Deconstructing the Potentially Exempt Transfer: Where Most Families Trip Up

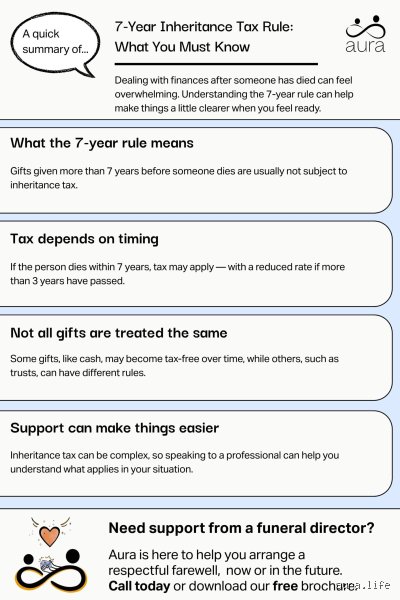

Let us strip away the jargon. When you hand over a lump sum to your children, the HMRC does not instantly cash a check. Instead, they label this a Potentially Exempt Transfer, or PET. This is where it gets tricky because a PET is effectively a tax ghost; it sits invisibly in your financial history, waiting to see if you will draw breath for another 84 months. People don't think about this enough, assuming that once the money leaves their account, the liability vanishes. We are far from it.

The Legal Anatomy of a Lifetime Gift

What constitutes a gift under these rules? It is not just writing a check for a wedding or handing over the keys to a property. The Revenue defines it as any transfer of value where your estate decreases and someone else's increases. If you sell your house to your daughter for £150,000 when the open market value is £400,000, you have not just made a savvy family deal. You have made a £250,000 gift. And the clock starts ticking the exact day the deed transfers, not when you first discussed it over Sunday roast. I have seen families caught out because they bungled the paperwork, delaying the official transfer date by months and resetting their seven-year countdown entirely by accident.

Why the Nil-Rate Band Changes Everything

Every individual gets a £325,000 tax-free allowance, known formally as the nil-rate band, which has been frozen since 2009. But here is the sting in the tail that conventional wisdom misses: lifetime gifts eat into this threshold first. If you give away £300,000 today and pass away four years later, that gift devours almost your entire allowance. This means your remaining assets—your actual home, your savings, your physical possessions—get hit with the full 40% tax rate from the very first pound. The issue remains that people look at the taper graph and assume their house is safe, completely oblivious to how gifts cannibalize the baseline exemptions from the bottom up.

The Taper Relief Myth: Why Surviving Four Years Might Not Save You a Penny

Ask the average person on the street how taper relief works, and they will tell you that the tax drops every year you stay alive. It sounds beautifully linear. Except that it is completely wrong. Taper relief does not reduce the value of the gift itself; it only reduces the tax rate charged on the gift if its value exceeds the £325,000 nil-rate band. If your total lifetime gifts sum up to less than this threshold, taper relief is completely useless to you. That changes everything for the middle-class estate.

The Sliding Scale of the Seven-Year Countdown

When an estate does breach that magic boundary, the tax rate on the excess slides down. For the first three years, the rate stays at a brutal 40%. Hit year four, and it drops to 32%. By year five, it is 24%. Year six brings it to 16%, and the final stretch in year seven sits at 8% before hitting zero. But because experts disagree on the psychological impact of this timeline, families often fail to buy appropriate insurance to cover the tapering liability. Why gamble with the taxman when a simple decreasing term policy could fix the exposure? Honestly, it's unclear why more advisers don't scream this from the rooftops.

The Disastrous Mathematics of an Early Demise

Let us look at a concrete example to ground this madness. Imagine Arthur, a retired architect in Bristol, who gifted his son £500,000 in cash on May 14, 2021, to buy a townhouse. Arthur tragically passes away on September 3, 2025, having survived four years and some change. Because the gift exceeded his £325,000 allowance by £175,000, that excess is subject to tax. Thanks to taper relief for a year four death, the tax rate drops from 40% to 32%. The resulting bill is a staggering £56,000, which the son must pay out of pocket within six months of Arthur's passing. If Arthur had lived until June 2028, that bill would be zero. A mere matter of months cost them a fortune.

The Seven-Year Clock vs. The Gift with Reservation Trap

You cannot have your cake and eat it too, though thousands try every single year. The Revenue is hyper-aware of the old trick where parents "gift" their home to their children but continue living in the master bedroom without paying a dime. This triggers the Gift with Reservation of Benefit rules. This completely breaks the 7 year rule on inheritance.

The Illusion of the Free House

If you retain any benefit from an asset after gifting it, the seven-year clock never actually starts ticking. It is a financial purgatory. You could survive twenty years after signing over the deeds, but if you still host your weekly bridge club there or use it as a holiday home without paying market rent, HMRC treats the property as if it never left your hands. Which explains why so many DIY estate plans collapse under audit. The state views this as a blatant tax avoidance scheme, and they will unwind it with terrifying efficiency, calculating the value at your eventual date of death rather than the historical transfer date.

The Annual Exemptions That Bypasses the Clock Entirely

Yet, we must nuance this bleak landscape; not every penny you hand over is subject to this agonizing countdown. The law provides small escape hatches that bypass the seven-year rule completely, though they are arguably far too small in the current economic climate. You can give away £3,000 total each tax year using your annual exemption. You can also carry forward any unused allowance from the previous year, meaning a married couple could theoretically clear £12,000 from their estate in a single afternoon without triggering a PET. There is also the small gifts allowance of £250 per person, wedding gifts up to £5,000 for children, and regular gifts out of normal surplus income, provided it doesn't impact your standard of living. In short: use these small allowances aggressively, because they are the only true instant passes out of the inheritance tax trap.