The Messy Origin Story: Unpacking the "Five Six" Misnomer in Modern Banking

Language gets messy when compliance officers and loan underwriters share the same office floor. When people ask about the five six of credit, they usually trip over a semantic collision between ancient banking pillars and strict federal disclosure rules. The mistake is understandable. But where it gets tricky is assuming credit scoring is a singular, monolithic calculation. It is not. I once watched a boutique commercial real estate developer in Miami lose a $14.2 million financing package because he optimized his credit score but completely ignored his liquid capital reserves. He had the "Cs" down on paper, yet he failed the regulatory readiness test. The issue remains that modern lending operates on a dual-track system: qualitative human judgment and rigid statutory math.

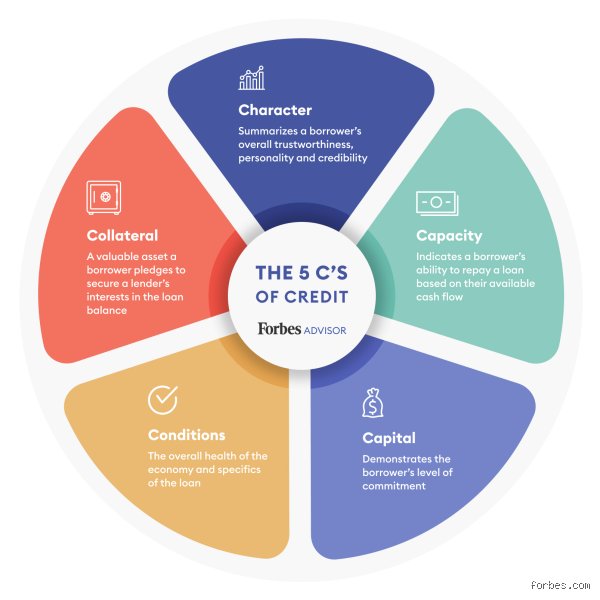

The Historical Weight of the Five Cs

For over a century, traditional underwriting leaned on a qualitative quintet. Bankers wanted to know who you were before they handed over the vault keys. This framework focused on character (your track record), capacity (your debt-to-income ratio), capital (your skin in the game), collateral (the asset backing the play), and conditions (the broader economic climate). Yet, relying solely on these five metrics created massive blind spots, leading to systemic biases and erratic risk assessments across the banking sector prior to the regulatory overhauls of the late twentieth century.

Enter the Six Regulators: The Statutory Overlap

Then came the paperwork nightmare of modern consumer protection laws. When the Consumer Financial Protection Bureau updates its manuals, the industry listens. Regulations like the Truth in Lending Act forced institutions to standardize exactly six pieces of information—including your name, income, social security number, property address, estimated property value, and the mortgage loan amount sought—to trigger an official Loan Estimate. Hence, the "five six" confusion was born in the trenches of retail banking where old-school credit philosophy collides with modern compliance checklists.

Technical Breakdown Part One: Character and Capacity Under the Regulatory Microscope

Let us dismantle the first structural pillar of this borrowing matrix. Character sounds incredibly folksy, like something a small-town bank manager assesses with a firm handshake, but today it means raw data. Underwriters look at your repayment history across a 7-year window, tracking every single late payment on credit cards or auto loans. The thing is, your reputation is now just a digitized compilation of your past financial sins. Do you really think a automated underwriting system cares about your good intentions? We are far from the days of character references; now, your character is a FICO score ranging from 300 to 850.

Calculating the Ultimate Metric: Debt-to-Income Ratio

Capacity is where the math gets brutal. Lending institutions generally demand a front-end debt-to-income ratio below 28 percent for housing costs, and a back-end ratio below 43 percent for total monthly obligations. Because if your fixed costs consume more than nearly half of your gross earnings, a single macroeconomic hiccup will break you. Imagine a consultant in Seattle earning $12,000 a month; if their mortgage, student loans, and Porsche lease total $5,500, they are already sailing dangerously close to the wind, irrespective of their perfect payment history.

The Hidden Traps of Variable Capacity

And what happens if your income fluctuates? Freelancers, commission-based sales reps, and venture-backed entrepreneurs face a completely different underwriting gauntlet. Banks typically average the last 24 months of tax returns, applying a conservative haircut to unpredictable revenue streams. This explains why a tech worker with a volatile bonus structure might struggle to secure a premier tier mortgage despite having a massive net worth. Experts disagree on whether this backward-looking methodology accurately predicts future default rates during technological disruptions, but honestly, it is unclear if a better automated alternative exists.

Technical Breakdown Part Two: Capital, Collateral, and the Reality of Market Conditions

Capital represents your financial shock absorber. If you walk into a commercial bank seeking an acquisition loan for a logistics hub in Ohio without putting down at least 20 percent of your own cash, you will be laughed out of the boardroom. Underwriters want to see significant cash reserves—often measured as six months of principal, interest, taxes, and insurance—sitting untouched in a liquid account. People don't think about this enough: banks hate being the sole risk-bearer in any transaction.

The Changing Face of Collateral Valuation

Collateral is the ultimate safety net for the lender, a physical asset they can seize, liquidate, and turn into cash when everything goes sideways. But valuation is a moving target. During the commercial property correction of recent years, an office tower valued at $50 million in 2022 might only fetch $32 million at auction today, which drastically alters the loan-to-value calculations that risk management departments obsess over during quarterly audits.

The Overlooked Impact of Economic Conditions

You can control your capital, and you can offer up clean collateral, but you cannot dictate the Federal Reserve's interest rate trajectory. Conditions are the wild card of the credit universe. When the central bank hikes benchmark rates, the cost of funds skyrockets across the entire global economy. As a result: an institutional borrower who looked incredibly creditworthy in a low-rate environment suddenly looks like an existential risk when refinancing at higher yields.

The Alternative View: Why the Five Cs Matrix Fails the Modern Economy

The traditional credit framework is showing its age. Critics argue that relying on rigid definitions of capital and character locks out millions of viable borrowers who operate entirely within the gig economy or hold wealth in non-traditional digital assets. Fintech disruptors are completely reimagining the landscape by looking at alternative data streams. They are analyzing cash-flow underwriting—looking at real-time deposit histories and utility payment consistency—rather than relying solely on legacy credit bureau reports.

The Rise of Cash-Flow Underwriting

This alternative approach flips the script on traditional creditworthiness. By analyzing a business or consumer’s daily banking transactional data over a 12-month period, algorithmic platforms can predict default probabilities with astonishing accuracy, sometimes outperforming old-school scoring models by a wide margin. It proves that looking at a static snapshot of collateral is a lagging indicator of financial health.

Algorithmic Bias and the Future of Risk

Except that shifting to purely algorithmic credit assessment introduces its own set of terrifying complications. If an artificial intelligence model trains on historical data that contains human prejudices, it simply automates that discrimination at scale, hiding bias behind a veneer of mathematical objectivity. In short, the industry is caught between an outdated mid-century banking philosophy and an unpredictable, hyper-automated future that nobody fully commands yet.

The Hidden Traps: Common Misconceptions Around the Six Cs of Credit

You think you have memorized the standard underwriting playbook. Let's be clear: blind adherence to textbook definitions will sink your next financing application faster than a sudden interest rate hike. Most borrowers conflate having a solid revenue stream with possessing impeccable capacity, which remains a massive tactical error in modern corporate finance.

The Collateral Mirage

Asset evaluation is completely broken in the minds of eager entrepreneurs. You assume a warehouse valued at $2 million secures a $2 million line of credit effortlessly. Except that banks apply a brutal haircut, often discounting equipment value by up to 60% during liquidation assessments. Your pristine balance sheet means nothing if your primary asset cannot be liquidated within ninety days, which explains why lenders treat specialized machinery with extreme skepticism.

Character vs. Credit Scores

Can a simple three-digit algorithm encapsulate human integrity? Absolutely not. Wealthy applicants often assume a FICO score of 800 grants them automatic passage through the underwriting gauntlet. The problem is that character encompasses pending litigation, regulatory compliance history, and management stability. A single undisclosed lawsuit can completely override a flawless repayment history, rendering your pristine numerical score useless.

The Six Cs of Credit: The Secret Leverage Point of Capital Runway

Everyone talks about cash flow, but they ignore the unspoken reality of business elasticity. Expert lenders secretly prioritize the sixth, often unwritten factor: capital runway, or the actual velocity at which a business burns through its liquid reserves during a macroeconomic downturn.

The Architecture of Capital Runway

This goes far beyond simple liquidity metrics. We are looking at your operational runway when credit markets freeze completely. A company with a current ratio of 2:1 might seem perfectly healthy on paper. Yet, if your monthly overhead is $150,000 and your accounts receivable freeze, that ratio crumbles into dust within forty-five days. True creditworthiness requires demonstrating a minimum of six months of operational runway without relying on fresh debt injection, an expert benchmark that separates surviving entities from bankrupt ones.

Frequently Asked Questions

Which of the six Cs of credit do underwriters prioritize during economic recessions?

During periods of severe market volatility, lenders rapidly pivot their focus toward conditions and capital runway above all else. Historical data from the 2008 financial crisis reveals that banks tightened credit availability by over 43% for small businesses that lacked adaptive operational models. Your personal credit score matters significantly less when your entire industry faces structural collapse. As a result: underwriting departments scrutinize external market trends, supply chain vulnerabilities, and your specific sector exposure before they even glance at your collateral packages. Survival dictates that you prove your business model can withstand a sustained 30% drop in industry-wide consumer demand.

How does a startup with zero asset history satisfy the collateral requirement?

Securing traditional financing without hard machinery or real estate requires pivoting aggressively toward alternative structures like accounts receivable financing or personal guarantees. Startups frequently leverage intellectual property valuations, though intellectual property faces a steep valuation haircut that can reach up to 85% in conservative banking models. Do you really want to pledge your primary residence just to secure a volatile revolving line of credit? Venture debt funds occasionally accept warrants or equity kickers instead of physical assets to mitigate this specific structural hurdle. Consequently, early-stage founders must rely on forward-looking cash flow projections that are backed by signed, legally binding enterprise software contracts.

Can alternative data streams fix a poor character assessment during underwriting?

The short answer is yes, because modern fintech lenders utilize machine learning algorithms to analyze nontraditional indicators like vendor payment consistency and utility bill compliance. Traditional institutions take months to evaluate a borrower, whereas algorithmic platforms analyze over 10,000 distinct data points including real-time accounting software integrations within minutes. This shift allows businesses with historical hiccups to demonstrate current operational rectitude through impeccable transactional consistency. (Though a recent tax lien or active fraud investigation will still trigger an immediate, automated rejection across all platforms). Utilizing these transparent, real-time data ecosystems allows modern enterprises to bypass traditional underwriting biases entirely.

Beyond the Underwriting Grid: A Definitive Take on Capital Acquisition

The entire framework of capital evaluation is fundamentally an exercise in risk asymmetric warfare where the bank holds all the cards. Stop viewing the six Cs of credit as a tedious compliance checklist to be passively fulfilled. It is an aggressive roadmap for operational fortification. If your business cannot survive the scrutiny of a cynical loan officer, it will not survive the chaotic realities of the open market. We must discard the outdated notion that cheap debt is a right earned merely by existing for more than three fiscal quarters. True financial mastery means building an enterprise so structurally resilient, liquid, and transparent that lenders end up competing for the privilege of financing your expansion.