The Fatal Collision of Living Trusts and Tax-Deferred Accounts

Estate planning attorneys love trusts, and for good reason. They bypass probate court, keep your financial business private, and dictate exactly how your assets are distributed after you take your final breath. But when you try to shove a traditional 401k or a Traditional IRA inside a standard revocable living trust while you are still breathing, the financial machinery breaks down completely. The thing is, the IRS views these accounts through a completely different lens than your house or a standard brokerage account.

The Ownership Quandary: Who Actually Holds the Reins?

You cannot simply change the ownership title of an IRA to the name of your trust. If you try to transfer ownership of a tax-deferred account to a trust during your lifetime, the IRS treats that specific administrative action as a total individual distribution of the entire account value. Boom. Just like that, you have triggered a massive taxable event. Because of this, your retirement account must remain in your individual name until your death. The only way a trust ever gets involved with these accounts is if you intentionally name the trust as a primary or contingent beneficiary on your account's designation form. But even then, where it gets tricky is how the IRS reacts once you pass away.

A Clash of Definitions: Individual Humans Versus Legal Constructs

The tax code was built with a specific assumption in mind: retirement accounts are meant for individual human beings who have finite lifespans. A trust is an artificial legal entity. It does not eat, it does not sleep, and it certainly does not have a life expectancy that can be easily plugged into an actuarial table. When an entity without a heartbeat becomes the owner or beneficiary of a retirement account, the IRS gets nervous and immediately starts demanding its tax cut much faster than you or your heirs would ever prefer.

Technical Breakdown: The Death of the Stretch IRA and the SECURE Act Reality

Everything we used to know about inheriting retirement accounts shattered on January 1, 2020. That was the day the SECURE Act officially went into effect, changing the wealth transfer playbook permanently. Before this legislative shift, naming a trust as a beneficiary allowed heirs to slowly pull money out over several decades. Now? We are far from that reality.

The Brutal 10-Year Rule for Designated Beneficiaries

For most non-spouse heirs, the old strategy of stretching distributions over a lifetime is dead. Under the current rules, inherited retirement accounts must be completely emptied by December 31 of the 10th anniversary year of the original owner's death. This compression applies whether the money goes to an individual or a trust. Imagine your daughter inheriting a $1.2 million Traditional IRA. If she inherits it directly, she can manage those withdrawals over a decade, perhaps taking larger chunks during years when her career income drops. If that money flows through a poorly drafted trust, however, the administrative flexibility evaporates completely, and the tax consequences become severe.

The Compressed Trust Tax Bracket Nightmare

Here is something people don't think about this enough: trusts hit the highest federal income tax bracket incredibly fast. In 2026, an individual human does not reach the highest 37% federal income tax bracket until their taxable income climbs past roughly $600,000. Yet, for a trust, that exact same 37% maximum tax bracket slams shut at just $16,000 of retained income. I cannot emphasize enough how devastating this disparity is. If a trust receives a large distribution from a traditional retirement account and retains that money within the trust structure rather than paying it out immediately to the beneficiary, the IRS will happily confiscate more than a third of it right out of the gate. That changes everything for families trying to build generational wealth.

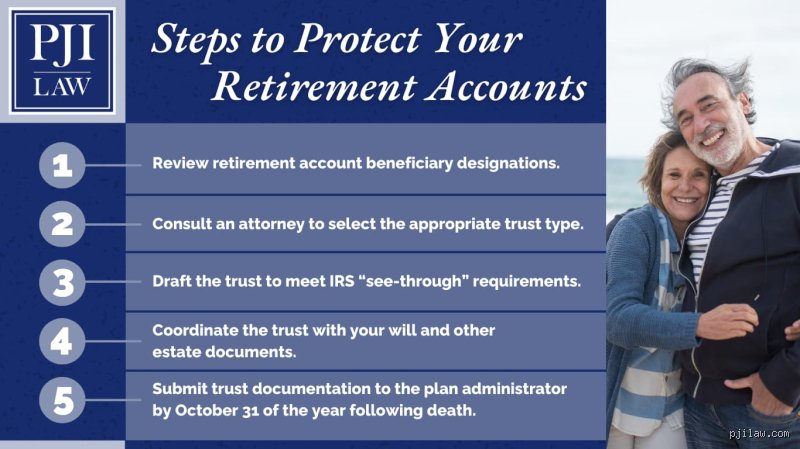

The Mirage of Control: When See-Through Trusts Fail

Some estate planners will try to sell you a complex workaround known as a see-through trust or a conduit trust. The theory is that the IRS will look through the legal paperwork and treat the actual human beneficiaries as the direct recipients for tax purposes. Except that it rarely works out as cleanly as the marketing brochures suggest. The issue remains that the rules governing these structures are notoriously rigid.

The Administrative Burden of Conduit Structures

A conduit trust is designed to act as a mere pass-through window. Any distribution forced out of the retirement account by the 10-year rule must be immediately pushed out of the trust and handed directly to the beneficiary. But wait a minute. If the primary reason you created the trust in the first place was to keep a massive lump sum of cash out of the hands of a spendthrift child or an unstable relative, this completely defeats the purpose. The trust cannot hold onto the money to protect it from creditors or poor spending habits without hitting that catastrophic 37% trust tax rate. Honestly, it's unclear why so many people still pay thousands of dollars for these complex structures when simpler options exist.

The Discretionary Accumulation Trust Trap

The alternative is an accumulation trust, which allows the trustee to hold the retirement funds inside the legal structure to protect the money from the beneficiary's bad decisions. As a result: you face the exact tax compression nightmare mentioned earlier. You are essentially choosing between exposing the money to a beneficiary's potential bankruptcy or handing a massive portion of it directly to the federal government in taxes. It is a classic rock-and-a-hard-place scenario where nobody wins.

Comparing Direct Beneficiary Designations to Trust Formations

When you take a step back and look at the numbers, bypassing the trust entirely and using standard beneficiary forms usually delivers a far superior financial outcome. It feels almost too simplistic, which explains why wealthy families often over-engineer the process.

The Seamless Transition of Direct Forms

Naming an individual persona—like a spouse or a child—directly on the IRA or 401k custodian's beneficiary designation form creates a clean, legally binding path that completely avoids the probate court anyway. When you die, the account transitions directly into an Inherited IRA for that person. There are no legal fees to pay, no ongoing trustee management fees, and no complex fiduciary tax returns to file every April. It happens automatically. Yet, people still insist on complicating things because they assume expensive legal structures are always better.

The Unique Protections of Eligible Designated Beneficiaries

There is a select group of people who are exempted from the 10-year liquidation rule under the law. These are called Eligible Designated Beneficiaries, or EDBs. This group includes surviving spouses, chronically ill or disabled individuals, and minor children of the account owner. A surviving spouse, for instance, can roll your traditional IRA directly into their own individual IRA and postpone required minimum distributions for years. If you mistakenly name a standard revocable living trust as the beneficiary instead of naming your spouse directly, you risk stripping them of this incredibly valuable legal privilege, forcing rapid distributions that could have been easily avoided.

Common mistakes and dangerous misconceptions

The phantom conduit trap

Many well-meaning planners blindly appoint a standard revocable living trust as the primary beneficiary of their traditional IRA. They assume it smoothly funnels money to their heirs. The problem is, standard boilerplate trust documents rarely contain the precise conduit clauses required by the IRS. Without these, the tax authority views the trust as a non-designated beneficiary. Boom. Your children must liquidate the entire account balance within a measly five years. They face a massive, immediate income tax bill. Why don't you put retirement accounts in a trust without hiring a specialized estate attorney? Because an ordinary estate planning document cannot navigate the post-SECURE Act landscape where tax-deferred growth must be fiercely protected.

The uniform tax rate delusion

People often imagine that money sitting inside a fiduciary structure gets taxed just like individual income. Let's be clear: trust tax brackets are brutally compressed. In 2026, a trust hits the top federal income tax bracket of 37% on retained income at just $15,650. For a single human being, that same peak bracket requires over $600,000 in earnings. If the trustee fails to distribute the required minimum distributions to the human beneficiaries before December 31, the trust itself pays the bill. The IRS swallows over a third of your hard-earned wealth instantly. It is fiscal suicide to let traditional retirement funds accumulate inside an accumulation trust without calculating this geometric disparity.

Ignoring the secure act 2.0 ripple effects

Amateurs frequently forget that legislation fundamentally rewrote the playbook for non-spouse beneficiaries. You cannot just rely on old advice from 2019. Under current rules, most adult children must completely empty an inherited IRA by December 31 of the tenth year following the owner's death. But if you shoehorn this asset into a rigid trust, the interaction between the ten-year rule and trust distribution mechanics becomes a logistical nightmare. The trustee is caught between a rock and a hard place: dump all the cash onto the beneficiary at once, potentially ruining them, or hold the cash and pay those punishing fiduciary tax rates.

The see-through solution and expert choreography

Mastering the look-through trust protocol

If you absolutely must use a legal entity to control your wealth after you pass away, it must be meticulously structured as a see-through trust. This is a highly specialized legal framework where the IRS agrees to look past the entity and analyze the underlying human beneficiaries. To qualify, the document must be valid under state law, it must be irrevocable upon your death, and all beneficiaries must be identifiable individuals. But even this advanced strategy requires extreme caution. If a single contingent beneficiary is an entity like a non-profit or a business, the see-through status vanishes completely. Why don't you put retirement accounts in a trust unless you have an exceptionally complex situation, such as a special needs child or a blended family dynamics? Because the compliance burden is suffocatingly high.

Frequently Asked Questions

Can a trust hold a Roth IRA without causing immediate negative tax consequences?

Yes, you can legally name a trust as the beneficiary of a Roth IRA, but the financial justification remains incredibly weak. Because Roth distributions are already tax-free, you avoid the compressed fiduciary tax bracket nightmare that plagues traditional accounts. Yet, the ten-year withdrawal rule established by the SECURE Act still applies to the entity, meaning the trust must completely empty the account within a decade. Think about it: why don't you put retirement accounts in a trust when a Roth IRA can grow completely tax-free for a full decade before a direct human beneficiary has to touch a single penny? By forcing the funds through a legal entity, you inject unnecessary administrative costs, trustee fees, and legal liabilities into an asset that was designed to be beautifully simple and maintenance-free.

What happens to an inherited 401k if it is left directly to an irrevocable trust?

When an employer-sponsored 401k plan is left to an irrevocable trust, the plan administrator usually demands an immediate, lump-sum liquidation of the entire balance. Unlike IRAs, many corporate 401k plans do not possess the administrative infrastructure or the willingness to manage ongoing lifetime distributions to a fiduciary entity. As a result: the entire account value is realized as ordinary taxable income in a single calendar year, destroying decades of compounding interest. This massive influx of cash triggers the highest possible tax brackets for the estate, leaving the actual heirs with a fraction of the original inheritance. It is a catastrophic operational failure that could easily be avoided by utilizing a direct beneficiary designation instead.

Are there any specific situations where putting a retirement plan in a trust is actually a smart move?

The only legitimate scenario involves protecting a highly vulnerable beneficiary who cannot manage money due to severe disability, substance abuse, or extreme spendthrift tendencies. In these rare instances, the severe tax penalties are accepted as a necessary cost for securing the physical well-being of a loved one. You are essentially trading financial efficiency for behavioral control and asset protection against predatory creditors or chaotic divorces. Except that even in these scenarios, you must utilize a customized Special Needs Trust or a highly restrictive discretionary trust rather than a generic family trust. For 95% of standard American families, the math simply does not add up, and the strategy backfires completely.

An uncomfortable truth about modern estate planning

The obsession with funneling every single piece of property through a comprehensive trust has blinded investors to basic mathematical reality. We have been conditioned by aggressive estate planning marketing to fear the probate court process at all costs. But here is the reality: naming an individual directly via a standard transfer-on-death beneficiary designation bypasses probate entirely, cleanly, and for free. Why don't you put retirement accounts in a trust? The answer is that doing so introduces an expensive, tax-inefficient layer of bureaucracy to an asset class that already possesses its own built-in, elegant mechanism for passing wealth across generations. Stop over-engineering your legacy based on outdated financial dogmas. Trust your heirs, protect your compounding growth, and keep Uncle Sam out of your retirement accounts by embracing the profound simplicity of direct beneficiary designations.