Let's be real about the industry marketing for a second. We have all seen the slick seminars promising that a revocable living trust solves every conceivable earthly problem, from probate avoidance to shielding your estate from a bitter ex-spouse. But that changes everything when you actually look at how the tax code treats different types of property. A trust is a powerful legal vehicle, yet it is far from an all-purpose dumpster where you can just toss your life's savings and walk away. Some assets are inherently incompatible with trust ownership because their tax classification is tied strictly to individual human status, not artificial legal entities. When you strip that individual ownership away, the legal machinery grinds to a halt, or worse, backfires on your beneficiaries.

Understanding the Boundaries: Why Shifting Ownership Is Not Always a Great Idea

To understand what assets should not go in a trust, we first have to dissect what actually happens when you fund one of these structures. You are changing the legal title of your property from your own name to that of the trustee. Now, if we are talking about a standard revocable living trust, the IRS largely ignores this during your lifetime because you maintain total control, but state laws and specific asset custodians operate on entirely different wavelengths. The issue remains that certain contracts and equity structures contain strict transfer restrictions that trigger immediate liquidity events the moment a transfer document is executed.

The Disconnect Between Legal Entities and Individual Tax Perks

The IRS grants massive tax breaks to individual human beings that it completely denies to non-human entities. Think about your primary residence. Under Internal Revenue Code Section 121, an individual can exclude up to $250,000 of capital gains—or $500,000 for married couples—when selling a home they have lived in for two out of the last five years. Move that house into the wrong kind of irrevocable vehicle, and you might just wave goodbye to that exemption. Why? Because the trust is now the owner, and a pile of legal paper cannot physically reside in a house to claim a primary residence perk. Experts disagree on the exact workaround strategies here, and honestly, it is unclear how some aggressive strategies will hold up under future audit cycles, but the risk is glaringly obvious.

When Asset Custodians Push Back on Funding Requests

Then there is the sheer logistical friction of dealing with traditional financial institutions. You might sign a beautiful, gold-embossed trust agreement in your lawyer’s office in Boston, but when you take that document to a retail bank teller to rename your checking account, you hit a brick wall. Financial institutions have their own internal compliance departments, and they are terrified of fraud. As a result: they often require exhaustive certification documents, or they might simply refuse to honor the trust terms without a court order, meaning your attempt to streamline your estate just added three layers of red tape.

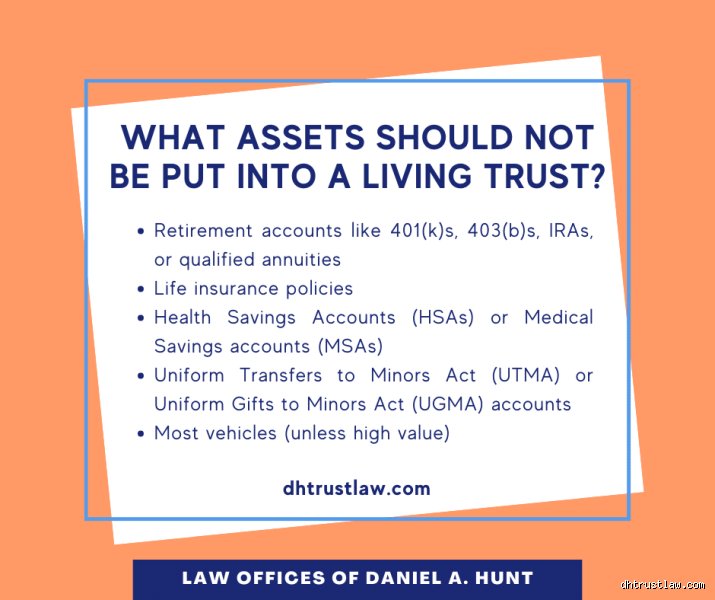

The Absolute Red Lines: Accounts That Trigger Mass Tax Penalties

Where it gets tricky—and frankly, dangerous—is with qualified retirement accounts like your traditional IRA, 401k, or 403b. If you take away nothing else from this analysis, remember this rule: never, under any circumstances, transfer the actual ownership of a qualified retirement account to a trust during your lifetime. Doing so is treated by the IRS as an immediate, 100% taxable distribution of the entire account balance. Imagine transferring a $1.2 million 401k into a trust in June; by April of the following year, you will owe federal and state income taxes on that entire lump sum as if you cashed it out to go to Vegas.

The SECURE Act Disaster and Conduit Trusts

But what about naming a trust as the beneficiary of your IRA after you die? People don't think about this enough, but Congress completely rewrote the playbook with the passage of the SECURE Act, which took effect on January 1, 2020. Before that date, if you named a trust as your IRA beneficiary, the trust could often stretch out the required minimum distributions over the lifetime of the oldest human beneficiary, keeping the tax hit minimal. Not anymore. Now, unless the beneficiary is an Eligible Designated Beneficiary—like a spouse or a chronically ill individual—the entire account must be completely emptied within 10 years.

If you used a traditional conduit trust structure designed before 2020, that means all those forced RMDs must pass straight through to the beneficiary anyway, completely defeating any asset protection goals you had. But wait, what if you use a accumulation trust instead to keep the money away from a spendthrift child? That is where the tax knife cuts deep. Any money trapped inside an irrevocable structure is subject to highly compressed tax brackets. For the tax year, a trust hits the maximum federal income tax rate of 37% at just $15,650 of retained income, whereas an individual doesn't hit that peak until their income passes $626,350. That is an astronomical penalty for a lack of foresight.

S-Corporation Stock and the Threat of Disqualification

Another minefield involves small business ownership, specifically S-Corporation shares. The IRS imposes incredibly rigid restrictions on who can own stock in an S-Corp to ensure it maintains its pass-through tax status. Only individuals, estates, and very specific types of trusts are allowed on the shareholder cap table. If you mistakenly transfer your S-Corp shares into a standard foreign asset protection trust or an unapproved irrevocable structure, you instantly disqualify the entire corporation’s S-status. The company ceases to be a pass-through entity and is immediately taxed as a C-Corporation. Can you picture the look on your business partners' faces in Chicago when they realize your estate planning blunder just subjected the entire enterprise to double taxation?

The Operational Logistical Nightmares: Vehicles and Day-to-Day Cash

Moving away from the pure tax disasters, let us talk about the everyday assets that create operational chaos when placed inside a trust. Your personal vehicles, your boat, and your daily checking accounts fall squarely into this category. It sounds great on paper to say everything you own is held by your trust, but the practical reality of managing these assets under a trustee title is an exercise in futility.

Why Titling Cars and Boats to a Trust Fails the Common Sense Test

Take your everyday driver, say a 2024 Ford Explorer. If you title that vehicle in the name of your trust, you will immediately run into a brick wall with your auto insurance carrier. Most consumer auto insurers do not know how to underwrite a vehicle owned by a legal entity rather than a human driver. They will either force you to switch to a commercial fleet policy—which can easily double your premiums—or they will deny coverage entirely if you get into a fender bender on Route 9. Except that the DMV will also charge you administrative fees to process the title change, meaning you are spending cash and increasing your liability just to keep a depreciating asset out of a probate process that it might have been exempt from anyway due to small estate thresholds.

The Trap of Transferring Active checking Accounts

Then there is your primary checking account, the one you use to pay the electric bill, buy groceries, and receive your bi-weekly direct deposits. I strongly argue against putting this specific account into a trust wrapper. While it is perfectly fine to move long-term savings accounts or brokerage portfolios over, your active cash flow needs to remain nimble. Many payment apps, international wire systems, and peer-to-peer lending platforms flag transactions originating from accounts titled as trusts. It triggers fraud alerts because the software thinks a corporate entity is masquerading as a private consumer. Keep your operational cash in your own name and simply utilize a payable-on-death designation to ensure it transfers seamlessly when you pass away.

Strategic Alternatives: Better Ways to Protect Your Vulnerable Assets

Since we have established that cramming everything into a trust is a recipe for financial self-sabotage, what are the actual alternatives? You do not have to leave these assets completely exposed to the elements or destined for a grueling multi-year probate court battle. There are simpler, cleaner legal mechanisms designed specifically to handle the property that trusts reject.

Using Beneficiary Designations as a Precision Tool

For retirement accounts and life insurance policies, the solution is beautifully simple: the Transfer-on-Death (TOD) or Payable-on-Death (POD) designation. These statutory instruments bypass probate completely because they operate as a matter of contract law. When you pass away, the beneficiary simply presents your death certificate and their identification to the custodian, and the assets transfer directly into their name within weeks. No lawyers, no trustee fees, and absolutely no compressed trust tax brackets to worry about. It is clean, it is fast, and it keeps the IRS out of your pockets.

Corporate Formations for Active Business Assets

If you are trying to shield an active business, real estate investments, or high-risk ventures, a trust should not be your first line of defense anyway. That is what Limited Liability Companies (LLCs) are built for. By holding your real estate or business operations inside an LLC, you isolate the liability to that specific entity, protecting your personal wealth from lawsuits. If you still want the estate planning benefits of a trust, you can then transfer the membership interest of the LLC into your trust, rather than the raw assets themselves. It is a layered approach that gives you the best of both worlds without breaking any IRS rules regarding S-corporation eligibility.

Common Misconceptions Surrounding Trust Funding

The Myth of the All-Inclusive Safety Net

People love the idea of absolute protection. You set up a revocable living trust, transfer everything you own into it, and assume the job is finished. The problem is that dumping every single asset class into a trust creates massive administrative headaches and potential tax traps. For instance, transferring your everyday checking account might seem logical, but it frequently disrupts automated bill payments and direct deposits. Why complicate your life? Keep a baseline operating account in your individual name to handle daily financial friction. Some vehicles simply resist the trust structure due to inherent institutional friction.

Misunderstanding Retirement Asset Mechanics

Can you transfer your Traditional IRA or 401k directly into a trust during your lifetime? Absolutely not. Attempting a direct transfer triggers an immediate, catastrophic tax event. The IRS views this clumsy maneuver as a 100% total distribution. As a result: you face a massive income tax bill on the entire balance in a single tax year. Let's be clear about how this works. You do not change the ownership of the account itself; instead, you strategically adjust the beneficiary designation forms to coordinate with your estate plan after your death. Yet, even this secondary step requires surgical precision to avoid accelerating mandatory distribution timelines for your heirs.

The Real Estate Transfer Trap

Putting real estate into a trust sounds like standard operating procedure, except that certain properties carry hidden liabilities. Consider heavily mortgaged properties. Transferring real estate without checking the lender's guidelines can inadvertently trigger a due-on-sale clause, forcing an immediate loan acceleration. While federal law protects primary residences transferred into revocable trusts, commercial properties and multi-family units do not enjoy the same blanket immunities. Furthermore, foreign real estate often clashes violently with domestic trust laws, causing double taxation nightmares in overseas jurisdictions.

The Hidden Friction of Vehicle Transfers and Liability

Why Your Daily Driver Belongs on Your Personal Ledger

Titling your commuter car or family SUV in the name of your trust is generally a administrative blunder. The issue remains that insurance companies view trust-owned vehicles through a lens of profound suspicion. They often demand commercial auto policies, which can hike your annual premiums by 40% to 60% compared to standard personal coverage. Why pay an inflated premium for an asset that depreciates by 15% the moment it leaves the lot? Unless you are dealing with an exotic classic car collection valued over $500,000, keep vehicles out of your trust. Personal liability umbrella policies offer a far more efficient shield against automotive lawsuits than any trust wrapper ever could.

The Operational Chaos of Active Small Businesses

Operating business interests demand specialized handling. If you hold shares in an S-Corporation, transferring them requires strict adherence to internal revenue codes. Only specific types of trusts qualify to hold S-Corp stock; messing this up can instantly destroy the corporation's tax status, harming your business partners. What assets should not go in a trust? Active, operational partnerships where the trustee lacks the day-to-day expertise to manage corporate votes are prime candidates for exclusion. It is far wiser to utilize buy-sell agreements or transfer-on-death provisions to transition corporate power cleanly.

Frequently Asked Questions

Can I put my personal checking account into a living trust?

Yes, you can physically retitle a standard checking account, but doing so often creates more operational friction than it resolves. Most financial institutions require you to close the existing account and open a brand-new one under the trust's tax identification number, which instantly breaks all your linked subscription services and direct deposits. Statistics indicate that the average American household has 6 to 8 automated recurring payments attached to their primary checking account. If you insist on retitling it, you must meticulously audit these connections to avoid missed payments and penalties. A practical alternative is simply establishing a payable-on-death designation, which transfers the cash instantly to your heirs while bypassing probate entirely.

What happens if I accidentally transfer my IRA into a trust?

An accidental transfer of an individual retirement account is a financial emergency that triggers immediate taxation. The IRS treats this misstep as an unallowable assignment of the contract, forcing the entire balance to become taxable income within that specific calendar year. For an individual with a $400,000 retirement balance, this sudden spike could push them into the highest federal tax bracket of 37%, wiping out over one-third of their nest egg instantly. (And that is before you calculate potential state income taxes or early withdrawal penalties if you are under age 59.5). Rectifying this mistake requires immediate, complex unwinding procedures that financial institutions rarely execute without significant pushback.

Should out-of-state real estate be placed in a revocable trust?

Out-of-state real estate is actually one of the most compelling reasons to utilize a trust structure. If you die owning land in multiple jurisdictions, your estate faces the grueling, expensive nightmare of ancillary probate proceedings in every single state where property is registered. Legal fees for ancillary probate can easily consume 3% to 5% of the property's total market value. Placing that Florida vacation home or Montana ranch into your primary revocable trust consolidates your estate under a single governing entity. This simple administrative pivot streamlines the ultimate distribution process, saving your grieving family months of cross-border legal red tape.

A Strategic Stance on Asset Selection

Blindly stuffing every possession into a trust is a recipe for administrative gridlock. Wealth management requires an understanding of where boundaries lie. We must realize that the legal fiction of a trust is a precision instrument, not a oversized storage unit for your entire life. You do not need to wrap your daily checking account or your depreciating minivan in a complex legal shroud just because an estate planning checklist suggested it. True asset protection coordinates diverse mechanisms like beneficiary designations, corporate structures, and robust insurance policies alongside your trust. Let us reject the lazy, all-in approach and instead build a balanced estate framework that respects operational reality.