The True Weight of Death Duties: Understanding the Baseline Before the Exceptions

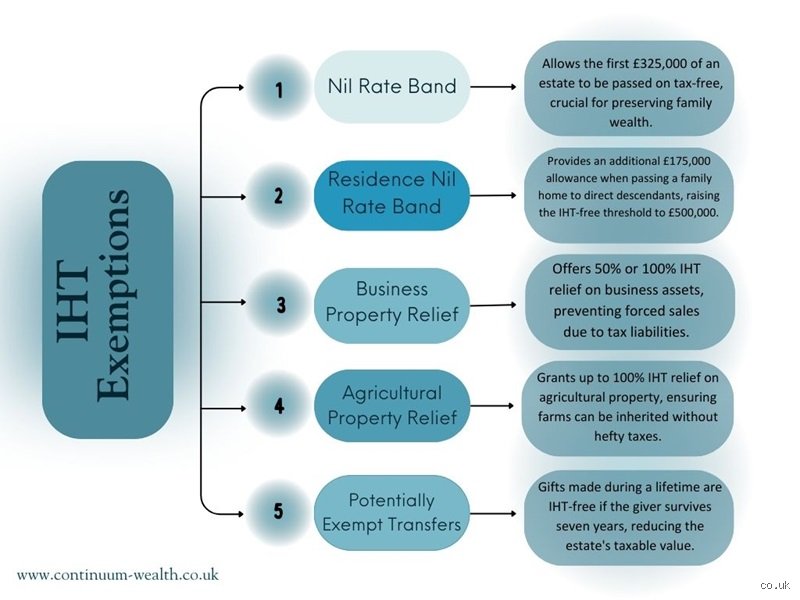

Before we can even talk about escaping the taxman, we need to look at what we are actually fighting against here. The standard Inheritance Tax rate sits at a staggering 40%, a figure that hasn't budged in decades, levied on everything you own above the standard nil-rate band. Currently, that baseline allowance is frozen at £325,000. It has been stuck at that exact number since the 2009/10 tax year, which, honestly, is a fiscal joke when you look at how property values have skyrocketed over the last fifteen years. Because the government refused to index this boundary to inflation, a tax that was once designed solely for the ultra-wealthy now routinely cannibalises the estates of ordinary, middle-class homeowners who bought modest terrace houses in London or Bristol back in the nineties.

The Residence Nil-Rate Band Twist

Then came the government's attempt to fix their own mess in April 2017 with the introduction of the residence nil-rate band. This adds an extra £175,000 allowance to your pool, theoretically bringing a single person's total tax-free threshold to a much-quoted £500,000. But people don't think about this enough: it only applies if you pass your main home directly down to "direct descendants" like children, grandchildren, or even foster kids. If you don't have children, or if you decide to leave your flat to your favourite niece or your lifelong best friend, that extra £175,000 vanishes instantly. Is that fair? I think it is an archaic, deeply discriminatory policy that penalises alternative family structures, yet it remains the law of the land.

The Ultimate Shield: How Marriage and Civil Partnerships Change Everything

If you want the most potent weapon against HMRC, you just need a wedding ring. The spousal exemption is absolute, meaning you can pass an estate worth £50 million to your husband, wife, or civil partner upon your death, and they will not pay a single penny of Inheritance Tax. Except that this magic trick only works if you are legally married. You could live with someone for forty-five years, share a mortgage, raise four children, and build a massive business together, but in the eyes of the law, you are still just cohabiting "strangers." The concept of a common-law spouse is a persistent, dangerous myth that ruins lives every day; when one partner dies intestate in that scenario, the survivor gets hit with a massive, unexpected tax bill that often forces them to sell the family home just to settle up.

The Inter-Spousal Transfer Post-Mortem

Where it gets tricky is what happens when the second partner eventually passes away. This is where the concept of transferable allowances saves the day, allowing a surviving spouse to inherit 100% of their late partner's unused nil-rate bands. Let us look at a concrete case: Arthur died in Manchester back in November 2021, leaving everything to his wife, Beatrice. Because his transfer to Beatrice was fully exempt, his £325,000 standard allowance and his £175,000 residence allowance remained completely untouched. When Beatrice eventually passes away, her executors can claim Arthur's unused allowances, effectively doubling her personal tax-free threshold to a whopping £1 million. That changes everything for the family finances, but the paperwork must be flawless.

The Non-Domiciled Trap

But we are far from a perfect system, especially if you or your spouse were born abroad. The spousal exemption is only unlimited if both partners are domiciled in the UK. If the deceased partner is UK-domiciled but the surviving spouse is non-domiciled, the tax-free spousal transfer is strictly capped at a lifetime limit of £325,000. It is a massive fiscal trap for international couples living in multicultural hubs like Birmingham or Edinburgh, often requiring the surviving partner to make a complex, formal election to be treated as UK-domiciled for tax purposes within two years of the death, a move that carries its own heavy, long-term global tax implications.

Altruism as a Strategy: The Power of Qualifying Charitable Donations

Another major group that answers the question of who is exempt from Inheritance Tax is registered charities. Any legacy you leave to a UK-registered charity, a national museum, an established university, or a registered political party is completely exempt from death duties. But there is a secondary, hidden benefit built into the tax code that many estate planners overlook. If you leave at least 10% of your net estate to a qualifying charity, the government rewards your generosity by slashing your overall Inheritance Tax rate on the remainder of your taxable estate from 40% down to 36%.

The Complex Mathematics of Giving

Let's run the numbers on this because the math is highly counterintuitive. Imagine Clara passes away in Leeds with a taxable estate of £100,000 above her allowances. Under normal circumstances, HMRC takes £40,000, leaving her family with £60,000. If Clara alters her will to leave exactly £10,000 to a local hospice, her taxable estate drops to £90,000, and her tax rate drops to 36%. The tax bill becomes £32,400. As a result: the charity gets £10,000, HMRC gets £32,400, and Clara's family walks away with £57,600. So, for the "cost" of just £2,400 out of her family's pocket, Clara directed £10,000 to a cause she actually cared about instead of letting it disappear into the government's general treasury pool.

The Potentially Exempt Transfer: The Seven-Year Gamble on Living Gifts

You don't have to wait until you die to move your money out of harm's way, but doing so early turns your life into a statistical countdown against the calendar. When you give a substantial sum of money or an asset to an individual during your lifetime, it is classified as a Potentially Exempt Transfer (PET). The issue remains that this gift is not immediately exempt; it only achieves total immunity if you manage to stay alive for at least seven years after the exact date the transfer took place. If you get knocked down by a bus in year six, the gift is dragged back into your estate for tax calculations.

Taper Relief and the Illusion of Safety

People often misunderstand how taper relief works during that tense seven-year window. They think the value of the gift magically reduces over time, which explains why so many families get caught out by unexpected tax demands. The reality is that the gift's valuation remains completely fixed; it is only the tax rate applied to the gift that decreases, and even then, it only starts dropping after year three. If you die within the first three years, the rate is the full 40%. In years three to four, it drops to 32%. Years four to five see it hit 24%, then 16% in years five to six, and finally 8% if you die between six and seven years after the gift. Hence, the protection is heavily back-loaded, making early lifetime gifting a strategy best suited for the relatively young and healthy, rather than a last-minute panic move on a deathbed.

Common Misconceptions That Cost Beneficiaries Millions

Thinking you are safe from the taxman is a dangerous game. Many people assume that Inheritance Tax exemptions apply automatically across the board without any paperwork. They do not. The Inland Revenue does not just take your word for it when a loved one passes away. Every single penny must be accounted for, which explains why so many families end up facing unexpected bills during probate.

The Myth of the Cohabiting Partner

Let's be clear: unless you have walked down the aisle or registered a civil partnership, the law views you as legal strangers. You might have shared a bed, a mortgage, and three children for over thirty-five years, yet you enjoy zero automatic spousal relief. If your partner dies without a will leaving everything to you, the estate faces a standard 40% levy on everything over the baseline £325,000 threshold. It sounds harsh because it is. Wealthy cohabitees often assume common-law marriage protects them, except that common-law marriage has not legally existed in this jurisdiction for centuries.

The Seven-Year Gifting Illusion

Gifting money solves everything, right? Wrong. The problem is that people misunderstand the taper relief rules completely. If you gift £500,000 to your daughter and pass away three years later, that money is still dragged back into your estate calculation. The tax rate does not actually drop for the recipient until year four, and even then, it only reduces the tax due on the gift itself, not the overall estate threshold. People confidently write cheques thinking they have outsmarted the system, but HMRC keeps a long, meticulous memory.

The Business Relief Loophole: An Expert Strategy

Most taxpayers focus entirely on residential property, entirely overlooking the massive potential of Business Property Relief. This is where truly sophisticated estate planning happens. If you own shares in an unlisted trading company, or even certain Alternative Investment Market shares, these assets can qualify for 100% inheritance tax exemptions after just two years of ownership. It is a legal, highly effective shelter.

Unlisted Shares as a Shield

Imagine possessing a portfolio worth £2,000,000. Left in cash or standard FTSE 100 stocks, your heirs would face an absolute bloodbath of taxation upon your demise. By restructuring those assets into qualifying trading businesses, you effectively wipe out that future liability. (Naturally, this assumes you can stomach the higher investment volatility inherent to smaller companies). It is a strategy utilized by the wealthy to bypass standard limits entirely, transforming what would be taxable wealth into completely exempt business property.

Frequently Asked Questions

Does the Nil-Rate Band automatically double for surviving spouses?

It does not happen automatically, as the surviving executor must actively claim the Transferable Nil-Rate Band during the probate process. When the first spouse dies and leaves their entire estate to the survivor, their personal £325,000 allowance goes unused. As a result: the surviving spouse can combine both allowances, creating a robust £650,000 shield against death duties. If you add the potential £175,000 residence nil-rate band from each partner, a total of £1,000,000 can eventually pass down to direct descendants completely tax-free. Failing to submit the specific form IHT400 within twenty-four months of the second death will forfeit this massive benefit entirely.

Can giving money to charity completely wipe out my tax bill?

Leaving your entire estate to a registered charity will indeed ensure that no tax is paid, because charitable donations are fully exempt. However, if you leave at least 10% of your net estate to a baseline eligible charity, a different rule kicks in. The government rewards this philanthropy by slashing the remaining tax rate on your taxable assets from 40% down to 36%. For a net estate valued at £1,500,000, this subtle four-percent reduction can save your family tens of thousands of pounds. It represents an excellent way to support a cause you love while simultaneously reducing the state's take.

Are pension pots subject to standard estate levies?

Pensions are generally kept entirely outside of your legal estate for tax calculations, making them one of the ultimate wealth transfer vehicles available today. If you die before reaching the age of seventy-five, your beneficiaries can inherit your remaining defined contribution pension pot totally free from any levy on inherited wealth. Should you pass away after seventy-five, the recipients will only pay income tax at their personal marginal rate when they withdraw the funds. Why do people spend down their pensions while preserving their taxable cash savings? The issue remains that traditional financial advice has been inverted by modern legislation, meaning you should actually spend your cash first and leave your pension untouched.

A Final Word on Wealth Preservation

The entire system governing who is exempt from Inheritance Tax has become an over-engineered labyrinth designed to catch the unprepared. We must recognize that the state views your accumulated wealth as an untapped revenue stream. If you choose to sit back and do nothing, your family will pay the price for your inertia. Do not rely on outdated assumptions or assume the system will treat your heirs fairly. True tax mitigation requires aggressive, early implementation of statutory exemptions. Take control of your legacy now, because the government certainly will not do it for you.