Decoding the Arcadium Anatomy and Why the Mining Giant Bit

To understand the sheer scale of what happened, we need to look at what Arcadium Lithium actually was before it got swallowed up by Rio Tinto. The company was not some speculative junior miner with a few exploratory boreholes and a glossy slide deck; it was a newly minted titan. Formed just a year earlier in January 2024 through a mega-merger between American chemical specialist Livent and Australian mining force Allkem, Arcadium boasted operational deep roots. People don't think about this enough, but this corporate marriage brought together legacy assets dating all the way back to the mid-twentieth century under a single banner.

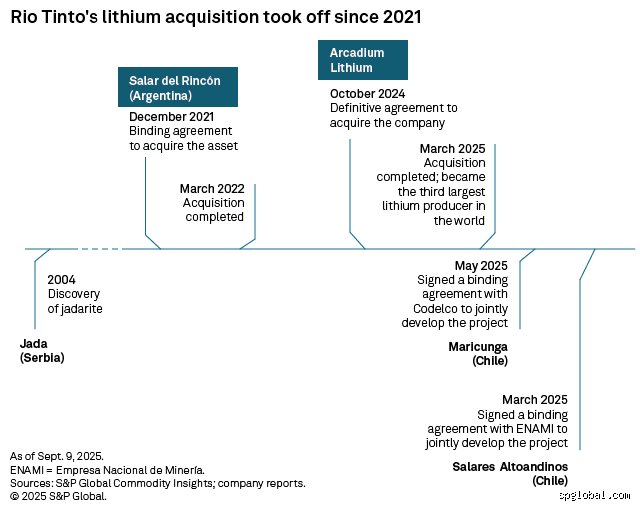

Rio Tinto had been itching to get into the white-gold rush for years, especially after their Jadar project in Serbia encountered fierce political roadblocks and environmental protests. They needed immediate, tier-one production capacity. Arcadium provided exactly that on a silver platter. By paying $5.85 per share in cash, Rio Tinto bypassed the grueling, decade-long process of building a mining project from scratch, absorbing operational nodes across Argentina, Australia, Canada, and the United States. Honestly, it's unclear if any other entity had the financial muscle to pull off such an aggressive consolidation during a market downturn, but Rio Tinto proved it did.

The Architecture of a Global Pure-Play Subsidiary

Following the finalization of the transaction, the Arcadium corporate entity was dissolved from the New York Stock Exchange and the Australian Securities Exchange. It was promptly integrated into a newly created operating division rebranded simply as Rio Tinto Lithium. This structural metamorphosis means that the mining giant now controls an integrated pipeline that goes straight from brine pumping and hard-rock blasting to high-purity chemical manufacturing. Where it gets tricky is the integration of these highly diverse chemical processing plants with a traditional, bulk-commodity mining culture. I believe this cultural and operational synthesis is where the real battle will be won or lost, because managing specialty chemical refining is miles away from shipping millions of tons of raw iron ore out of Western Australia.

The Geopolitical Chessboard and South American Brine Dominance

The crown jewels of the acquisition are undeniably located within the Lithium Triangle of South America, specifically the high-altitude salt flats of Argentina. Through Arcadium, Rio Tinto took absolute control over the massive Salar de Olaroz project in Jujuy and the historic Fénix operations in Catamarca. This moves the needle significantly. The thing is, by marrying these running operations with its own pre-existing Rincon lithium project in Salta, Rio Tinto has transformed overnight into the undisputed king of Argentine lithium extraction. But can they smoothly scale up production across three separate, ecologically sensitive salt flats without triggering local regulatory pushback?

To keep the momentum going, Rio Tinto immediately applied to enter Argentina’s RIGI framework—a specialized incentive regime for large investments—proposing an additional injection of $2.5 billion specifically earmarked for expanding the Rincon plant. This massive capital deployment aims to drive total corporate production capacity toward a staggering 200,000 tonnes per year of lithium carbonate equivalent by 2028. Yet, the local communities and regional water tables remain a highly delicate variable that corporate balance sheets often underestimate.

The Push for Direct Lithium Extraction

The technical salvation for these brine operations heavily relies on the deployment of Direct Lithium Extraction tech. Unlike traditional evaporation ponds that sit under the sun for up to two years, this method pumps brine through a processing unit that chemically extracts the ions before reinjecting the depleted liquid back underground. It sounds like an environmental silver bullet, right? Except that traditionalists in the mining sector remain deeply skeptical about its energy consumption and commercial scalability at a massive volume. Rio Tinto is betting big that their engineering prowess can optimize this process, having already initiated small-scale production at their Rincon starter plant late last year.

Hard Rock Assets and Northern Hemisphere Footholds

Beyond the sprawling salt flats, the acquisition handed Rio Tinto vital hard-rock spodumene assets like the Mt Cattlin mine in Western Australia and advanced development projects in Canada, notably the James Bay deposit. This geographic diversification is incredibly strategic. Because automakers in Detroit and Berlin are desperate to comply with strict domestic sourcing laws, having assets located safely inside North American and Australian jurisdictions that qualify for subsidies is a major win. That changes everything for Western supply chains trying to decouple from East Asian refining dominance.

The Countercyclical Gambit: Buying the Bottom of a Collapsed Market

The timing of this transaction was a masterclass in corporate predatory behavior. Spot prices for battery-grade lithium carbonate had famously collapsed by more than 80 percent from their speculative peak of over $80,000 per tonne down to a bruising $10,159 per tonne. This savage pricing downturn devastated the valuations of pure-play producers, cutting Arcadium’s equity value roughly in half over a twelve-month period. Most boards would freeze in terror during such a rout. Rio Tinto’s executive team, however, saw a golden window to strike while their target was bleeding.

The issue remains that commodity cycles are brutally volatile, and critics argue that Rio Tinto may have moved too early if prices stagnate for longer than anticipated. Yet, long-term macroeconomic data strongly supports the move, with global demand projected to expand by more than 10 percent annually through 2040. When you look at the fundamental realities of electric vehicle adoption and grid-scale storage, a structural supply deficit looks practically inevitable. By using its massive iron ore cash flows to fund this deal via a bridge loan, Rio Tinto pulled off a maneuver that its less-diversified competitors could only watch with envy.

The Fine Print of Regulatory Clearances

An international acquisition of this magnitude doesn't just happen overnight without a mountain of regulatory scrutiny. A global antitrust team had to steer the transaction through complex merger control reviews across several major jurisdictions, including the United States, China, Japan, South Korea, and the United Kingdom. Because the clean energy transition has become deeply politicized, any cross-border consolidation of critical minerals invites intense government inspection. Fortunately for Rio Tinto, since they had virtually zero operational lithium assets prior to the purchase, the competitive overlaps were minimal, which explains why the regulatory green lights were secured with relatively little friction by the first quarter of 2025.

How the Deal Alters the Global Peer Landscape

This transaction completely alters the competitive hierarchy of the Western mining world. Historically, diversified giants like BHP and Glencore have been highly hesitant to dive headfirst into lithium, preferring to focus their energy transition bets heavily on copper and nickel. Rio Tinto has broken ranks completely, positioning itself far ahead of its traditional peers in the battery chemical race. We are far from the days when lithium was considered a niche, minor commodity traded in small volumes; it is now a foundational pillar of heavy industrial strategy.

Juxtaposing Rio Tinto Against the incumbents

Before this transaction, the global lithium landscape was firmly ruled by dedicated specialists like Albemarle, SQM, and aggressive Chinese conglomerates who rapidly locked up global processing capacity. By inserting a multinational miner with a market cap exceeding one hundred billion dollars into the mix, the playground rules shift. Rio Tinto can easily absorb losses during weak pricing cycles that would bankrupt smaller producers, allowing them to consistently invest in asset expansions while others are forced into care and maintenance. As a result: the consolidation of the lithium sector is bound to accelerate, forcing remaining mid-tier miners to either scale up rapidly through their own mergers or prepare to be acquired by the remaining cash-rich mining elite.

Common mistakes and misconceptions about the transaction

Confusing the asset type with traditional brine

Many spectators assume Rio Tinto acquired a standard, evaporation-pond operation. Except that Arcadium Lithium’s portfolio is a complex, multi-geography beast spanning hard-rock mining in Australia and premium conventional brines in Argentina. The problem is that retail investors often lump all South American lithium into a single, slow-drying bucket. Arcadium utilizes proprietary direct lithium extraction techniques alongside traditional methods, which dramatically alters the production timeline and scaling velocity.

The illusion of an overnight supply surge

Did you really think this multi-billion-dollar swoop would instantly fix the global supply crunch? Think again. Merging two massive corporate structures takes time, and translating raw acreage into battery-grade hydroxide is an entirely different battle. Rio Tinto purchased long-term capacity, not an immediate valve to flood the market. It will take years to fully integrate the engineering cultures. Why do people always expect instant gratification from a industry that measures progress in decades?

Overestimating the impact of current spot prices

Pundits screamed that the mining giant overpaid because the commodity price was languishing in a brutal cyclical trough. But let's be clear: Rio Tinto is playing a generational game, completely ignoring the short-term noise that panics day traders. They acquired Arcadium Lithium precisely because the market was depressed, securing a massive discount relative to peak valuation cycles. The issue remains that casual observers evaluate mining megadeals through the microscopic lens of this week's spot price rather than a thirty-year macroeconomic horizon.

The overlooked extraction paradox and expert guidance

The hidden chemistry bottleneck that nobody discusses

Everyone talks about tonnage, yet the real bottleneck is the strict chemical purity required by cathode manufacturers. Arcadium's true value lies not just in its massive sub-surface reserves, but in its specialized processing facilities. Battery-grade lithium carbonate requires 99.5 percent purity, a threshold that sounds simple until you attempt to achieve it at a scale of tens of thousands of metric tons per year. If you are tracking what lithium company did Rio Tinto buy to assess the future of EV supply chains, you must focus on the chemical refining capacity rather than just the raw extraction volume.

Strategic advice for navigating the new mining landscape

Our recommendation for analyzing this consolidated market is straightforward: watch the capital expenditure allocations very closely. Rio Tinto possesses the deep pockets that Arcadium desperately lacked to execute its aggressive expansion pipeline. As a result: we expect a rapid acceleration of the Sal de Vida and Hombre Muerto expansions in Argentina. We admittedly cannot predict exact geopolitical shifts in South American mining jurisdictions, but watching the cash flow will reveal the true velocity of this consolidation. Keep your eyes on the engineering contracts, not the press releases.

Frequently Asked Questions

What lithium company did Rio Tinto buy and what was the total transaction value?

Rio Tinto officially acquired Arcadium Lithium in an all-cash transaction valued at 6.7 billion American dollars, paying a substantial premium of ninety percent over the company's undisturbed closing price. This massive consolidation brought together Rio's global mining infrastructure with Arcadium’s specialized extraction footprint across multiple continents. The deal instantly positioned the combined entity as one of the top three global producers of the critical battery metal. Which explains why the market reacted with such volatility during the announcement phase, as the acquisition fundamentally alters the competitive dynamics of the energy transition ecosystem.

How does this acquisition change Rio Tinto's global production ranking?

Prior to finalizing this specific acquisition, the Anglo-Australian mining behemoth lacked significant, active commercial production of battery-grade materials despite holding massive un-mined assets like the Jadar project. By absorbing Arcadium's existing facilities, Rio Tinto instantly captures roughly eleven percent of global chemical supply capacity. This leapfrogs them past dozens of junior exploration outfits directly into the dominant upper echelon of global producers alongside giants like Albemarle and SQM. In short, the company bought its way out of a multi-year development delay by acquiring immediate, operational market share.

Which specific geographical assets were included in the Arcadium purchase?

The acquisition delivers a highly diversified geographical footprint including the massive James Bay hard-rock project in Canada and active brine operations in Argentina's lithium triangle. Furthermore, the transaction includes the Mt Cattlin spodumene mine located in Western Australia, which provides immediate feedstock flexibility. These assets collectively represent a projected production capacity exceeding 170,000 metric tons of lithium carbonate equivalent annually by the turn of the decade. (This diversified footprint effectively mitigates the localized political risks that often plague concentrated mining operations.)

A definitive look at the mining paradigm shift

The era of the independent lithium pure-play company is rapidly drawing to a close. Rio Tinto’s aggressive acquisition of Arcadium Lithium signals that the world's most powerful diversified miners are no longer content to sit on the sidelines of the green transition. This move was never about chasing a temporary market trend; it was a cold, calculated consolidation of critical chemical infrastructure. We believe this transaction will trigger a domino effect across the entire sector, forcing rival mining conglomerates to aggressively gobble up the remaining independent extractors before they are left behind. The future belongs to massive, vertically integrated giants with the financial muscle to weather cyclical storms. Ultimately, you are either a predator or a target in this new era of resource nationalism, and Rio Tinto just staked its claim as the undisputed apex predator.