govern real-world ledgers. First, debit real accounts when assets come in, and credit them when they leave. Second, debit the receiver for personal accounts and credit the giver. Third, debit all expenses or losses, and credit your gains and income. It sounds dry, yet it prevents corporate chaos.

Real Accounts and Tangible Company Wealth

Think about physical property, inventory, or cash reserves held at Chase Bank. When your Denver-based logistics firm buys a new delivery van for $45,000, the asset account swells via a debit. But the money has to leave your bank account, generating a corresponding credit. If you skip this dual entry, your balance sheet suddenly claims you possess forty-five thousand dollars in extra wealth that simply does not exist. It is pure fantasy.

Personal Accounts: Managing Humans and Corporate Entities

This is where we deal with actual people, suppliers, and clients. Let us say you run a consulting agency and you invoice a client in Boston for $8,500 on a Tuesday morning. You immediately debit their specific accounts receivable record because they owe you that value. They are the receiver of your expertise. When they finally mail a check three weeks later? You credit their personal account to wipe out the debt, while simultaneously debiting your cash account to reflect the incoming funds.

Nominal Accounts: Tracking the Invisible Flow of Expense and Revenue

Nominal accounts are temporary holding zones for things that do not have a physical form, like rent, utilities, or software subscriptions. When you pay $1,200 for office electricity, that money vanishes into an expense category via a debit. Experts disagree on the best ways to categorize ambiguous digital expenses nowadays, but the mechanics remain rigid. You cannot just log a cost without showing the exact account that funded it.

The Ripple Effect: What Happens When You Ignore the Balance?

If you ignore what is the golden rule of bookkeeping, your business will eventually face a cash flow crisis. It is not just about pleasing the IRS or passing an external audit without fines. The issue remains that flawed data leads to disastrous strategic decisions. Owners look at a bloated dashboard, think they have capital to burn, and sign leases they cannot afford.

The Disastrous Case of the Single-Entry Trap

Some micro-businesses still use single-entry tracking, which is basically a glorified checkbook register where you only write down what you spent. Imagine a retail boutique in Seattle during the Q4 holiday rush of 2025. The owner records a cash sale of $300 but fails to track the reduction in physical inventory on the shelves. By January, the cash looks great, but the shelves are bare and there is no capital reserved to restock. Single-entry systems fail because they only tell half the story.

How a Failed Reconciliation Destroys Investor Trust

I once reviewed a tech startup that missed a minor $14.20 discrepancy during their monthly bank reconciliation. It seemed completely insignificant to the founders. Except that small error was actually the net result of a misplaced $50,000 wire transfer and a mismatched $49,985.80 vendor payment. When venture capitalists discovered the sloppy tracking during due diligence, they walked away from the funding round entirely. Investors do not gamble on founders who cannot master basic ledger discipline.

Alternative Financial Frameworks: Do We Still Need This Rigor?

Cash-basis accounting offers an alternative to accrual-basis systems, allowing smaller entities to log transactions only when cash physically changes hands. It feels simpler. It feels more intuitive for creative professionals or freelancers who do not want to deal with complex accounts payable ledgers.

Cash vs Accrual Methodologies

Under the cash method, you do not record an invoice until the client pays you. This makes your bank balance look very clear, but it completely distorts your actual financial health if you have massive bills due next month. Accrual accounting relies heavily on what is the golden rule of bookkeeping because it forces you to match revenues and expenses in the exact period they occur, regardless of cash flow. It gives a true picture of profitability, hence its status as the gold standard for growing enterprises.

Common Mistakes and Misconceptions Regarding the Golden Rule of Bookkeeping

Many novice business owners assume that balancing the books implies absolute financial health. It does not. The problem is that a perfectly balanced ledger can still mask catastrophic operational realities if you misclassify transactions.

The Illusion of the Balanced Ledger

You can meticulously credit your cash account and debit an expense account, maintaining the pristine equilibrium required by double-entry systems. Yet, if that expense was actually an asset acquisition, your balance sheet becomes a work of fiction. Misallocating capital expenditures as operational expenses deflates your net income artificially. The entries match perfectly, which explains why automated software rarely flags these structural blunders. Computers validate math, not economic intent.

Mixing Personal and Business Oceans

Let's be clear: co-mingling funds is the ultimate administrative sin. When you use the corporate account to buy a morning espresso, you violate the core tenet of entity separation. It sounds trivial. Because a single coffee won't bankrupt a firm, right? Wrong, it muddies the audit trail. Entrepreneurs frequently forget that the golden rule of bookkeeping demands a pristine boundary between the owner's wallet and the enterprise's ledger. A single messy month can require up to 15 hours of forensic reconciliation to rectify.

Over-Reliance on Automation

Modern cloud platforms promise magic. They sync bank feeds and auto-categorize recurring transactions with startling speed. However, blindly accepting these algorithmic suggestions compromises your financial integrity. A platform might tag a 2,500 dollar legal settlement as routine utility spend. If you fail to review these triggers, your historical data becomes useless for forecasting.

The Hidden Velocity of Money: Expert Strategic Advice

True mastery of financial tracking goes beyond merely recording historical artifacts. You must look at temporal distortion.

The Lead-Lag Asymmetry

The golden rule of bookkeeping dictates that every debit must equal a credit, yet it says absolutely nothing about the timing of actual cash flows. This is where most expanding enterprises choke. You sign a lucrative 100,000 dollar contract. Your ledger reflects the revenue under accrual guidelines. But what happens if the client negotiates a 90-day payment window while your suppliers demand immediate settlement? You are technically profitable, yet practically insolvent. Managing the cash conversion cycle requires tracking the velocity of your ledger adjustments, not just their static balance. We must acknowledge that accounting software shows you the map, but it rarely warns you about the immediate traffic jam.

Frequently Asked Questions

What happens if a business violates the golden rule of bookkeeping for an extended period?

Persistent neglect of symmetrical ledger entry integrity leads to a complete breakdown of corporate governance. Statistics indicate that 82 percent of small businesses fail due to cash flow mismanagement, a crisis often masked by distorted financial records. When your debits and credits do not align, generating accurate income statements becomes impossible. Regulatory bodies like the IRS can impose penalties averaging 20 percent of the underpayment amount for negligent record-keeping. As a result: outside investors will flee, banks will summarily deny line-of-credit applications, and your operational visibility drops to zero.

Can micro-enterprises use single-entry methods and ignore double-entry principles?

While a solo freelancer earning under 50,000 dollars annually can legally utilize single-entry cash accounting for tax purposes, doing so severely limits scalability. Single-entry systems function like a basic checkbook register, tracking receipts and payments without establishing a corresponding balance sheet. Why would you deliberately blindfold your business growth? This simplistic approach fails to track liabilities, outstanding client invoices, or equipment depreciation. In short, avoiding the rigorous double-entry framework prevents you from understanding your true net worth or leveraging asset equity for future commercial loans.

How does the transition from cash to accrual accounting affect ledger balancing?

Shifting to accrual rules introduces complex matching adjustments that complicate your daily entry validation. Under this framework, you must record revenues when earned and expenses when incurred, irrespective of when physical currency changes hands. For a mid-sized firm making this transition, accounts receivable balances can instantly spike by 40 percent or more. This conversion requires establishing robust matching accounts to track prepaid expenses and unearned revenues accurately. Consequently, your bookkeeping workflows will require daily reconciliation cycles rather than a casual end-of-month review to maintain system equilibrium.

The Reality of Financial Equilibrium

Let us stop treating accounting as a mere bureaucratic chore or a dry compliance exercise. The golden rule of bookkeeping is not a rigid cage designed by pedantic auditors; it is the ultimate truth machine for your operational efficiency. If you treat your ledger as a secondary priority, you are flying a commercial aircraft through a storm without an instrument panel. The numbers never lie, though they frequently mock our optimistic business projections. True financial leadership demands that you respect the mathematical symmetry of your enterprise every single day. Own your financial data completely or watch your entrepreneurial ambitions crumble under the weight of unrecorded realities.