The Great Delusion: Why Today's Bear Market is a Mathematical Trap

The Illusion of the Lithium Glut in Western Markets

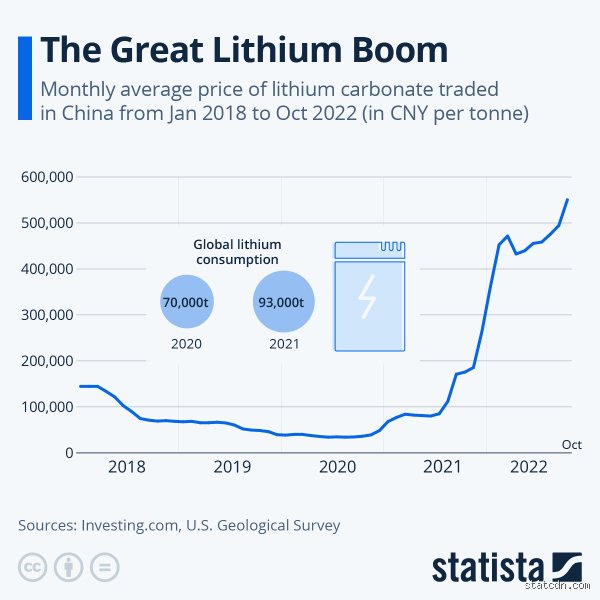

Commodity markets possess a cruel sense of irony. Right now, mainstream financial analysts are busy writing obituaries for the green transition because carbonate spot prices collapsed from their dizzying 2022 peaks. It is a classic trap. What they are missing is that current low prices have already triggered massive project deferrals across Western Australia and the Chilean salars. But the thing is, you cannot simply flip a switch to restart a multi-billion-dollar extraction project when demand inevitably spikes. It takes roughly seven to ten years to bring a greenfield spodumene mine online.

Because major producers like Albemarle and SQM have slashed capital expenditure budgets over the last eighteen months, the supply pipeline for 2028 and beyond is actively drying up. Meanwhile, global battery manufacturing capacity continues to expand relentlessly. The math does not add up for the bears. We are systematically underinvesting in the very infrastructure needed to prevent a structural deficit, which explains why this current lull is merely the quiet before a spectacular macroeconomic storm.

Chasing the Ghost of the 2022 Speculative Peak

Everyone remembers when lithium carbonate prices skyrocketed past $80,000 per metric ton in late 2022. That was not a sustainable boom; it was a speculative fever dream driven by panic-buying from Chinese cathode manufacturers who overordered because they feared getting left behind. People don't think about this enough: a healthy boom is built on structural scarcity, not supply-chain hysteria. I am convinced that the next price surge will be far more calculated, driven by strict automotive procurement mandates rather than spot-market gambling. Yet, retail investors are still waiting for a carbon copy of the last cycle, which is a mistake because the market has matured significantly since then.

Decoding the True Drivers of the Next Lithium Supercycle

The Gigafactory Explosion and the Realities of Battery Throughput

Let us look at raw industrial capacity instead of volatile trading charts. As of mid-2026, there are over 400 gigafactories either operational or under construction globally, representing a combined capacity that requires millions of tons of high-purity lithium chemicals annually. Where it gets tricky is the chemical specification. A battery does not just take raw dirt; it requires ultra-pure, battery-grade lithium hydroxide or carbonate with microscopic tolerance for impurities like iron or sodium. If a single batch is off by a few parts per million, the entire production run of electric vehicle cells becomes a fire hazard or a pile of expensive scrap.

This technical barrier is precisely why minor supply additions from lepidolite mining in China cannot solve the looming deficit. That changes everything because it creates a bifurcated market where high-quality, Tier-1 producers command massive premiums while inferior supply goes unused. Consider the sheer scale of the Northvolt Ett plant in Sweden or Tesla's ongoing expansions in Texas—these facilities require steady, predictable, multi-decade off-take agreements. Do you honestly believe a handful of artisanal operations in Africa or unproven direct lithium extraction technologies can meet that rigorous automotive standard? We're far from it, and that realization is going to hit the automotive supply chain like a freight train by 2029.

The Geopolitical Tug-of-War Over Critical Minerals

Geography is destiny when it comes to the energy transition. China currently controls over 60 percent of global lithium refining capacity, creating a dangerous choke point that Western policymakers are desperately trying to dismantle through legislation like the United States' Inflation Reduction Act. But rewriting global supply chains takes more than just signing executive decrees in Washington or Brussels. Except that money alone cannot bypass environmental permitting laws or local community resistance in places like Nevada or the pristine landscapes of Portugal.

The geopolitical reality is that Western automakers are legally barred from using supply chains tied to foreign entities of concern if they want to qualify for consumer tax credits. Consequently, a massive, localized premium is developing for domestic or free-trade-agreement-compliant material. It is an artificial fragmentation of a global commodity market. This means that even if the global aggregate balance sheet shows a slight surplus, Western car manufacturers will still face an acute shortage of legally compliant, ethically sourced material, hence forcing a localized price explosion that will decouple Western contracts from the Shanghai spot price.

The Supply Bottleneck: From Hard Rock to South American Brines

The Structural Friction of Scale-Up Operations

Mining is inherently messy, unpredictable, and capital-intensive. In the lithium sector, you essentially have two distinct production methodologies: extracting spodumene from hard-rock pegmatite deposits, predominantly found in Western Australia's Greenbushes mine, or pumping lithium-bearing brines from beneath the hyper-arid flats of the South American Lithium Triangle. Both have distinct vulnerabilities. Hard-rock mining is energy-intensive and produces massive amounts of tailings, but it boasts a faster processing timeline from mine to chemical plant.

Brine operations, conversely, rely heavily on solar evaporation ponds that can take up to 24 months to concentrate the liquid to a usable grade. The process is painfully slow. And what happens when climate patterns disrupt these fragile ecosystems? In the Salar de Atacama, water scarcity has become a battleground, pitting multinational mining conglomerates against indigenous communities and agricultural interests. As a result: production permits are becoming increasingly difficult to secure, creating an invisible ceiling on how much volume can actually be extracted regardless of how high the market price climbs.

The Direct Lithium Extraction Wildcard

Every venture capitalist is currently obsessed with Direct Lithium Extraction, or DLE, promising it will revolutionize the industry by pulling the metal straight out of brine streams in hours rather than years. It sounds beautiful on paper. In practice, however, commercial-scale DLE remains largely unproven at the massive volumes required to move the global supply needle. The technology is highly bespoke; a chemical framework that works perfectly on a specific brine composition in Argentina might completely fail when applied to the geothermal waters of the Salton Sea in California or the oilfield brines of Alberta. Experts disagree fiercely on the scalability of these systems, and honestly, it's unclear whether DLE will be a savior or a multi-billion-dollar sinkhole for early adopters over the next five years.

Substitution Myths: Why Sodium-Ion Won't Save the Automotive Sector

The Energy Density Boundary Wall

Every time lithium prices tick upward, headlines proclaim that sodium-ion or solid-state alternatives will render the metal obsolete. It is a fundamental misunderstanding of basic chemistry. Sodium sits directly below lithium on the periodic table, meaning it is inherently heavier and possesses a lower electrochemical potential. You can build a perfectly functional sodium-ion battery for a stationary energy storage system or a tiny, short-range urban commuter vehicle where weight does not matter. But for a premium long-range SUV or a commercial delivery truck? The physics simply do not work. To achieve a 300-mile range with sodium, the battery pack would be so heavy that it would neutralize the vehicle's payload capacity, which explains why mainstream automotive platforms remain entirely locked into lithium-based chemistries for the foreseeable future.

The Ironclad Supremacy of LFP and High-Nickel Chemistries

The market has largely coalesced around two primary pathways: Lithium Iron Phosphate for mass-market vehicles and high-nickel NMC for premium performance. Both require massive amounts of the white gold. Even with the rapid adoption of LFP chemistries across Europe and North America—a trend pioneered by Chinese giants like BYD—the demand for carbonate remains relentless. In short, alternative battery chemistries are not a threat to the market; they are a necessary release valve to prevent the entire electric vehicle transition from grinding to a halt due to absolute structural material shortages.

Common mistakes and misconceptions about the battery metal market

The illusion of a monolithic lithium market

Investors frequently track lithium as if it were gold or crude oil. It is not. The primary blunder is assuming a single, uniform commodity price dictates the entire ecosystem. Lithium carbonate and lithium hydroxide serve completely different battery architectures, with the latter requiring rigorous, high-purity chemical processing that many junior miners simply cannot achieve. The problem is that a massive spike in global lepidolite or spodumene mining capacity does not automatically translate into battery-grade material. High-nickel cathodes demand precise chemical specifications, which explains why top-tier automakers bypass open spot markets entirely to sign exclusive, multi-year supply agreements with tested refiners.

The recycling savior complex

Everyone loves a perfect circular economy narrative. We assume that millions of spent electric vehicle batteries will seamlessly plug the supply gap by 2030. Except that the math is completely broken. Scrap volume is currently negligible because older electric cars are staying on the road far longer than early statistical models anticipated. Furthermore, hydrometallurgical recycling facilities face immense technical hurdles and razor-thin margins when processing diverse, non-standardized battery packs. Let's be clear: recycling will not prevent a lithium shortage over the next decade; it is a late-2030s story at best.

The geopolitics of the processing bottleneck

Where the real white gold monopoly hides

You probably think the country digging the rock out of the ground holds all the leverage. Think again. Australia dominates raw extraction, and South America sits on the largest brine reserves, yet China controls over 60 percent of global refining capacity. Why does this matter? Because a mining company can unearth thousands of tons of raw material, but if they must ship it to Yibin or Chengxin for chemical conversion, the geographic risk remains entirely unchanged. (Western nations are scrambling to fund domestic processing, but building a chemical plant takes years of environmental permits and specialized engineering expertise).

Is lithium going to boom if the West builds its own independent supply chains? The financial reality is brutal. Building a fully integrated lithium refinery in North America or Europe costs up to twice as much as constructing an identical facility in Sichuan. This economic disparity creates a massive dilemma for automakers who need cheap cells to make electric vehicles affordable for the mass market.

Frequently Asked Questions

Is lithium going to boom again like it did during the historic 2022 price peak?

A repeat of the astronomical 2022 price surge where spot prices breached $80,000 per ton is highly improbable due to structural market maturing. The issue remains that the wild volatility of the past was driven by speculative panic and empty supply pipelines, whereas the current market features sophisticated hedging instruments and massive corporate stockpiles. However, a structural demand expansion is projected to push the market into a deficit of 300,000 metric tons of lithium carbonate equivalent by 2030. As a result: we will witness a sustained, healthier demand cycle rather than an erratic, short-lived price spike. Sharp capital investment declines in 2024 and 2025 guarantee that when the next supply crunch hits, the price floor will sit significantly higher than historical averages.

Can alternative battery chemistries like sodium-ion kill the lithium boom?

Sodium-ion technology represents a fascinating diversification tool for stationary energy storage and ultra-cheap, low-range urban vehicles, but it poses zero existential threat to high-performance applications. The core limitation stems from energy density, as sodium cells deliver roughly 160 watt-hours per kilogram compared to the 300 watt-hours per kilogram achieved by advanced lithium-ion formulations. Automakers cannot compromise on driving range for mainstream consumer SUVs and long-haul trucking platforms. Consequently, alternative chemistries will merely act as a safety valve to absorb excess low-end demand, which actually stabilizes the broader market. Lithium will maintain its iron grip on the premium automotive sector for the foreseeable future.

Which extraction method will dominate the next decade of production?

Traditional hard-rock spodumene mining in regions like Western Australia will maintain its dominant market share for the next five years due to its established infrastructure and predictable yields. Meanwhile, South American brine operations using conventional evaporation ponds are facing unprecedented regulatory scrutiny and intense local community opposition regarding water usage in the Atacama desert. This friction accelerates the commercial deployment of Direct Lithium Extraction technologies, which promise to pump brine, strip the metal in hours, and reinject the water back underground. But can these unproven, capital-intensive filtration systems scale up fast enough to meet the impending automotive demand wave? Early pilots in Arkansas and Argentina suggest commercial viability is real, but scaling them up requires billions in unproven infrastructure investments.

The ultimate verdict on the lithium boom

The era of easy money in the battery sector is dead, replaced by a ruthless landscape where only the most efficient, geographically secure projects survive. We are moving away from speculative hysteria and entering a phase of industrial consolidation. Do not buy into the myth that alternative chemistries will make this metal obsolete overnight. Our global energy transition relies entirely on electrochemical realities that cannot be bypassed by wishful thinking or political decrees. The next market expansion will not lift all boats equally; it will handsomely reward high-purity chemical refiners while punishing junior explorers with nothing but unproven dirt. Prepare for a prolonged, strategic market upswing that rewards cold engineering metrics over flashy promotional slide decks.