The Historical Trap: Why Your Modern Brain Struggles with Left and Right Ledger Entries

The Venetian Legacy of Luca Pacioli

We have to blame a 15th-century Franciscan friar named Luca Pacioli for this mental gymnastics, though he merely documented a system merchants in Venice had used for decades to track spice voyages. People don't think about this enough: accounting was not invented for modern tax software, but for wooden ships exposed to piracy and storms. When a merchant purchased silk in Genoa in 1494, they needed a dual tracking mechanism. If you only write down that your cash decreased, how do you track what that cash turned into? You cannot. Because of this, Pacioli popularized the double-entry method, utilizing the Latin terms *debere* (what is owed) and *credere* (what is entrusted), which mutated over half a millennium into our modern abbreviations: Dr. and Cr.The Retail Banking Illusion That Distorts Reality

Where it gets tricky is your personal bank account. When the bank sends a notification saying they have credited your account, you celebrate because your balance went up. But have you ever paused to think about whose perspective that ledger represents? Hint: it is not yours. To the bank, your deposit is a massive liability because they eventually have to give that cash back to you. When you hand over five thousand dollars to a teller, the bank debits their own cash asset account and credits a liability account called "Customer Deposits." You are viewing their books backward. Honestly, it's unclear why schools don't teach this distinction early on, given how many small business owners bankrupt themselves by misinterpreting their own cash flows based on this exact misunderstanding.The Core Mechanics: How the Five-Finger Rule Dictates Financial Movement

The Accounting Equation as an Unyielding Scale

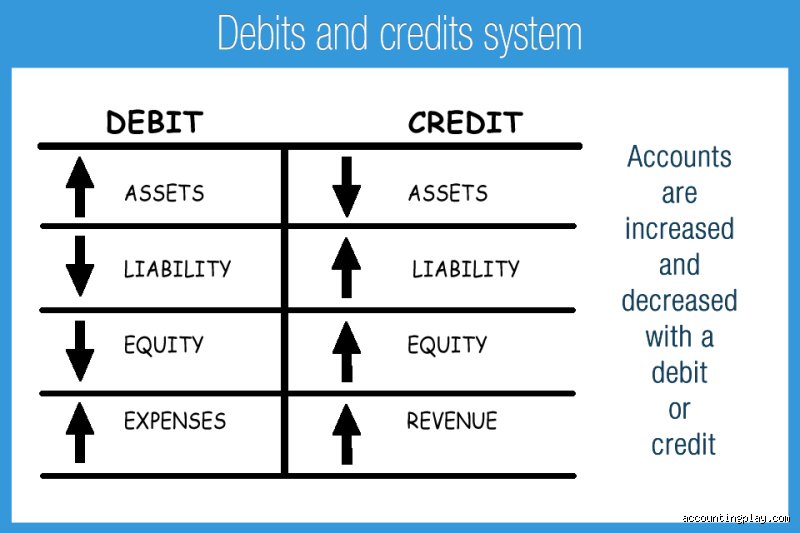

Everything rests on one elegant formula: Assets equal Liabilities plus Equity. This equation must balance, always, with an almost religious certainty. Yet, beginners stumble because a debit increases some accounts but actively decreases others. I take a very firm stance on this: if you try to memorize every combination of accounts without understanding the underlying equation, you will fail within your first month of corporate bookkeeping. Let us look at how it actually moves. Assets—things you own like land, inventory, or a 2024 Ford F-150 transit van—increase with a debit and decrease with a credit. Conversely, liability accounts (what you owe to suppliers or the bank) and equity accounts (the owner's residual stake) operate in the exact reverse manner, increasing with a credit and decreasing with a debit.The Revenue and Expense Paradox

But what about the operational side of a business? This is where the thing is: revenue and expenses are merely sub-components of equity, dragging it up or down as the fiscal year progresses. Expenses decrease your overall equity. Because an equity decrease requires a debit, all expenses are naturally increased via debit entries. Revenue, on the other hand, boosts your equity, meaning sales transactions are always recorded as credits. Some contemporary software designers argue we should abandon these traditional terms for simple positive and negative signs. Experts disagree on this point. While plus and minus signs work for rudimentary spreadsheets, they utterly collapse when handling complex corporate transactions like depreciation or stock buybacks.The Anatomy of a Transaction: Real-World Manifestations of Dual-Entry Logic

An Inventory Acquisition in Chicago

Let us look at a concrete corporate scenario to ground this theory. Imagine a manufacturing firm based in Chicago purchasing raw steel components on May 15, 2026. The total invoice comes out to exactly twelve thousand five hundred dollars, and the vendor, Midwest Industrial Supply, grants net-30 payment terms. How does the accountant log this? Two movements occur simultaneously. First, the company increases its inventory asset account, which demands a debit of twelve thousand five hundred dollars. Second, because they did not pay cash on the spot, they have created a brand-new liability. They credit their accounts payable account for the exact same amount. The ledger expands on both sides. The scale remains perfectly level.The Mid-Month Payroll Crunch

Then comes the cash settlement. When the Chicago firm finally cuts a check thirty days later, the entire process reverses itself. The accounts payable liability account is debited, shrinking it back down to zero. Simultaneously, the cash asset account is credited for twelve thousand five hundred dollars, reflecting the departure of funds from the corporate bank account. And what happens if a novice clerk accidentally debits cash instead? The system breaks instantly. The books would show an extra twenty-five thousand dollars of phantom value that simply does not exist in the physical world.Alternative Frameworks: Single-Entry Systems and the Boundaries of Modern Accounting

When the Ledger Fails to Justify Double Entries

Is double-entry bookkeeping always mandatory? No, we are far from it in the world of micro-businesses and solopreneurs. A single-entry system functions much like a standard checkbook register, tracking only cash inflows and outflows as singular events. If an independent graphic designer in Austin, Texas buys a new laptop for one thousand two hundred dollars, they write down the expense, reduce their cash balance, and stop there. No balancing act. No matching credit to an equipment asset account. As a result: their books are simple, cheap, and fast. The issue remains that this method offers zero insight into long-term financial health, completely hiding things like unpaid debts or depreciating machinery from potential investors.The Modern ERP Transition

Which explains why any enterprise eyeing serious growth must eventually migrate to double-entry protocols managed by Enterprise Resource Planning software. These modern systems disguise the underlying mechanism through clean user interfaces. When a retail clerk scans a barcode at a grocery checkout, they see a green checkmark on a screen, yet behind that glossy interface, the software is furiously executing a pre-programmed script: debiting cash, crediting sales revenue, debiting cost of goods sold, and crediting inventory. Every digital ghost of a transaction still obeys the ancient rules laid down in Venice.Common Mistakes and Misconceptions When Balancing the Ledge

The Illusion of Personal Banking Language

You open your smartphone app, look at your checking account, and spy a fresh credit. You rejoice. Yet, in corporate ledger design, that exact event signals a radically different phenomenon. The problem is that everyday consumers conflate corporate bookkeeping mechanics with retail banking notifications. When a financial institution credits your personal checking option, they are merely acknowledging an increase in their own internal liability to you. For a standard enterprise, however, tracking debits and credits requires abandoning these comforting consumer biases completely. A debit is not automatically an addition to wealth, nor is a credit an inherent subtraction. They are positional indicators, left versus right, nothing more.

The Danger of One-Sided Adjustment Attempts

Amateur bookkeepers often stumble when attempting to fix an erroneous transaction by simply altering a single entry. Let's be clear: a solitary adjustment destroys the entire equilibrium of your double-entry accounting matrix. If an accountant attempts to lower cash without simultaneously executing a corresponding change elsewhere, the trial balance shatters instantly. Every single monetary movement demands a dual-sided reflection. Because of this rigid symmetry, attempting to force a single-legged correction will leave your balance sheet lopsided. This occurs most frequently during messy year-end inventory cleanups or hasty cash reconciliation adjustments.

Confusing Revenue Increases with Debit Actions

Why do so many entrepreneurs falsely assume that earning money requires a debit to revenue? It feels intuitive because cash is increasing, right? Except that while your bank account asset does indeed experience a debit, the revenue tracking category operates under completely opposite structural rules. Revenue expands via credits. When a software company closes a major licensing deal, the sales ledger expands on the right-hand column. Failing to grasp this distinction leads to completely chaotic income statements that fail even basic auditing procedures.

The Hidden Velocity of Contrariwise Accounts

Mastering the Dark Art of Contra-Asset Mechanisms

Let us peek behind the curtain at a concept that routinely completely paralyzes intermediate bookkeeping students: the contra-asset category. Most traditional assets naturally possess a debit configuration. However, allowance for doubtful accounts or accumulated depreciation operates in reverse, retaining a permanent credit balance to intentionally erode the primary asset's top-line valuation. Why do we employ such a convoluted structural detour? It preserves historical cost data while simultaneously delivering real-time asset impairment metrics to sharp-eyed investors. It is an elegant accounting trick, though admittedly, it feels like driving a car backwards through a crowded intersection.

Consider a manufacturing corporation purchasing a heavy industrial stamping press for $500,000. Instead of continuously slashing the value of the machinery directly whenever depreciation occurs, the business maintains the original machinery account intact. The offset goes directly into the accumulated depreciation bucket. As a result: observers can immediately deduce both the raw age of the infrastructure and its current net book value. Managing these specific double-entry bookkeeping transactions flawlessly separates basic data entry clerks from strategic financial controllers who can truly forecast corporate tax liabilities.

Frequently Asked Questions

Does the implementation of computerized ERP software render the manual study of accounting entry balance rules completely obsolete?

Absolutely not, because automated systems frequently misclassify complex corporate transactions when encountering non-standard operational workflows. Recent industry surveys indicate that approximately 37% of enterprise resource planning implementations suffer from initial ledger configuration flaws. When algorithms misinterpret an obscure international supply chain tariff, human intervention must diagnose the anomaly. The system might blindly execute automated calculations, yet the issue remains that an uneducated operator cannot identify where the errant balance sheet discrepancy originated. Relying entirely on automated software without understanding underlying ledger logic invites catastrophic reporting failures during independent corporate audits.

How do modern digital cryptocurrency holdings complicate traditional ledger system documentation?

Crypto assets inject significant volatility into standard corporate ledgers because they behave simultaneously like speculative investments and traditional cash equivalents. When an organization utilizes digital tokens to settle an invoice, the transaction triggers an immediate multi-layered entry requiring a debit to expenses, a credit to the digital asset repository, and an additional realization entry for capital gains or losses. If Bitcoin fluctuates by 15% within a single six-hour operating window, the fair market value adjustment demands constant, meticulous recalculation. This rapid asset mutation demonstrates why traditional accounting system debit credit mechanics must remain highly flexible to accommodate decentralized finance structures. Accountants must frequently establish specialized valuation allowances just to stabilize these wildly shifting balances before quarterly regulatory reporting deadlines arrive.

Can a growing business successfully manage its financial operations using single-entry tracking methods instead?

A startup can certainly attempt utilizing a simplified single-entry structure during its initial operational months, but this approach fails spectacularly once external financing or inventory management becomes necessary. Financial institutions routinely reject commercial loan applications from entities lacking formal double-entry verification records. Statistically, over 80% of venture capital firms make comprehensive, balanced ledgers a non-negotiable prerequisite for series A funding rounds. Without the dual verification inherent in balanced columns, fraud detection becomes virtually impossible because cash leakage can easily hide behind unmonitored operational columns. Transitioning to a professional framework early prevents costly retrospective forensic accounting cleanups when the enterprise eventually scales.

Rethinking the Ledger as a Competitive Edge

Stop viewing the dual-column system as an archaic bureaucratic chore invented by Renaissance monks. It is a highly sophisticated, real-time diagnostic engine for tracking corporate energy and capital velocity. Executives who treat financial ledger tracking methods as a mere compliance checkbox completely miss the operational intelligence embedded within their own numbers. Your ledger tells a vivid story about risk, operational friction, and capital efficiency. By mastering these structural rhythms, leadership transforms messy raw transaction data into precise strategic maneuvers. We must demand absolute precision from our financial records, or we risk navigating the turbulent modern economic landscape completely blind. Ultimately, the ledger is not just recording history; it is actively dictating your company's survival capacity.