The Double-Entry Big Bang: Where It Gets Tricky for Modern Thinkers

We need to go back to 1494 in Venice. A Franciscan friar named Luca Pacioli published a mathematical compendium, though he didn't actually invent double-entry bookkeeping. He merely codified what Venetian merchants had been doing to prevent ship captains from stealing their spice cargo. People don't think about this enough: accounting wasn't born out of a love for math, but out of absolute paranoia. Pacioli mandated that the ledger layout must present the debit on the left, which he called debeo (he owes), and the credit on the right, or credo (he trusts). The left-to-right reading order of Western languages automatically weaponized debit as the first operational step in any entry.

The Linguistic Trap That Scrambles Your Brain

Why does your bank statement show a credit when your paycheck hits? It confuses everyone. When the bank credits your account, they are speaking from their perspective, not yours. To the bank, your money is a liability—something they owe back to you—and increasing a liability requires a credit. Yet, when you look at your own corporate books, that exact same cash injection is a debit. Honestly, it’s unclear why banks refuse to clarify this to the public, except perhaps that confusing customers keeps them compliant.

The Left-Right Orthodoxy of the Ledger Page

The layout is non-negotiable. Because Western civilization reads from left to right, the debit side must be populated before the eye travels to the credit side. It is a spatial tyranny. But does spatial primacy mean chronological primacy? Not at all. They are born at the exact same millisecond, much like quantum entangled particles in a Swiss physics lab.

The Mechanical Supremacy of the Left-Side Entry

Let us look at how this plays out in a real corporate system, say at a software firm in Berlin in May 2026. When a company buys a new server for 15,000 Euros, the software technician inputs the asset increase first. That is the debit. But wait, how do we pay for it? The issue remains that you cannot magically increase assets without showing the source of the funding, which explains why the credit to cash follows immediately after. But here is where my opinion ruffles feathers: the obsession with writing debits first is a archaic relic of ink-and-quill bookkeeping that modern ERP software like SAP or Oracle could easily discard tomorrow, yet we cling to it like gospel. Why? Because the human brain craves a starting point, and the left side provides that psychological anchor.

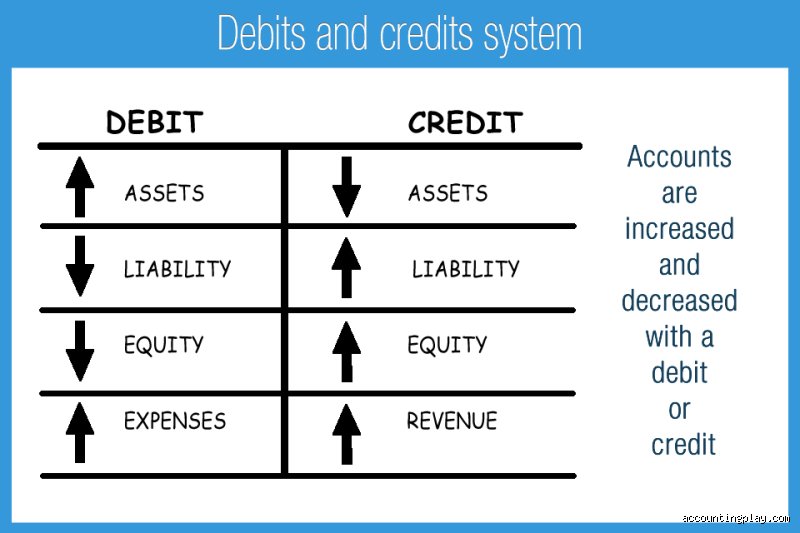

The T-Account Anatomy and Asset Realities

Think of a T-account as a scales-of-justice metaphor. If you inject 50,000 Dollars of seed capital into a startup in Austin, Texas, the cash account (an asset) rises on the left. The balancing act occurs on the right side of the equity account. Can you have a credit without a debit? Never. The algebraic reality of the accounting equation—Assets equals Liabilities plus Equity—demands a perfect, symmetrical dance where the left foot must move so the right foot can land.

The Chronological Paradox of the Journal Voucher

Every single transaction starts with a journal entry. Convention dictates that you list all debit lines completely before you indent and list the credit lines. If you dare to reverse this order on a university exam or in a corporate audit, the system will flag it as an error. As a result: we are forced to think of the destination of funds before we formally record the source, a mental inversion that drives non-accountants completely mad.

Why Debit Wins the Presentation Race in Corporate Reporting

If you open the balance sheet of Apple Inc., what do you see at the very top? Cash, short-term investments, and accounts receivable. These are all debit-balance accounts. The entire structure of financial reporting is biased toward showing what you own before showing who owns a piece of you. Yet, here is the nuance that contradicts conventional wisdom: while debits dominate the top of the balance sheet, credits completely rule the income statement because revenue is inherently a credit balance. That changes everything for growth-obsessed Wall Street analysts who only care about the top-line revenue, meaning they are actually worshiping credits while pretending to value assets.

The Secret Life of Normal Balances

Every account has a home state, known as its normal balance. For assets and expenses, that home is the debit side. For liabilities, equity, and revenue, it is the credit side. When a business experiences massive growth, both sides explode simultaneously. It is an expansion of the financial universe where the left and right sides push outward with equal force, meaning that prioritizing one over the other is like arguing whether the north or south pole of a magnet is more important to its magnetism.

Alternative Financial Systems and the Ghost of Single-Entry

What if we abandoned this binary system altogether? Micro-businesses often use single-entry bookkeeping, which is essentially a glorified checkbook register. In that world, the question of debit or credit vanishes entirely, replaced by a simple column of pluses and minuses. Except that single-entry systems are utterly useless for complex corporate entities because they fail to capture the dual nature of economic reality. When a company signs a lease for a warehouse in Tokyo, a single-entry system only sees the cash leaving the building months later, whereas double-entry captures the massive liability the exact second the pen hits the paper.

The Blockchain Disruption and Triple-Entry Mythos

Now, tech evangelists claim that Bitcoin and decentralized ledgers change everything by introducing triple-entry accounting, where a cryptographically secured receipt forms a third dimension. But look closer at the code. The underlying smart contracts still rely on inputs and outputs—a digital reincarnation of our old Venetian friends, debit and credit, masquerading as futuristic cryptography.