The Mechanics of Trust Evolution: From Flexible to Unchangeable

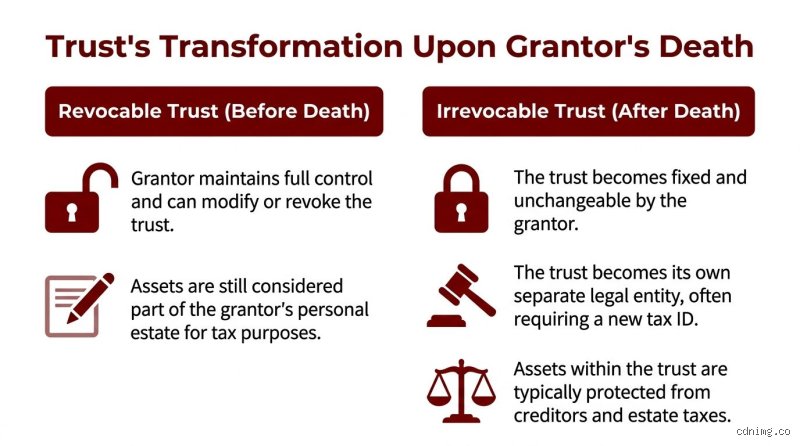

When you set up a revocable living trust—let us use the example of Arthur Pendelton in San Francisco back in 2018—you wear three hats simultaneously. You are the grantor who created it, the trustee who manages the bank accounts, and the primary beneficiary who enjoys the money. It is a legal mirror image of yourself. Because you hold all the cards, you can tear the document up, sell the house inside it, or rewrite the beneficiaries on a whim. That is the essence of a revocable instrument.

The Trigger Event That Alters Everything

Death changes everything. The moment the grantor passes away—or in the case of a joint trust, when the surviving spouse also dies—the power to revoke dies with them. Nobody else possesses the legal authority to alter the text. Why? Because the law dictates that the grantor's intent must be preserved flawlessly, and since the grantor is no longer around to consent to changes, the document hardens into an irrevocable trust. It becomes an independent legal entity with its own tax identification number, completely separate from the deceased creator.

The Myth of the Automatic Transfer

Do not mistake this legal hardening for instant wealth distribution. The trust becomes irrevocable immediately, yes, but the assets do not just magically fly into the bank accounts of your children. A successor trustee—perhaps your oldest daughter or a professional fiduciary company like Vanguard Trust Services—must step into the vacuum. They have to formally accept the role, notify the beneficiaries within a strict statutory window (often 60 days depending on state law), and begin the arduous process of trust administration. It is a hands-on job.

Tax Implications and the IRS Reality Check After a Grantor Dies

Here is where the paperwork gets heavy and expensive. While Arthur Pendelton was alive, the IRS did not care about his trust because he reported everything on his personal Form 1040. The trust was a pass-through entity using his Social Security number. Once he passed away in November 2024, that arrangement vanished forever.

The Birth of the EIN and Form 1041

The newly minted irrevocable trust cannot use a dead person's Social Security number. The successor trustee must immediately apply for a federal Employer Identification Number (EIN) from the IRS. From that day forward, the trust files its own tax return using Form 1041. This is no minor administrative detail. Irrevocable trusts face compressed tax brackets, hitting the highest federal income tax rate of 37% at just $15,250 of retained income, a threshold that individuals do not reach until their income climbs past $600,000. It is a brutal fiscal reality that catches many families off guard.

The Stepped-Up Basis Windfall

Yet, the tax code offers a massive silver lining that offsets these compressed brackets. Because the assets inside a revocable living trust are included in the grantor's gross estate for estate tax purposes, those assets qualify for a stepped-up basis to fair market value at the date of death. If Arthur bought a rental property in Oakland for $200,000 in 1995, and it is worth $1.5 million when he dies, the beneficiaries can sell it immediately through the irrevocable trust and pay zero capital gains tax. That changes everything for the heirs.

The Grey Areas Where Experts Disagree on Trust Finality

We like to pretend the law is binary, a neat line between black and white, but honestly, it is unclear sometimes how absolute this irrevocability really is. While the grantor cannot change the terms from beyond the grave, the living sometimes find ways to bend the bars of the cage. The issue remains that families change, laws evolve, and what made sense in 2010 might look absurd by 2026.

The Modern Escape Hatch Known as Decanting

Can you change an unchangeable trust? Sometimes, yes. Through a process called trust decanting—literally pouring the assets of an old, poorly worded trust into a brand-new one with better terms—trustees can bypass rigid restrictions. If the original document has an outdated administrative flaw, a savvy attorney in states like Nevada or Delaware can use state statutes to effectively rewrite the rules. But we are far from an easy fix here; this requires deep pockets and judicial or beneficiary consent, which means it is never guaranteed.

Judicial Modification and the Power of the Court

What happens if the trust becomes impossible to execute? If Arthur's trust mandated that his wealth be invested solely in a defunct railroad company, a judge can step in. Courts possess the equitable power to modify an irrevocable trust if unforeseen circumstances have frustrated the original purpose of the grantor. The trouble is, you are now paying litigation attorneys $500 an hour to argue about what a dead man wanted, which defeats the purpose of avoiding court in the first place.

Comparing the Shift: Single Grantor vs. Joint Marital Trusts

The transition from revocable to irrevocable gets significantly more complicated when we move away from single individuals and look at married couples. It is a common trap for families who think one size fits all.

The Clean Break of the Single Settlor

With a single grantor, the line is sharp. One heartbeat stops, the trust locks, the successor trustee takes over, and the administration begins. There is no ambiguity, no shared assets to untangle, and no surviving spouse to placate. It is the cleanest version of the process.

The Complex Split of the AB Trust Structure

But when a married couple uses a joint trust—frequently structured as an AB Trust or a marital bypass trust—the death of the first spouse triggers a partial freeze. Half of the trust assets (the deceased spouse's share) typically move into an irrevocable "B Trust" or Credit Shelter Trust to lock in estate tax exemptions, while the surviving spouse retains complete control over the revocable "A Trust" containing their own share. It is a logistical nightmare of bookkeeping, asset valuation, and dual tax tracking that requires a professional accountant to survive intact.

Common Mistakes and Misconceptions Regarding Trust Status

The Illusion of Immediate, Automatic Transformation

You assume everything freezes the millisecond a heartbeat stops. It does not. While the conceptual shift from legal revocability to irrevocability happens instantly, administrative paralysis frequently traps families before the new machinery actually starts working. The problem is that financial institutions do not possess psychic powers. A bank will not alter an account profile simply because a death occurred; they demand death certificates, certified trust extracts, and updated tax identification numbers first. Until those documents land on a compliance officer's desk, the assets remain in a functional limbo where nobody can touch them.

The Trap of the Joint Trust

Couples routinely fall into a massive trap assuming a single shared document behaves identically to an individual one. Except that it rarely does. When the first spouse passes away, does a living trust automatically become irrevocable upon death? For joint entities, the answer is a frustratingly complicated "only partially." Usually, the deceased partner's specific share of the estate locks down permanently to protect underlying beneficiaries, yet the surviving spouse retains complete, unchecked authority to alter, amend, or completely strip their own half of the assets. Failing to separate these distinct sub-trusts immediately can trigger severe IRS tax penalties and spark bitter, multi-generational litigation among heirs who feel cheated by subsequent step-parents.

Ignoring the Essential Tax ID Shift

Let's be clear: using a deceased person's Social Security number for ongoing estate transactions is a fast track to a federal audit. A revocable arrangement operates entirely under the grantor's personal tax identity during their lifetime. But the exact moment that structure hardens into an irrevocable status, it transforms into a completely independent legal and tax entity. You must immediately file IRS Form SS-4 to secure a brand-new Employer Identification Number (EIN). Failing to execute this shift within nine months of the grantor's passing messes up fiduciary accounting, delays mandatory distributions, and guarantees a bureaucratic nightmare with state revenue agencies.

Advanced Legal Mechanisms and Expert Guidance

The Power of Administrative Flexibility Provisions

Total immutability sounds safe, yet absolute rigidity often breaks under the weight of changing real-world circumstances. Smart estate planners inject specific escape hatches directly into the paperwork before the concrete dries. Incorporating a Trust Protector clause grants an independent third party the legal authority to modify administrative terms, change the governing state law, or swap out toxic trustees long after the original creator has died. This mechanism provides a vital safety valve if tax laws shift dramatically or if a designated beneficiary develops a destructive substance abuse problem. It allows the operational framework to adapt to fresh economic realities while strictly honoring the original intent of the decedent.

Navigating the Trust Decanting Process

What happens when an unchangeable vehicle becomes completely unworkable? You might be able to pour the old assets into a completely fresh vessel through a specialized process known as decanting. This sophisticated maneuver allows a fiduciary to transfer property from an unfavorable, restrictive framework into a brand-new, modern document with superior terms. Currently, over 25 US states permit decanting under specific statutory guidelines. It represents the ultimate tool for fixing drafting errors, modernizing archaic distribution schedules, or adding robust asset protection features without enduring the agonizing delays and public exposure of a formal courtroom battle.

Frequently Asked Questions

Can a trustee change the terms after the grantor passes away?

Absolutely not, because a successor trustee possesses zero legislative authority to rewrite the core distribution rules or alter the named beneficiaries specified in the original document. Their singular legal mandate centers entirely on executing the explicit orders left behind by the deceased creator. Statistical data from estate litigation reviews indicates that roughly 22% of fiduciary lawsuits stem directly from well-meaning trustees attempting to unauthorizedly reallocate assets based on what they mistakenly believe the deceased person would have wanted. Any unauthorized deviation from the written text constitutes a severe breach of fiduciary duty, which exposes the trustee to personal financial liability and immediate removal by a probate judge.

Does a living trust automatically become irrevocable upon death for all assets?

Only assets that were properly titled in the name of the structure prior to the grantor's passing will transition into this protective, unchangeable status. Many individuals mistakenly believe the mere existence of the document magically shields their entire estate. The issue remains that any account, real estate deed, or investment portfolio left in the creator's individual name must still pass through the lengthy, expensive public probate process. Empirical tracking of estate administrations reveals that approximately 35% of established trusts are underfunded at the time of death, meaning valuable assets were left outside the safety net. These forgotten items require a catch-all pour-over will to push them into the framework after the fact, a process that completely destroys the privacy goals of the original plan.

How long does it take to settle everything once the status changes?

The timeline for wrapping up operations typically spans anywhere from five months to nearly two years depending entirely on asset complexity and the specific debts involved. Settling a clean estate holding only a primary residence and a couple of liquidated brokerage accounts can move swiftly if the successor trustee acts with high efficiency. However, if the decedent owned commercial real estate, international assets, or complex business interests, the process slows down drastically. Fiduciaries must also leave the estate open long enough for the four-to-six-month creditor claim window to expire under local state statutes. As a result: rushing distributions to beneficiaries before resolving outstanding tax liabilities can make the trustee personally liable for the lingering debts.

Strategic Synthesis and Final Assessment

Waiting until a funeral to understand the operational machinery of an estate plan is a recipe for familial disaster. Does a living trust automatically become irrevocable upon death? Yes, the legal transformation triggers instantaneously, but the practical, real-world execution requires meticulous, deliberate administrative action to succeed. Wealth preservation is never an automated, hands-off cruise control system that functions flawlessly without human intervention. (And let's be totally honest, human error is the number one destroyer of even the most masterfully crafted inheritance plans.) True security requires proactive funding, clear communication, and an acute understanding of how tax identities shift when a heartbeat stops. Do not leave your family guessing where the boundaries sit when they are grieving. Speak with a qualified estate attorney today to ensure your documents match your exact intentions before time runs out.