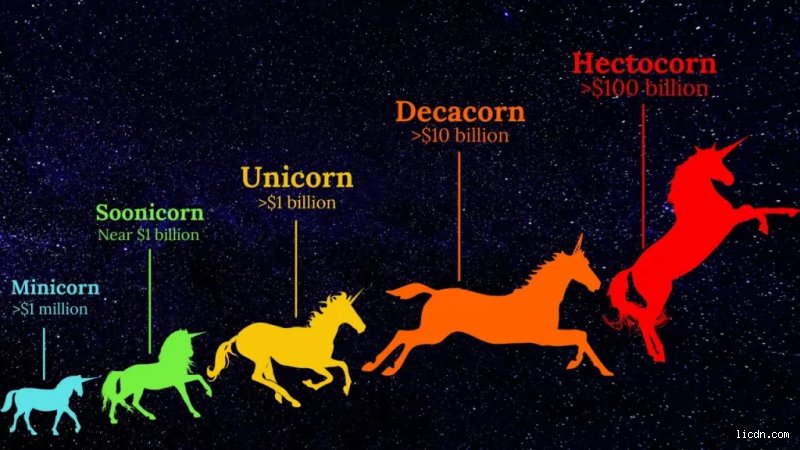

Every founder dreams of the horn. But let's be real for a second—the venture capital ecosystem has shifted dramatically since Cowboy Ventures founder Aileen Lee first coined the term "unicorn" back in 2013. Back then, finding a private company worth ten figures was like spotting a literal mythical creature, with only 39 companies making the original cut. Today, the global herd has ballooned past 1,200, transforming a rare badge of honor into a crowded club. And that changes everything.

The Evolution of Startup Valuation Metrics and Why the Nomenclature Shifted

The thing is, the tech world gets bored easily with its own vocabulary. When the billion-dollar mark became a crowded room filled with everything from enterprise software giants to cash-burning quick-commerce apps, the market needed a new lens to identify tomorrow's winners before their price tags skyrocketed. Hence, the birth of the soonicorn.

From Scarcity to Ubiquity: The 2013 Benchmark vs Today

We used to look at a billion-dollar valuation as the absolute pinnacle of private market success. Now? It is often just a milestone on the way to an IPO or a multi-billion-dollar acquisition. Because of the massive influx of late-stage venture capital over the last decade—particularly during the funding frenzy of 2021—companies are staying private much longer than they did during the dot-com era. Consequently, the soonicorn stage has become the primary battleground for growth equity investors who want to capture massive upside before the valuation premium becomes too steep to justify.

The Psychology of the "Soon" Prefix in Venture Capital

Why do we love these arbitrary labels? It is mostly about signaling. When an ecosystem like India or Southeast Asia boasts a high number of soonicorns, it tells global institutional investors that the pipeline is healthy. It is a predictive metric. Honestly, it's unclear whether some of these companies will ever actually cross the finish line, but the designation alone acts as a magnet for top-tier engineering talent and secondary market liquidity.

Deconstructing the Unicorn: Valuation, Capital Efficiency, and the Burden of the Billion-Dollar Tag

To truly grasp the difference between unicorns and soonicorns, we have to look at the immense pressure that comes with a ten-figure valuation. It is not just a math equation; it is a psychological contract with your investors. When a company hits a $1 billion valuation, the expectations change overnight, and the margin for error completely evaporates.

The Realities of Late-Stage Funding and Liquidation Preferences

Unicorn status is rarely achieved through pure, unadulterated organic growth. It requires massive, multi-million-dollar funding rounds, often led by sovereign wealth funds or mega-funds like SoftBank's Vision Fund. But here is where it gets tricky: those high valuations frequently come with complex structural protections attached to them. Liquidation preferences mean that if a company raises money at a $1.2 billion valuation but eventually sells for $800 million, those late-stage investors get their money back first. The founders and early employees can easily end up with nothing. People don't think about this enough when they celebrate a new unicorn announcement on LinkedIn.

Case Studies in Valuation Corrections

Look at the historical trajectory of companies like Klarna or Instacart. Klarna peaked at a staggering $45.6 billion valuation in 2021, only to see it slashed by 85% down to $6.7 billion during the 2022 market correction. Was it still a unicorn? Yes. But the narrative around the company shifted from triumphant market leader to a cautionary tale about growth-at-all-costs. This is why some founders actually fear the unicorn label; it sets a valuation floor that becomes incredibly difficult to defend if the macroeconomic climate sours.

Inside the Soonicorn Pipeline: Identifying Tomorrow's Market Leaders Today

So, where does that leave the soonicorn? If the unicorn is the seasoned heavyweight boxer trying to defend its title, the soonicorn is the hungry contender climbing the ranks. These companies are usually in their Series B or Series C funding stages, pulling in significant revenue but still nimble enough to pivot when market dynamics shift.

The Growth Metrics That Matter Most

A true soonicorn isn't just a startup with a fancy pitch deck and a charismatic founder. Investors look for specific, hard data points before conferring this status. We are talking about a Net Revenue Retention (NRR) rate above 110%, annualized recurring revenue (ARR) marching toward the $50 million mark, and a clear path to profitability within 18 to 24 months. Except that in the current economic climate, capital efficiency has replaced raw user growth as the metric that matters most. Can you scale without burning through $5 million a month? If the answer is no, you are not a soonicorn; you are just an expensive hobby.

The Regional Powerhouses: Where the Next Herd is Breeding

The geographic distribution of these companies is telling. While Silicon Valley still dominates the absolute numbers, regions like Latin America and India have become absolute factories for soonicorns. In Bengaluru alone, trackers identified over 100 potential unicorns across fintech and SaaS sectors waiting in the wings. These ecosystems are highly localized, solving specific infrastructure problems—like digital payments or supply chain logistics—that global giants like Amazon or Google cannot easily replicate.

Financial Mechanics: How the Valuation Chasm Alters Investment Strategies

The difference between unicorns and soonicorns manifests most clearly in how institutional investors deploy their capital. The risk profile shifts dramatically between a company valued at $400 million and one valued at $1.5 billion.

Risk-Reward Ratios in the Mid-to-Late Stage Transition

For a venture capitalist, investing in a soonicorn offers the potential for a 3x to 5x return by the time the company reaches an IPO or a major secondary sale. But the risk of total failure remains distinct. A unicorn, by contrast, offers lower upside potential for new investors—perhaps a 1.5x or 2x return—but is generally viewed as a safer bet because it has already achieved significant market penetration and brand equity. Yet, as we saw during the recent tech downturn, that safety is often an illusion. Which explains why many crossover funds have started moving upstream, abandoning late-stage unicorns to hunt for value in the soonicorn cohort instead.

Common mistakes and dangerous misconceptions

The valuation mirage

Many spectators assume paper wealth equals cold cash. It does not. A soonicorn valuation is highly volatile, often calculated using aggressive forward revenue multiples that ignore macroeconomic shifts. We saw this when global venture funding plummeted by over 30% in recent cycles, dragging theoretical sub-billion-tech-giants back to reality. The problem is that founders celebrate the milestone before the capital actually clears the bank. High valuations on paper can vanish during the next down-round.

The inevitable graduation fallacy

Does every upcoming market leader become a mythical billion-dollar beast? Absolutely not. Growth is never linear. Some firms plateau permanently because their total addressable market shrinks unexpectedly. Except that tech journalists love writing destiny narratives, implying that crossing the $500 million threshold guarantees entry into the exclusive club. But reality is a graveyard of highly funded scale-ups that simply ran out of runway.

Chasing status over unit economics

Why do executive teams sacrifice profit for a label? Because prestige attracts top-tier talent and press coverage. Yet, optimizing for a vanity title usually destroys the underlying business architecture. Burn rates accelerate dangerously. Startups inflate their gross merchandise value using heavy discounting, which explains why so many businesses collapse immediately after hitting their target valuation.

The hidden engine of secondary liquidity

The cap table pressure cooker

Let's be clear: early employees and angel investors cannot eat paper shares. By the time a business transforms into a prominent pre-unicorn contender, those day-one stakeholders have been waiting seven to ten years for a payout. This creates massive internal friction. Sophisticated founders manage this tension by organizing structured secondary sales, allowing early backers to liquidate a fraction of their equity to institutional buyers. As a result: the company stabilizes its ownership structure without the immense public scrutiny of a traditional initial public offering (IPO).

Frequently Asked Questions

What is the exact financial threshold that separates a unicorn from a soonicorn?

The primary dividing line is the verified $1 billion valuation mark. A difference between unicorns and soonicorns lies in their current audited worth, where the former has officially closed a funding round at or above ten figures, while the latter typically operates in the $200 million to $900 million corridor. Data from recent global tech indexes indicates that fewer than 15% of high-growth scale-ups successfully make this precise financial leap. The rest either get acquired by legacy conglomerates, merge with competitors, or stall due to capital inefficiencies. Did you really think reaching a billion was just a matter of time?

Can a company lose its status after achieving it?

Yes, prestige is temporary. When market corrections hit the tech sector, public market comparables drop, forcing private late-stage businesses to revalue their shares during subsequent financing rounds. Stripe and Instacart famously adjusted their internal valuations downward by tens of billions during recent macroeconomic contractions. If a business raises capital at a lower valuation than its previous round, it suffers a down-round, which can strip away its elite title. In short, maintaining the position requires continuous revenue growth and disciplined fiscal management.

How do geographical ecosystems impact the transition speed?

Location alters the entire trajectory. Silicon Valley, Bangalore, and London possess dense concentrations of late-stage venture capital firms, which accelerates the velocity of large-scale funding rounds. A business operating in these mature hubs can complete the transition in under twenty-four months, whereas an identical company in an emerging market might spend five years chasing the same capital allocation. Cultural risk tolerance also dictates how aggressively local founders burn capital to achieve rapid scale. (We must acknowledge that regional regulatory frameworks also play a massive role in footprint expansion).

The final verdict on valuation vanity

We need to stop treating these arbitrary financial classifications as definitive badges of corporate health. The obsession with hitting a specific ten-figure metric distorts genuine entrepreneurial progress. Chasing a label encourages reckless capital deployment while penalizing sustainable, cash-flow-positive operations. Building a resilient, enduring business matters infinitely more than joining a temporary marketing club. Let's champion durable market infrastructure instead of worshiping inflated balance sheets.