The Evolution of Venture Nomenclature: From Mythical Beasts to Predictive Metrics

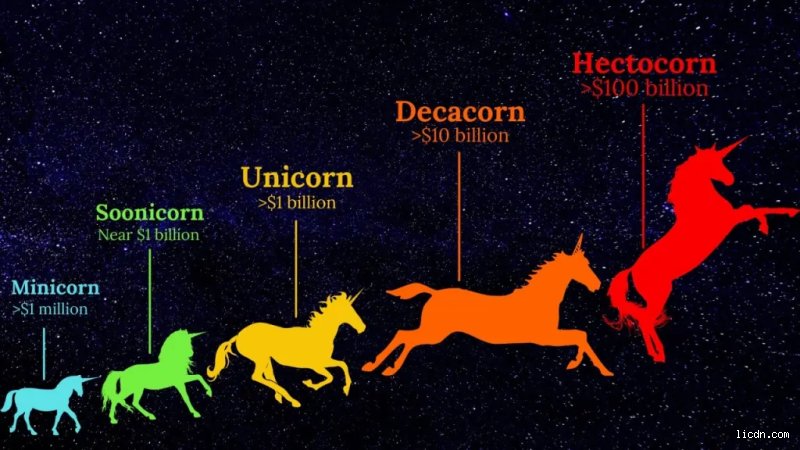

Silicon Valley thrives on folklore. When venture capitalist Aileen Lee coined the term "unicorn" back in 2013, she was highlighting statistical anomalies—rare, venture-backed tech companies that defied the odds to achieve 10-figure valuations. Back then, only 39 companies fit the description. Today, global venture capital databases track over 1,200 unicorns globally, rendering the term slightly less mythical than originally intended.

What is a Unicorn Startup in the Modern Economy?

Let us be real here. A unicorn is no longer an invisible creature; it is a specific asset class. To qualify, a private company must close a funding round—whether Series B, C, or later—that prices its equity at a aggregate worth of $1 billion or more. Think of companies like Stripe or Canva during their meteoric rises. The valuation relies on investor sentiment, forward-looking multiples, and liquidation preferences rather than public market profitability. Because of this, public scrutiny intensifies the moment that ninth zero lands on the spreadsheet.

Defining the Soonicorn: The Next Generation of Market Disruptors

Where it gets tricky is identifying the pre-unicorn cohort. Enter the "soonicorn"—a portmanteau of "soon-to-be unicorn." These are businesses that have outgrown their early-stage training wheels, typically raising substantial Series A or Series B tranches. They are not merely small companies; they are hyper-growth engines pulling in serious annual recurring revenue. The issue remains that their current capitalization does not yet match their market hype, leaving them in a high-stakes waiting room where execution is everything.

The Financial Mechanics: Valuation Methodologies and the Gap That Changes Everything

How do we actually measure the distance between these two stages? It is not just about adding a few hundred million dollars to a balance sheet. The underlying financial engineering changes drastically once a company crosses the threshold.

Discounted Cash Flows vs. Hype Multiples

Soonicorn valuations are often driven by raw momentum, addressable market size, and a desperate fear of missing out among investors. Analysts apply aggressive revenue multiples—sometimes 20x to 50x forward ARR—based on the assumption that triple-digit year-over-year growth will continue indefinitely. Yet, for a unicorn, the valuation methodology must withstand deeper due diligence. Late-stage private equity shops and sovereign wealth funds look at unit economics, customer acquisition cost patterns, and net revenue retention. I believe the industry relies far too heavily on paper valuations, which explains why so many unicorns stumble when they finally face the harsh reality of the public markets.

The Role of Mega-Rounds and Late-Stage Venture Capital

Growth equity firms like Tiger Global, SoftBank Vision Fund, and General Atlantic act as the ultimate kingmakers in this ecosystem. A soonicorn typically secures check sizes between $30 million and $75 million. But to bridge the gap? That requires a mega-round. We are talking about massive injections of $100 million or more in a single financing event. This influx of cash allows the company to aggressively acquire competitors, scale international operations, and build a massive defensive moat. As a result: the valuation artificially spikes, sometimes overnight, converting a promising growth-stage player into an official industry titan.

Operational Velocities: Scaling Friction Inside the Two Tiers

The internal culture of a company undergoing this transition morphs into something unrecognizable. What worked for a 150-person team fighting for market share fails miserably when the headcount hits 800.

The Post-Billion Dollar Corporate Shift

Once the unicorn badge is secured, the administrative burden skyrockets. Founders who used to focus entirely on product development are suddenly dragged into complex corporate governance, international compliance, and investor relations. The scrappy, move-fast-and-break-things ethos disappears. Why? Because a billion-dollar valuation attracts intense regulatory oversight from bodies like the SEC or the European Commission, particularly regarding data privacy and antitrust concerns. People don't think about this enough, but the pressure to protect a massive valuation often stifles the very innovation that created the company in the first place.

The Soonicorn Agility Advantage

Here is where the smaller players actually hold the upper hand. Soonicorns operate with an aggressive agility that their larger counterparts can no longer afford. They can pivot product strategies within a week, target niche demographics without worrying about massive brand dilution, and hire top-tier engineering talent by offering equity with massive upside potential. If a unicorn's stock options feel like a safe corporate bet, a soonicorn's options represent life-changing wealth if the company scales correctly. That changes everything for a hungry engineer looking to make a mark in the tech world.

Comparative Architecture: Mapping Risk, Liquidity, and Exit Horizons

To fully grasp what is the difference between unicorn and soonicorn startup models, one must examine their paths toward a liquidity event. The risk profiles of these two entities are fundamentally asymmetrical.

Risk-Reward Profiles for Late-Stage Investors

Investing in a soonicorn is a classic high-risk, high-return proposition. There is still a distinct possibility the company could run out of runway, misjudge its market fit, or get crushed by an incumbent. However, the upside could be a 5x or 10x return if it achieves unicorn status. For a unicorn investor, the risk is different; they are playing a game of capital preservation and modest upside. They want a clean 2x or 3x return via an initial public offering or a massive strategic acquisition. Honestly, it's unclear whether the current macroeconomic environment can support the sheer volume of unicorns looking for an exit right now, and experts disagree on how many of these companies are genuinely viable long-term.

The S-Curve of Growth and Execution

Every successful tech company follows an S-curve, but their positions on this trajectory define their classification. A soonicorn sits right at the bottom of the steepest slope—growth is accelerating, inefficiencies are masked by rising revenue, and the market opportunity seems limitless. The unicorn sits near the top of that specific growth spurt. It has captured the low-hanging fruit. Now, it must find new revenue streams, optimize its margins, and defend its territory from the next wave of hungry startups. But wait, can a company stay in the soonicorn phase forever? No. The intense burn rate required to sustain that level of growth means a company must either scale up, get acquired, or face a painful down-round down the line.

Common mistakes and misconceptions about these tech echelons

The valuation mirage

Investors often treat a tech valuation as an objective truth carved in marble. It is not. The most glaring blunder observers make is conflating paper wealth with actual market utility. A unicorn startup might boast a ten-figure valuation on a term sheet, yet possess negligible revenue. Because late-stage venture capital metrics frequently rely on preferential liquidation rights, these numbers are artificially inflated. Founders chase the mythical billion-dollar status by sacrificing unit economics, which explains why so many heavily funded entities collapse when public markets demand profitability. You cannot pay salaries with hypothetical equity value.

The linear growth fallacy

Everyone assumes a soonicorn startup smoothly accelerates into a full-fledged unicorn. The problem is that scaling is rarely a predictable, straight line. A company valued at $700 million is not simply 70% of the way to the top tier; it is often sitting at a dangerous precipice. Many growth-stage enterprises burn through cash reserves to artificially sustain a steep trajectory. Let's be clear: a significant portion of these high-potential ventures plateau permanently or experience brutal down-rounds. The transition requires a complete overhaul of operational architecture, not just a larger marketing budget.

Chasing headlines instead of unit economics

Founders frequently optimize for press releases rather than sustainable margins. But vanity metrics do not build enduring empires. Founders look at media darlings and assume that achieving a specific label guarantees survival, except that the tech graveyard is littered with former unicorns like Theranos or WeWork that prioritized hype over substance. It is a classic trap where vanity triumphs over sanity.

The hidden physics of the scaling chasm

The toxic allure of regulatory arbitrage

Expert venture capitalists know a secret that rookies miss: the easiest way to bridge the gap between a soonicorn startup and a billion-dollar valuation is ignoring the law until you are too big to ban. Look at early Uber or Airbnb. They did not just build superior software; they engineered a regulatory blind spot. Yet, this strategy carries immense, unquantified risk. If you build a business model entirely predicated on exploiting legal gray areas, a single municipal ruling can erase half your paper value overnight. (And yes, your expensive corporate lawyers cannot always save you from an angry city council.)

The structural talent trap

The operational machinery changes completely between these two stages. Managing a team of 80 engineers requires a completely different psychological toolkit than steering a multinational workforce of 1,500 people. As a result: many brilliant early-stage executives find themselves pushed out by seasoned corporate operators who understand enterprise bureaucracy. It is a brutal, often heartbreaking evolution that tech blogs rarely discuss.

Frequently Asked Questions

What is the exact survival rate of a soonicorn startup attempting to cross the billion-dollar threshold?

Data from historical venture capital cohorts indicates that only about 15% to 20% of these growth-stage companies successfully attain a 10-figure valuation. According to comprehensive market tracking from platforms like CB Insights, the vast majority of companies stuck in the $500 million to $900 million valuation range either stall out completely, get acquired at a discount, or face down-rounds. For example, during the macroeconomic correction of 2022 and 2023, more than 35% of these highly valued private entities saw their internal valuations slashed by at least half. The step up is a statistical anomaly, not a guaranteed milestone.

Can a company lose its status as a unicorn startup once it has been achieved?

Absolutely, because paper valuations only reflect the price of the most recent investment round. If a business runs out of capital and is forced to raise money at a lower valuation than before, it undergoes a down-round and loses its title. Think of prominent examples like Instacart or Klarna, both of which saw their private market valuations plummet by over 60% during shifting economic cycles. Once the market enthusiasm cools, the artificial valuation floor drops out. In short, the title is temporary, but the structural debt incurred to reach it is permanent.

How does the geographic distribution of a unicorn startup differ from emerging contenders?

The geographic concentration is heavily skewed toward established global tech hubs, though the map is slowly fracturing. Historically, the United States and China controlled over 75% of the billion-dollar landscape. However, emerging ecosystems in India, Southeast Asia, and Latin America are producing an unprecedented volume of growth-stage contenders. This shift occurs because local founders are solving region-specific infrastructure problems rather than blindly copying Silicon Valley models. Consequently, the next generation of market leaders will look radically different from the software giants of the past decade.

A radical reframing of the tech hierarchy

We need to stop worshiping arbitrary financial metrics that serve venture capitalists far more than they serve society or consumers. The obsessive focus on creating another unicorn startup has distorted the entire entrepreneurial ecosystem, encouraging reckless capital deployment at the expense of genuine, resilient innovation. Why do we celebrate a company simply because a handful of private equity funds agreed on a highly manipulated, theoretical valuation? The real winners of the next decade will not be the fragile entities that sprinted to a billion dollars on the back of unsustainable subsidies. Instead, the ultimate prizes will go to the disciplined companies that viewed growth-stage milestones merely as a temporary stepping stone. True corporate resilience cannot be synthesized by venture capital funding alone.