Beyond the Spreadsheet: Why Everyone Misunderstands the Basic Chart of Accounts Architecture

Most founders think accounting is just math. It is not; it is taxonomy. When you look at a raw list of ledger entries from a company like Stripe or FedEx, you are staring at absolute chaos unless a rigorous chart of accounts is there to enforce discipline. The issue remains that generic software defaults lure businesses into a false sense of security, handing them a cookie-cutter template that treats a software-as-a-service startup the same as a local bakery. That changes everything, and usually for the worse.

The Anatomy of the Five Core Categories

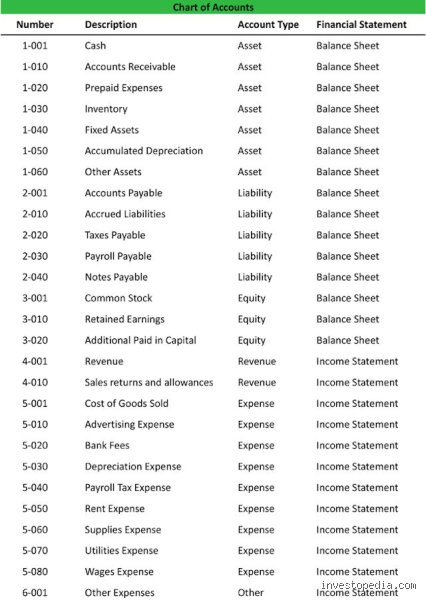

Every transaction falls into five distinct buckets, a rule established back in 1494 by Luca Pacioli, the monk who popularized double-entry bookkeeping. First come the assets, things you own, ranging from cash in a Chase checking account to a $500,000 printing press. Liabilities represent what you owe, such as a business loan or vendor invoices sitting in accounts payable. Equity is the residual value left for owners, while revenue and expenses track the operational dance of bringing money in and pushing it out. People don't think about this enough, but how you segment these five pillars dictates whether your financial reporting actually reflects economic reality or just satisfies tax compliance.

The Hidden Layer of Sub-Accounts

Where it gets tricky is when companies need granular data to make actual decisions. You do not just track "Travel Expenses"—that is too vague to be useful. An enterprise operating across the Midwest might split that into lodging, airfare, and meals, giving each a distinct sub-account tag. Because if you clump everything together, how do you spot a 15% spike in regional sales costs? You cannot.

The Numerical Coding Secrets Behind Modern General Ledgers

Accounting systems run on numbers, not words, which explains why the numbering system in a chart of accounts is so standardized. Historically, a four-digit block system formed the backbone of corporate ledgers, though modern global enterprises frequently utilize seven or eight digits to accommodate complex international operations. The first digit always tells you the account type—usually 1000 for Assets and 2000 for Liabilities—acting as a universal shorthand for auditors and software algorithms alike.

Deciphering the Block Numbering Logic

Let us look at how this plays out in the real world. A standard setup assigns 1000-1999 to assets, 2000-2999 to liabilities, and 3000-3999 to equity. Within that asset block, liquidity dictates the order. Cash comes first at 1010, followed by accounts receivable at 1200, and finally inventory at 1400 because you cannot buy groceries with a warehouse full of unsold widgets, can you? Fixed assets like real estate sit much further down the block, usually around 1700, reflecting their illiquid nature. Experts disagree on whether to leave gaps of five or ten numbers between accounts, but honestly, it's unclear why anyone would risk bottlenecking their system by numbering them sequentially without breathing room for future expansion.

The Global Expansion of Digit Length

But what happens when a firm grows? A four-digit system breaks down the moment a business expands from a single storefront in Chicago to ten international subsidiaries. That is when we see the introduction of multi-segmented codes, where the first three digits represent the natural account, the next two represent the department, and the final three represent the geographic region. A code like 5010-20-440 might signify marketing expenses for the European division, a level of precision that allows a CFO to instantly generate localized profitability reports.

Designing a Scaling Infrastructure: Customizing Your Financial Map

I have seen dozens of mid-market companies choke their own growth because they treated their chart of accounts like a static document rather than a living organism. Your ledger architecture must mirror your organizational chart. If your company restructures to focus on digital product lines rather than physical retail, but your accounting system still reflects the old brick-and-mortar reality, your financial statements are basically useless baggage. Yet, changing a ledger structure mid-year is the corporate equivalent of open-heart surgery while running a marathon.

The Danger of Over-Segmentation

There is a seductive trap here: creating an account for every single micro-expense. I once reviewed a ledger for a tech firm that had separate codes for paper clips, printer paper, and sticky notes. That is madness. It creates administrative fatigue, leads to rampant data-entry errors by tired clerks, and ultimately provides zero strategic value to the executive team. The goal is to strike a balance between executive visibility and operational simplicity, ensuring that your operating expenses are grouped meaningfully without turning the general ledger into a chaotic diary.

Industry-Specific Ledger Variations

A manufacturing company like General Electric requires a radically different chart of accounts compared to a digital agency in New York. The manufacturer needs intricate tracking for raw materials, work-in-progress inventory, and finished goods to calculate the exact cost of goods sold. Conversely, the digital agency can mostly ignore inventory accounts, focusing instead on unbilled revenue and utilization tracking for their consultants. If you try to force a service business into a manufacturing ledger template, you will end up with a convoluted mess of empty categories and mismatched data points.

Standardization vs. Customization: The Battle of GAAP and IFRS Frameworks

This is where the compliance rubber meets the operational road. While a company has the freedom to design its internal numbering system, the final output must comply with regulatory frameworks like Generally Accepted Accounting Principles (GAAP) in the United States or International Financial Reporting Standards (IFRS) globally. This requirement forces a fascinating tension between how a management team wants to view their business and how the Securities and Exchange Commission demands it be reported.

The Rigidity of Regulatory Reporting

Regulatory bodies do not care about your custom internal metrics or your clever department codes. They want to see a clear, standardized presentation of current assets versus long-term liabilities to assess corporate liquidity. This means your flexible internal chart of accounts must seamlessly roll up into rigid, standardized buckets when it comes time to publish quarterly reports. As a result: the mapping process between your daily operational ledger and your final financial statements must be flawless, or you risk facing severe regulatory penalties during an annual audit.