The Hidden Reality of Early Retirement at Fifty

We have all seen the glossy magazine covers featuring smiling couples who threw in the towel at middle age to sip wine on a porch in Portugal. What those photos do not show you is the sheer anxiety of watching a portfolio fluctuate when you have four decades of unemployment stretching ahead of you. Dropping out of the corporate rat race at 50 means your money has to work twice as hard because it needs to last twice as long. Honestly, it's unclear why more financial planners do not lead with this warning.

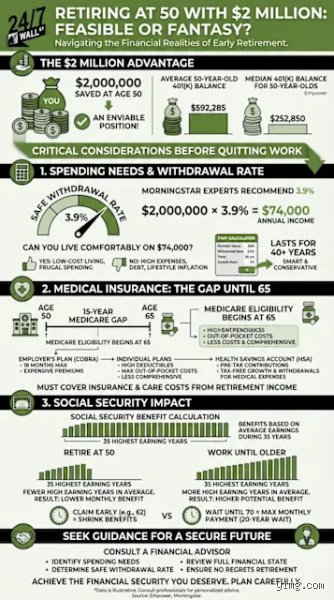

The Problem with the Conventional Four Percent Rule

William Bengen formulated the famous 4% rule back in 1994, but people don't think about this enough: his data assumed a traditional 30-year retirement window. If you pull the plug at 50, your horizon expands to 40 or even 50 years, which completely shatters the baseline math. Pulling $80,000 annually from a $2,000,000 portfolio might seem safe initially, yet a prolonged market downturn in your first five years of retirement—a phenomenon known as sequence of returns risk—can deplete your principal to a point of no return. The thing is, standard financial advice is built for 65-year-olds, and blindly applying it to an early exit is a recipe for disaster.

Why Modern Inflation is the Ultimate Portfolio Killer

Let us look at a concrete example. Imagine a real-world scenario involving a couple, Mark and Elena, who decided to retire in Austin, Texas, back in 2021 with exactly two million bucks. They assumed their static lifestyle costs would remain perfectly predictable, but then the post-pandemic macroeconomic shift triggered massive price hikes in everyday commodities. Because a dollar today buys significantly less than it did five years ago, their purchasing power eroded far faster than their conservative spreadsheets predicted. Inflation is not a flat 2% line item; it is a compounding beast that aggressively eats away at your fixed-income distributions.

Decoding the Math Behind a Two Million Dollar Nest Egg

To understand if you can retire at 50 with 2 million dollars, we have to strip away the emotional euphoria of leaving your boss behind and look strictly at the cold, hard numbers. Your asset allocation during this phase determines whether you thrive or end up applying for a retail job at 63. You cannot just park everything in a high-yield savings account or certificates of deposit because those vehicles rarely outpace the cost of living over multiple decades. On the flip side, going entirely into equities exposes you to heart-stopping market corrections that you no longer have a salary to buffer against.

The Sequence of Returns Hazard Explained

What happens if the S&P 500 drops 20% during your first twelve months of freedom? If you are forced to sell mutual fund shares at a steep discount to fund your daily espresso habit and mortgage, you are permanently locking in those losses. Where it gets tricky is that two investors with the exact same average annual return can experience wildly different outcomes based purely on the luck of their retirement start date. If the market booms in your early fifties, you are golden; if it crashes, you are cooked.

Tax Drag and the Pre-59.5 Penalty Trap

Another massive hurdle is the Internal Revenue Service. Most people accumulate their wealth inside traditional 401k plans or traditional IRAs, except that Uncle Sam slaps a 10% early withdrawal penalty on those accounts if you touch them before age 59.5. You must build a bridge strategy using taxable brokerage accounts or utilize sophisticated tax maneuvers like Substantially Equal Periodic Payments under IRS Section 72(t). And remember, unless your money is heavily concentrated in a Roth IRA, every single dollar you withdraw to buy groceries will be subject to ordinary income tax rates, reducing your actual net spending power.

The Outsized Impact of Healthcare Before Medicare

The single biggest line item that catches early retirees off guard is health insurance. When you leave your employer, you lose the corporate subsidy that makes premium payments bearable. Since Medicare does not kick in until you turn 65, you face a fifteen-year gap where you are entirely on your own in the open marketplace.

Navigating the Affordable Care Act Marketplace

To survive this period without draining your accounts, you have to become an expert at manipulating your Modified Adjusted Gross Income to qualify for federal subsidies. A family of two living in Ohio might easily see unsubsidized health insurance premiums skyrocket to $1,500 a month for a high-deductible silver plan. But if you can keep your taxable income low by strategically withdrawing from a mix of cash reserves and capital gains, those premiums drop significantly. As a result: managing your tax bracket becomes a full-time job in itself.

The Shock of Unexpected Long-Term Care Costs

We also need to discuss the late-stage reality that nobody wants to contemplate at age 50. According to historical industry data, more than half of individuals turning 65 will require some form of long-term care services. A private room in an assisted living facility can easily demand over $100,000 per year in today's dollars. If you do not have a dedicated insurance policy or an incredibly robust investment buffer to absorb that hit late in life, your two-million-dollar legacy will vanish into a healthcare provider's ledger within a few short years.

How Location and Lifestyle Redefine the Feasibility

Can I retire at 50 with 2 million dollars? The answer hinges heavily on geography. Two million dollars in San Francisco is a drop in the bucket; that same amount in the Midwest makes you local royalty.

The Power of Geographic Arbitrage

I am a strong proponent of moving your capital to where it is treated best. If you sell a highly appreciated home in a high-tax state like New Jersey and relocate to a tax-friendly jurisdiction like Tennessee or Florida, that changes everything. You instantly lower your property tax burden, eliminate state income tax on your investment dividends, and significantly drop your overall baseline cost of living. Some adventurous souls even choose international relocation to places like Costa Rica or Thailand, where high-quality medical care and luxury living cost a fraction of domestic prices.

Flexible Spending Versus Rigid Fixed Budgets

The ultimate secret weapon of the successful early retiree is structural flexibility. If your budget is packed with rigid, unyielding fixed costs like a massive luxury car lease and a jumbo mortgage, you are highly vulnerable to economic shocks. But if you can dynamically scale back your discretionary spending by 10% during a recession—perhaps by skipping an international vacation or delaying a home renovation—your portfolio's survival probability surges. In short, your willingness to adapt matters far more than any rigid mathematical formula ever will.

Navigating the Blind Spots of Early Retirement

You have hit the magic number. Two million dollars sits gleaming in your brokerage account, and the urge to hand in your resignation tomorrow is intoxicating. Let's be clear: achieving this milestone by age 50 is an exceptional feat that puts you far ahead of the average worker, but walking away from a paycheck for potentially four decades requires dismantling some dangerous financial myths first.

The Linear Return Mirage

Most spreadsheets assume a smooth, upward trajectory. They calculate a steady 7% annual gain and map out a flawless horizon. Except that markets do not cooperate with averages. If the stock market tanks 25% during your first thirty-six months of freedom, your portfolio faces a mathematical catastrophe known as sequence of returns risk. Aggressive early withdrawals during a market downturn permanently gut your principal, ensuring the money runs dry long before you do. Averages lie because volatility destroys compounding when you are actively draining the pot.

Underestimating the Healthcare Chasm

Medicare does not kick in until you turn 65. That leaves a fifteen-year gap where you are entirely on your own. Many early retirees assume they can just buy a basic plan on the health insurance marketplace and call it a day. The problem is that unsubsidized private health insurance for a 50-year-old couple can easily breach $1,500 monthly. Failing to budget for soaring medical premiums and out-of-pocket deductibles is the quickest way to turn a comfortable retirement into a stressful budgeting nightmare. A single chronic diagnosis can shatter your fragile assumptions instantly.

The Phantom Inflation Tax

We often think of our expenses as fixed numbers that stay frozen in time. But over a forty-year retirement, even a mild 3% inflation rate will cut the purchasing power of your money in half. Can I retire at 50 with 2 million dollars if everyday goods double in price? Your $80,000 annual lifestyle today will require $160,000 just to maintain the exact same standard of living down the road. Ignoring long-term purchasing power erosion means you are silently planning your own future poverty line.

The Hidden Leverage of the Variable Withdrawal Strategy

To survive a forty-year retirement without losing sleep, you must abandon the rigid, outdated rules of the past. The traditional 4% rule, which suggests pulling a fixed amount adjusted for inflation every year, was built for standard 30-year retirements starting at age 65. For a fifty-year-old, relying on a static withdrawal framework is financial suicide. The issue remains that rigidity breeds failure in dynamic economic environments.

Dynamic Spending Guardrails

The smartest retirees use a system of flexible guardrails. When the market thrives, you can safely enjoy the fruits of your capital. But when the market drops, you must immediately curtail your discretionary spending by 10% or 20%. By establishing a variable guardrail withdrawal framework, you dramatically lower the probability of depleting your capital. (It requires strict discipline to skip that luxury European vacation during a bear market, but it protects your core nest egg.) This adaptive mechanism allows a $2,000,000 portfolio to withstand prolonged economic stagnation without collapsing under the weight of constant, unyielding distributions.

Frequently Asked Questions

Can I retire at 50 with 2 million dollars if I still owe money on my mortgage?

Carrying a major housing debt into early retirement significantly increases your mandatory baseline expenses, which forces you to take larger portfolio withdrawals regardless of market conditions. If you have a remaining $300,000 balance on a 4% mortgage, your fixed monthly obligations eat up a massive portion of your safe withdrawal amount. Statistics show that housing typically comprises 33% of an average retiree's annual budget, making debt elimination the ultimate safety net. Eliminating all structural debt obligations before cutting ties with your employer provides immense psychological relief and creates a lean, highly resilient budget that easily survives market downturns. As a result: your portfolio experiences far less pressure during economic contractions because your absolute survival threshold is incredibly low.

How does the 72(t) IRS rule help fifty-year-old retirees avoid penalties?

Most people believe their retirement accounts are completely locked away until age 59.5 unless they want to pay a hefty 10% early withdrawal penalty to the government. Yet, the IRS provides a specialized loophole through Internal Revenue Code Section 72(t) that allows you to bypass this penalty entirely. By establishing a schedule of Substantially Equal Periodic Payments based on your life expectancy, you can legally access your traditional IRA funds early. You must commit to these withdrawals for at least five full years or until you hit age 59.5, whichever period is longer. Utilizing IRS Section 72(t) distributions bridges the liquidity gap perfectly, allowing your millions to fund your life today without enriching the tax collector.

What asset allocation is best for a multi-decade early retirement?

An early retiree cannot afford to be overly conservative because a 50-year-old needs their money to grow for another forty years to beat inflation. Holding 80% of your net worth in cash or low-yielding bonds will guarantee that your purchasing power is utterly annihilated by rising costs over time. Conversely, dumping 100% of your wealth into volatile equities exposes you to devastating sequence risk right when you stop working. An optimal balance typically hovers around 60% equities for long-term growth and 40% fixed income or cash equivalents to fund five to seven years of living expenses during market corrections. Balancing equity growth with short-term liquidity ensures you never have to liquidate your stocks at the absolute bottom of a market cycle.

The Verdict on Retiring Early with Two Million

Pulling the trigger on retirement at age 50 with a two-million-dollar nest egg is entirely achievable, but it is a razor-thin operation that leaves zero room for careless optimism. You are trading the security of a peak-earning paycheck for the unpredictable winds of global markets, meaning your luxury consumption must remain entirely flexible. Is it worth sacrificing your current corporate status for the ultimate freedom of time? Absolutely, provided you view your wealth as a tool for security rather than an endless personal ATM. Which explains why the final verdict hinges not on market performance, but on your personal willingness to live dynamically and adjust your spending when reality defies your spreadsheet. In short: you can certainly retire today, but only if you have the courage to manage your capital like an unyielding corporate CFO.