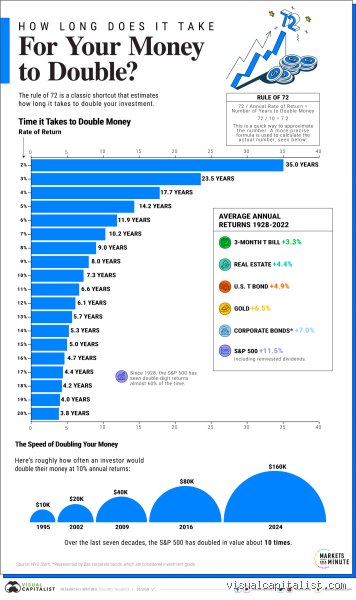

The Deceptive Simplicity of the Compounding Engine

We need to talk about why compound interest feels like magic to some and a trap to others. Most folks look at a 7% compound annual growth rate (CAGR) and think linearly, multiplying seven by ten and wondering where the extra two percent went. That is the thing is: geometric growth sneaks up on you. In the first year, your ten grand yields seven hundred bucks, but by year eight, you are earning interest on interest previously accumulated, which changes everything about the velocity of your capital.

The Mental Math Trap of Linear Thinking

People don't think about this enough, but our brains are wired for hunting and gathering, not exponential curves. If you track a stock portfolio across a decade, the early stages feel agonizingly slow. I once watched an investor friend in Chicago pull his money out of a boring index fund in 2016 because it "wasn't moving fast enough"—except that he missed the massive compounding bend that kicked in just three years later. Linear progression says two plus two equals four. Compounding means your money behaves like a snowball rolling down an infinite hill, where the mass of the ball itself accelerates the gathering of new snow.

Albert Einstein and the Ultimate Back-of-the-Envelope Trick

We have all heard the apocryphal quote attributed to Einstein calling compounding the eighth wonder of the world. Whether he actually said it remains highly debatable—honestly, it's unclear if the physicist ever cared about retail banking—yet the underlying formula remains undefeated. When you divide 72 by your expected rate of return, the resulting quotient gives you a remarkably accurate estimate of your investment's duplication timeline. Try it right now. Divide 72 by seven. You get 10.28, which sits so close to the logarithmic reality that arguing over the decimal points feels entirely pedantic.

The Logarithmic Truth Behind the Rule of 72

Where it gets tricky is when you move past the rule of thumb and look at the actual calculus. The mathematically precise formula relies on the natural logarithm, written out as LN(2) divided by LN(1 + r), where r represents your rate of return. When you run this equation using a strict 0.07 interest rate, the output shifts slightly. Is the Rule of 72 a flawless tool? Not quite, because it tends to lose accuracy as interest rates climb into the double digits, yet for the historical sweet spot of the modern stock market, it works beautifully.

Why the Number 72 and Not 69?

If we want to be pure math purists, the actual numerator for continuous compounding should be 69.3. But good luck dividing 69.3 by seven in your head while sitting at a coffee shop in Seattle trying to analyze your retirement portfolio. The financial community settled on 72 centuries ago—back when Renaissance merchants in Venice were tracking maritime trade loans—purely because it possesses an abundance of small divisors like two, three, four, six, and eight. It is a triumph of mental convenience over hyper-precision, hence its survival into the era of supercomputers.

The Real-World Variance Across Asset Classes

But let us look at how this applies to a real asset rather than a textbook example. A 7% return looks very different if you are holding a municipal bond versus a real estate trust in Ohio or a diversified basket of blue-chip equities. A bond might pay you out in regular cash increments, which means if you do not actively reinvest those dividends, your timeline to double your capital completely falls apart. You would be left with simple interest, and suddenly your ten-year horizon stretches out to over fourteen long years, which explains why automated dividend reinvestment plans are so critical.

Dissecting the 7% Return Threshold in Modern Investing

Why do we constantly obsess over a 7% benchmark anyway? Because when you strip away inflation from the historical performance of the S&P 500 over the last fifty years, that 7% figure is roughly what remains as the real rate of return for American equities. It represents the holy grail of passive wealth accumulation. Yet, the issue remains that historical averages are smooth, while your actual year-to-year experience in the market is incredibly jagged.

The Sequence of Returns Risk You Can't Ignore

Imagine two investors, Sarah and Marcus, who both start with $50,000 in 2026. Sarah experiences three years of consecutive 15% market gains followed by a sharp 10% correction, whereas Marcus suffers a brutal 20% drop in his first year followed by a massive recovery. Even if both portfolios average out to a 7% return over a decade, their actual cash balances at the ten-year mark will diverge wildly. The order in which your returns occur matters just as much as the average percentage itself, a structural reality that standard calculators completely ignore.

The Fee Erosion and the Silent Tax Bite

Here is my sharp opinion that contradicts the conventional wisdom found on standard financial blogs: aiming for a 7% return on paper is utterly useless if you are holding your assets in a taxable brokerage account with high expense ratios. Let us say your mutual fund charges a 1% management fee, and Uncle Sam takes another 15% in long-term capital gains distributions each year. Your net return isn't seven percent anymore; it has been chopped down to roughly 5.2%. As a result: your ten-year doubling timeline instantly balloons into nearly fourteen years of waiting.

How 7% Compares to the Rest of the Financial Universe

To truly understand how long to double money with 7% return, we have to look at the alternative realities available to your cash right now. We are far from the days of zero-interest bank accounts, but we are also not living in the hyper-inflationary eras of the past. The investment landscape is a spectrum of risk and patience.

High-Yield Savings Accounts vs. The Equity Markets

If you leave your money in a traditional brick-and-mortar bank account earning a miserable 0.05%, the Rule of 72 dictates that you will wait roughly 1,440 years to double your wealth. Even if you secure a high-yield savings account or a Certificate of Deposit paying 4%, you are still looking at an eighteen-year horizon. Moving your capital up the risk curve to chase that 7% target shaves nearly a decade off your waiting time, except that you must develop the stomach to watch your principal fluctuate during market downturns.

The Trap of Linear Thinking: Common Misconceptions

Our brains are fundamentally wired for addition, not multiplication. When you ask yourself how long to double money with 7% return, your intuition probably suggests a slow, steady crawl where each year looks identical to the last. Except that compounding works on a curve, not a straight line.

The Illusion of Simple Interest

The problem is that amateur investors often calculate gains based entirely on their initial principal. Let's be clear: if you invest $10,000, a 7% return doesn't just hand you $700 every single year until you cross the finish line. In the second year, you are earning interest on $10,700, which yields $749. Because that extra $49 seems minuscule, people dismiss it. Yet, this tiny snowballing effect is exactly what shaves decades off your wealth-building timeline.

Ignoring the Erosion of Purchasing Power

You hit your numerical target in roughly 10.3 years, but what can that money actually buy? Inflation is the silent tax that nobody factors into their spreadsheet calculations. If inflation hovers around 3%, your nominal 7% return shrinks to a real purchasing power growth of just 4%. As a result: your money takes nearly 18 years to double in terms of actual utility. Wealth is not a scoreboard of arbitrary numbers; it is about sustaining your standard of living.

The Sequence of Returns: The Expert Dimension

A steady, uninterrupted annual yield is a myth found only in textbooks. In the real world, achieving an average 7% performance means enduring a chaotic sequence of volatile market swings.

The Danger of Late-Stage Market Crashes

Does the order of your annual returns matter? If you are simply holding an asset for a decade without touching it, the mathematical answer is no. However, the issue remains critical if you plan to withdraw funds or if you alter your savings rate midway through the cycle. A massive 20% market dip in year two is easily remedied because your absolute dollar loss is minimal. But a crash in year nine? That devastating blow destroys a massive chunk of your accumulated interest right before the finish line, completely shattering your timeline for how long to double money with 7% return.

Frequently Asked Questions

Does the Rule of 72 work for a 7% return rate?

Yes, the mathematical shortcut remains incredibly accurate for this specific growth rate. By dividing 72 by your annual interest rate of 7, you get a projected timeline of 10.28 years. The actual logarithmic calculation places the figure at exactly 10.24 years, meaning the error margin of this mental trick is less than one percent. (Engineers might scoff at the rounded shorthand, but your wallet won't notice the difference). Investors can safely use this rule of thumb for quick napkin math across most single-digit market yields.

How does monthly compounding affect how long to double money with 7% return?

Frequent compounding accelerates your wealth accumulation by shifting the math from an annual schedule to a continuous loop. When a bank or fund calculates your 7% yield on a monthly basis, the effective annual rate actually bumps up to 7.23%. This structural adjustment trims the waiting period down from 10.24 years to roughly 9.93 years. Consequently, you shave nearly four months off your timeline simply by choosing an account that compounds more frequently. It proves that the vehicle you choose matters just as much as the nominal rate advertised on the glossy brochure.

Can taxes alter the time it takes to double your capital?

Taxes are the ultimate buzzkill for compound interest. If you hold your investments in a standard brokerage account, Uncle Sam will demand a cut of your dividends and realized capital gains every single year. A investor facing a 15% long-term capital gains tax effectively sees their 7% return drop to an annualized 5.95%. Which explains why your doubling timeline stretches from 10.24 years to over 12 years if you fail to shield your money. Utilizing tax-advantaged accounts like a Roth IRA or 401k is the only definitive way to keep your capital doubling velocity on its fastest trajectory.

The Reality of the 7% Threshold

Stop obsessing over the perfect mathematical symmetry of the number 72. Wealth accumulation is never a passive, sterile laboratory experiment; it is a gritty psychological battle against your own urge to panic-sell during market downturns. If you possess the emotional discipline to lock your money away for 3,740 days without tinkering with the portfolio, historical data shows the market will do the heavy lifting for you. We must realize that time, not brilliant stock picking, is the ultimate lever of financial freedom. Stop looking at the daily tickers. Trust the calculus, accept the volatile market dips as the price of admission, and let the compounding engine quietly do its job.

💡 Key Takeaways

- Is 6 a good height? - The average height of a human male is 5'10". So 6 foot is only slightly more than average by 2 inches. So 6 foot is above average, not tall.

- Is 172 cm good for a man? - Yes it is. Average height of male in India is 166.3 cm (i.e. 5 ft 5.5 inches) while for female it is 152.6 cm (i.e. 5 ft) approximately.

- How much height should a boy have to look attractive? - Well, fellas, worry no more, because a new study has revealed 5ft 8in is the ideal height for a man.

- Is 165 cm normal for a 15 year old? - The predicted height for a female, based on your parents heights, is 155 to 165cm. Most 15 year old girls are nearly done growing. I was too.

- Is 160 cm too tall for a 12 year old? - How Tall Should a 12 Year Old Be? We can only speak to national average heights here in North America, whereby, a 12 year old girl would be between 13

❓ Frequently Asked Questions

1. Is 6 a good height?

2. Is 172 cm good for a man?

3. How much height should a boy have to look attractive?

4. Is 165 cm normal for a 15 year old?

5. Is 160 cm too tall for a 12 year old?

6. How tall is a average 15 year old?

| Male Teens: 13 - 20 Years) | ||

|---|---|---|

| 14 Years | 112.0 lb. (50.8 kg) | 64.5" (163.8 cm) |

| 15 Years | 123.5 lb. (56.02 kg) | 67.0" (170.1 cm) |

| 16 Years | 134.0 lb. (60.78 kg) | 68.3" (173.4 cm) |

| 17 Years | 142.0 lb. (64.41 kg) | 69.0" (175.2 cm) |