Beyond the Spreadsheet: The Evolution and Modern Reality of Financial Tracking

Let us be real for a moment. Mention accounting to a room full of tech entrepreneurs or retail managers, and you can practically hear the collective sigh as eyes glaze over. They think of dusty ledger books, green eyeshades, and spreadsheets stretching into the digital horizon. The thing is, this perception is dangerously outdated. Modern financial architecture is less about hoarding receipts and more about constructing a living, breathing map of an organization's economic reality. Without this map, executives are essentially flying a commercial jet in dense fog without an instrument panel.

The Trap of the "Rearview Mirror" Mentality

Here is where it gets tricky. Traditionalists view these bookkeeping routines as a historical record. You look backward to see what you spent, which is fine, except that relying solely on historical compliance data is like driving down a highway while staring exclusively into your rearview mirror. I happen to believe that the true value of these procedures lies not in satisfying the tax authorities, though that keeps people out of prison, but in forecasting structural vulnerability. It is an active diagnostic mechanism. Yet, a shocking number of startups fail precisely because they treat their numbers as an afterthought to be sorted out during the Q4 tax preparation window.

A Fragmented Industry: Where Experts Openly Disagree

Do not assume the entire financial world agrees on how this should be executed. Honestly, it's unclear where the boundary between pure bookkeeping and strategic corporate finance truly lies these days. Some academics argue that the preliminary steps of data ingestion are purely administrative, leaving only the synthesis phase to be worthy of the "accounting" moniker. We are far from a consensus here. While the textbooks preach a seamless, linear workflow, the daily reality inside a fast-paced corporate finance department is often a messy, chaotic scramble to harmonize legacy software systems.

Activity 1: The Chaos of Raw Data Ingestion and Source Document Verification

Every single financial journey begins with a piece of paper, a digital PDF, or an automated cryptographic token. This is data collection. People don't think about this enough, but if your initial inputs are flawed, every subsequent balance sheet or profit metric becomes complete fiction. We are talking about invoices, bank statements, payroll logs from ADP systems, and point-of-sale data gathered from platforms like Shopify. In a typical mid-sized firm, like the logistics outfit I advised in Chicago last March, this phase involves sorting through thousands of disparate transactions a week.

The Anatomy of a Source Document

What makes a document valid? It is not just about having a dollar amount stamped on a page. A legitimate source document must provide verifiable proof of an economic exchange, featuring timestamps, counterparty identities, and explicit tax breakdowns. If an auditor walks into your office in October 2026 and asks to see the backup for a random $14,500 equipment depreciation entry, this is what you hand them. Because without these tangible anchors, your entire general ledger is nothing more than a collection of expensive campfire stories.

The Automation Myth and the Human Element

Many executives believe that installing enterprise resource planning software fixes this step instantly. But that is a pipe dream. Even with advanced optical character recognition technology processing digital receipts, human oversight remains indispensable for contextual categorization. Imagine an automated system misinterpreting a software-as-a-service subscription renewal as a capital asset purchase. The system executes the command perfectly, but the logic is flawed. As a result: your expense reporting for the quarter is completely warped, distorting your true operating margins.

Activity 2: The Double-Entry Matrix and Journalizing Transactions

Once you have verified the data, it must be translated into the formal language of business through journalizing. This is where we encounter the ancient double-entry system, a concept pioneered by the Italian Franciscan friar Luca Pacioli in 1494. Every transaction must be recorded in chronological order within a general journal or specialized sub-journals. It is a symmetrical universe where every debit must have a corresponding credit. If you purchase a delivery van for $45,000 in cash, your assets increase in one column and decrease in another simultaneously.

The Mechanics of Debits and Credits

The rules of this matrix can feel completely counterintuitive to the uninitiated. For instance, an increase in an expense account is recorded as a debit, whereas an increase in revenue is a credit. Why? Because the system is designed to maintain a permanent equilibrium, ensuring that assets always equal liabilities plus equity. It is a beautifully balanced intellectual structure, resembling a complex game of three-dimensional chess played with currency. But when an inexperienced clerk messes up a single entry in a specialized accounts payable journal, the entire structure begins to wobble.

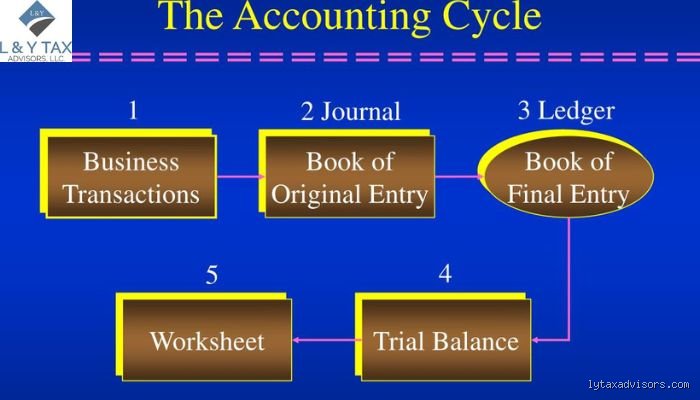

Decoupling the Ledger: Journalizing Versus Ledger Posting

It is quite common for outsiders to confuse the act of journalizing with ledger posting, but they serve entirely different masters within the workflow. Think of the journal as a diary. It tells the chronological story of a business day by day, listing events as they happen without regard to the bigger picture. The ledger, however, is a thematic encyclopedia. It groups those identical events by specific accounts, allowing a manager to see the total aggregate impact on cash, inventory, or accounts receivable at any given moment.

Chronological Narrative Versus Analytical Synthesis

The issue remains that looking at a journal will not quickly tell you how much money you owe your suppliers. You would have to manually add up hundreds of individual pages. Posting resolves this by transferring the journal entries to individual ledger accounts. This process transforms a chaotic timeline of business activities into a clean, categorized repository of financial truths. Hence, the ledger becomes the ultimate source of truth for generating high-level corporate strategy. The table below illustrates how these two phases separate raw data into structured insights.

| Feature Assessed | Journal Recording Phase | Ledger Posting Phase |

| Primary Arrangement | Strict chronological order based on transaction date | Thematic categorization based on specific account codes |

| Operational Purpose | Acts as the initial book of entry for raw validation | Serves as the final book of record for balance analysis |

| Systemic Focus | Individual transaction details and counterparty notes | Cumulative balances and structural account health |

Common Misconceptions and Costly Blunders in Financial Tracking

The Illusion of the Automated Ledger

Software does not think. Many business owners believe buying a high-end SaaS platform solves their entire tracking problem, except that bad data in equals bad data out. Algorithms can categorize a transaction, yet they cannot determine if a lunch meeting was a genuine marketing expense or a personal meal. Human oversight remains mandatory. When artificial intelligence automatically matches invoices, it frequently misinterprets nuance, which explains why manual reconciliation still consumes hours of a professional's week. Relying solely on automation invites devastating audit discrepancies.

Confusing Cash Flow with Pure Profitability

Your bank account is lying to you. A balance of fifty thousand dollars feels comfortable, but it ignores outstanding vendor debts and deferred tax liabilities. Let's be clear: cash flow and net income are entirely different beasts. You might look rich today while sliding into bankruptcy tomorrow because revenue recognition laws require counting income when earned, not when received. Why do so many founders ignore this distinction? The problem is that cash feels real, whereas accrual systems feel like abstract academic exercises.

The Danger of Retrospective Compliance

Treating your ledger like a yearly chore is financial suicide. Waiting until April to sort through crumpled receipts guarantees missed deductions and inaccurate reporting. Because tax planning requires proactive, real-time adjustments, retroactive data entry provides zero strategic value. It turns a potential steering wheel into a useless rearview mirror.

The Hidden Engine: Forensic Data Analysis and Strategic Forecasting

Unlocking the Power of Variance Interpretation

The standard balance sheet only tells half the story. The true magic happens when an expert digs into the gaps between projected budgets and actual expenditures. This discipline requires an unpredictable mix of historical investigation and behavioral psychology. You must understand why a department overspent, not just by how much. For instance, a twelve percent spike in raw material costs might look like supply chain failure, but deeper analysis could reveal it was a strategic bulk purchase to hedge against impending inflation. (Smart accountants spot these nuances instantly). We must look beyond the raw numbers to find the operational truth.

Transforming Regulatory Compliance into Competitive Advantage

Most executives view tax codes as a prison. Sophisticated entities view them as a roadmap for corporate strategy. By aligning capital expenditures with specific government incentives, you actively reduce your effective tax rate while modernizing your infrastructure. It is not about dodging obligations. The issue remains that average companies merely report past events, whereas market leaders use these statutory frameworks to fund their future expansion.

Frequently Asked Questions

Is it possible to manage corporate ledgers without specialized software?

Technically, yes, a firm can survive using basic spreadsheets, but the operational risks escalate exponentially. Recent industry metrics indicate that manual data entry suffers from an average error rate of 0.95 percent per keystroke. In a corporation processing ten thousand monthly transactions, those microscopic mistakes compound into massive financial discrepancies. Furthermore, modern regulatory bodies mandate strict cryptographic audit trails that legacy spreadsheets simply cannot provide. In short, avoiding dedicated digital platforms saves nominal subscription fees today while guaranteeing catastrophic forensic accounting costs during your next external audit.

How does the accrual method differ fundamentally from cash-basis systems?

Cash systems record transactions only when currency physically changes hands, making it highly deceptive for complex operations. Accrual frameworks recognize economic events the exact moment they occur, matching revenues directly against the specific expenses that generated them. Imagine securing a one hundred thousand dollar corporate contract in November but not receiving the wire transfer until February. The cash method shows a starving business in Q4 and an artificially inflated paradise in Q1, distorting your true operational health. As a result: savvy investors completely reject cash-basis statements when evaluating corporate valuation or creditworthiness.

What specific triggers should prompt an enterprise to outsource its financial oversight?

When your internal executive team spends more than ten hours a week wrestling with payroll allocations or inventory valuations, your growth bottlenecks. Another critical indicator is crossing the threshold of five distinct jurisdictional tax regions, which introduces unbearable regulatory complexity. Mismanaging cross-border sales tax compliance can trigger penalties that wipe out your entire quarterly margin. If your current staff cannot produce accurate monthly closing statements within seven business days, your decision-making data is already obsolete. Do not wait for a formal warning from revenue services before upgrading your professional support.

A Paradigm Shift in Corporate Stewardship

Accounting is not a passive filing system; it is the definitive operational playbook for survival. Business leaders must stop treating fiscal management as a secondary administrative burden. We must boldly state that financial transparency dictates market longevity. If your internal data is chaotic, your strategic vision is nothing more than a hallucination. The numbers never lie, but they will happily watch you fail if you refuse to interpret them correctly. Turn your ledger into a weapon, or watch your competitors use theirs against you.