The Hidden Friction in Your Monthly Books: Why Matching Numbers Matters

Most business owners look at their bank balance and assume that number represents reality. It does not. The actual cash you have available to spend exists in a state of constant flux because of outstanding checks, pending deposits, and the administrative friction of modern banking. Think of it as a delayed echo; what happened in your warehouse on Tuesday might not show up on the bank ledger until the following Friday. Because of this lag, the process of bank reconciliation acts as an internal audit system, an early warning radar for fraud, and your only real defense against overdraft fees.

The Anatomy of the Discrepancy

Where it gets tricky is understanding that differences between your internal ledger and the bank statement are not always errors. In fact, they rarely are. More often than not, you are looking at timing differences, such as a $14,500 vendor payment mailed on June 28, 2026, which the recipient will not deposit until July. The bank is not wrong, and neither are you—you are simply looking at two different moments in time captured on the same piece of paper. People don't think about this enough, but if you treat every variance as a mistake, you will waste hours chasing ghosts through your software.

A History of Ghost Balances

I once audited a regional logistics firm in Chicago that carried a persistent $42,000 variance for three quarters because nobody bothered to look at the outstanding deposits from an old payroll account. They just assumed the software would magically fix it. That changes everything when you realize that unresolved discrepancies compound over time, turning a tiny bookkeeping hiccup into an absolute nightmare during tax season. Experts disagree on how frequently small businesses should reconcile, but honestly, it's unclear why anyone would risk waiting longer than thirty days to verify their cash.

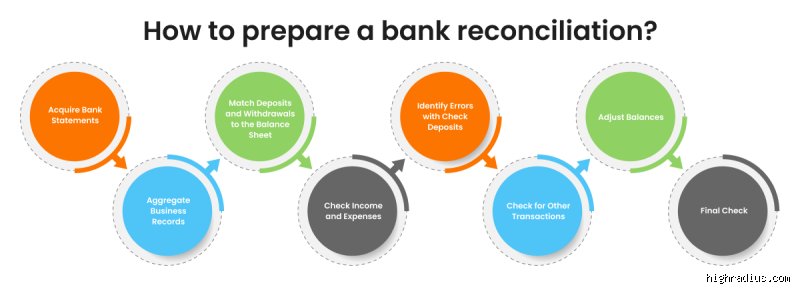

Step-by-Step Execution: Preparing Your Financial Arena

Before you even think about opening your accounting software, you need to gather your raw materials. This means pulling the internal general ledger for the specific target period—let's say June 1 to June 30, 2026—and matching it with the corresponding bank statement. Do not try to cut corners here by using partial data. You need the full, unvarnished history of every transaction, every wire transfer, and every automated clearing house settlement that occurred during those thirty days.

Gathering the Raw Data

The thing is, your internal records are biased toward your own actions. When you cut a check, you record it instantly, but the bank knows nothing about it until that slip of paper physical lands at another branch. Consequently, the first phase of how do you perform bank reconciliation involves establishing your two starting points: the ending cash balance from your bank statement and the ending balance of the cash account in your general ledger. If these two numbers match right out of the gate, congratulations, you have achieved a statistical miracle that happens about once a career.

The Preliminary Screen

Start with a high-level scan to catch the obvious culprits. Look at the total deposits and total withdrawals on both sides to see if the macro-numbers align because this quick check can immediately isolate which side of the equation holds the bulk of the variances. Did a client send an international wire transfer that incurred an unexpected $35 intermediary fee? Or perhaps an automated utility payment cleared for a slightly different amount than the estimated invoice you entered into the system? Identifying these glaring differences early saves you from the tedious line-by-line grind later on.

Isolating the Common Culprits

But what happens when the macro-numbers are completely skewed? That is when you must look for specific transaction types that notoriously cause friction in corporate accounting. Nonsufficient funds (NSF) checks from customers are particularly frustrating because your ledger says you received the money, but the bank has quietly clawed it back after the check bounced. Which explains why your internal cash balance looks artificially inflated until you manually adjust for the bad debt and the associated bank penalty.

Advanced Matching Diagnostics: Chasing the Elusive Pennies

Now comes the heavy lifting where you compare every single line item on the bank statement against your internal journals. You are looking for a perfect match in both date and amount, ticking off transactions one by one like a detective building a case. Yet, even with modern automated feeds, human error manages to creep into the system with alarming regularity.

The Perils of Manual Data Entry

Transposition errors are the bane of every bookkeeper's existence. You intend to type a check amount as $8,912, but your fingers slip, and it gets recorded in the general ledger as $8,192 instead. The bank clears the correct amount, leaving you with a baffling $72 discrepancy that defies easy explanation. A quick trick for finding these annoying mistakes is to divide the total variance by nine; if it divides evenly, you are almost certainly dealing with a transposed pair of numbers. Why does this mathematical quirk work? It is just the way our base-ten numerical system behaves when digits swap places, though most people look at you like you are practicing sorcery when you demonstrate it.

Adjusting the Bank's Perspective

To find the true, adjusted cash balance, you have to modify the bank's ending figure by adding any deposits in transit that have not yet cleared and subtracting any outstanding checks that are still floating out in the wild. As a result: you create a temporary, simulated balance that reflects what the bank account will actually look like once the physical world catches up with your digital records. If you skip this step, you are essentially flying blind, making strategic business decisions based on a fictional pool of liquidity that does not actually exist.

Alternative Reconciliation Philosophies: Software Versus the Ledger

The conventional wisdom touted by cloud accounting platforms is that manual bank reconciliation is dead. They want you to believe their artificial intelligence algorithms can handle everything automatically through live bank feeds, requiring nothing more from you than a casual click of an "approve" button. We're far from it, unfortunately.

The Myth of Total Automation

While automated matching rules are fantastic for recurring, predictable transactions like your monthly office rent or SaaS subscriptions, they break down spectacularly when faced with complex, multi-invoice vendor payments. If a customer sends a single lump-sum wire of $50,000 to cover four separate invoices from three different months, the software usually panics or, worse, guesses incorrectly. The issue remains that blind reliance on automation creates a false sense of security, burying systemic errors under a veneer of digital efficiency. A hybrid approach, where technology handles the bulk matching but a human eye reviews the anomalies, remains the gold standard for any organization that values financial integrity.

Common Pitfalls and Costly Blind Spots

Most accounting teams treat the monthly matching ritual as a mechanical checkboxes exercise. They are wrong. When you perform bank reconciliation, you are actually auditing human fallibility and institutional friction. A single typo can throw off an entire fiscal quarter, yet teams hunt for the wrong ghosts.

The Trap of Timing Discrepancies

Outstanding checks and deposits in transit are not errors; they are merely temporal ghosts. You write a check to a vendor for $4,500 on June 28, but they do not cash it until July 5. The ledger shows a depletion that the bank account ignores. New bookkeepers panic here and try to force a balance by inventing adjustment entries. Let's be clear: forcing the numbers to match without identifying the underlying lag is a recipe for compliance disasters. Why do we assume the ledger is always the source of absolute truth?

Ignoring the Insignificant Leakage

A $3 bank fee seems trivial. Because it is small, you might ignore it until the end of the year. The problem is that these micro-charges compound across multiple entities and accounts. Merchant processing fees, wire fees, and foreign exchange adjustments eat away at cash reserves like digital termites. If you do not reconcile these fees during your standard monthly workflow, your net income figures remain skewed by dozens of tiny, unrecorded expenses. Over a trailing twelve-month period, a firm with $5,000,000 in revenue can easily misplace $12,000 in unmonitored bank penalties.

The Hidden Mechanics of Unmatched Data

Every seasoned CFO understands that the real magic happens outside the standard matching software algorithms. Automated systems match roughly 85% of transactions based on exact dollar amounts and dates. The remaining 15% require genuine detective work. This is where you truly learn how to execute bank account balancing rather than just letting a machine guess.

The Anatomy of Asymmetric Transactions

Consider the nightmare of a single lump-sum bank deposit that represents four separate customer invoices. Your software looks for a single credit of $18,250, but your bank statement shows exactly that amount as a solitary line item. Meanwhile, your internal ledger lists four separate receipts of $5,000, $6,000, $4,250, and $3,000. The automated rules fail instantly. You must manually reconstruct the deposit slip data to bridge this visibility gap (which explains why modern accounting still requires human analytical oversight). Except that most teams lack the forensic patience to dig into the bank's underlying batch details, leaving items dangling for months.

Frequently Asked Questions

How often should a growing business perform bank reconciliation to ensure accuracy?

While traditional small firms reconcile their cash accounts every 30 days, any operation generating over 500 transactions monthly should transition to a daily reconciliation cycle. Waiting until the end of the month means your finance team must investigate discrepancies that are already four weeks cold. A recent study by the Association of Certified Fraud Examiners revealed that organizations practicing daily cash matching reduce their average fraud discovery window from 14 months down to less than 30 days. Furthermore, daily visibility ensures that your reported cash positions are 100% accurate for sudden capital allocation decisions. As a result: your executive team can spot cash flow bottlenecks before they threaten operational payroll obligations.

What specific steps should you take when an unresolved variance persists?

First, isolate the exact discrepancy by calculating the difference between your adjusted ledger balance and the bank statement summary. If the variance is perfectly divisible by 9, you are almost certainly dealing with a transposition error where a clerk wrote $54 instead of $45. Next, scrutinize the prior month's outstanding items to ensure no old check was double-counted or voided incorrectly. If the discrepancy remains completely static after these checks, you must pull the actual bank statement images to verify that the bank itself did not commit a processing error. The issue remains that banks are run by humans too, and processing missteps happen far more often than corporate software developers care to admit.

Can specialized accounting software completely automate the cash reconciliation process?

No software platform can entirely eliminate the need for human oversight during complex financial matching routines. While modern ERP systems utilize optical character recognition and machine learning to achieve an 88% automated match rate, they stumble on non-standard reversals, bounced checks, and international wire discrepancies. When a customer triggers a chargeback, the bank pulls funds immediately without notifying your internal ledger. An automated system cannot guess the strategic context behind that sudden withdrawal. In short, automation handles the tedious heavy lifting, but human intuition remains mandatory to untangle the inevitable edge cases that digital algorithms misinterpret.

The Definitive Stance on Financial Fidelity

Treating cash verification as a secondary administrative chore is a dangerous corporate delusion. When you reconcile corporate bank records, you are protecting the foundational bedrock of your entire business intelligence apparatus. Clean books are not a luxury designed for the amusement of external auditors. They are the only shield you have against operational blindness and internal fraud. If your cash numbers are a fuzzy approximation, every single strategic choice you make is based on a fiction. Stop looking at reconciliation as a retroactive compliance burden and start viewing it as real-time financial defense.