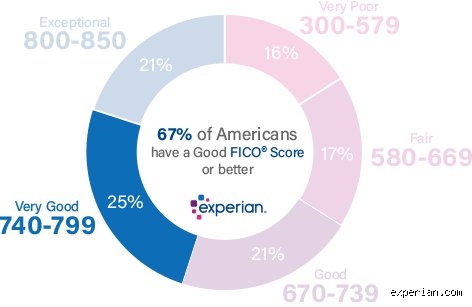

The Anatomy of the Three-Digit Myth: What Does a 740 Credit Rating Actually Mean?

Context is everything. When FICO rolled out its classic scoring model decades ago, it established a hierarchy that modern institutions still worship like gospel, even if the underlying mechanics have shifted dramatically. The Fair Isaac Corporation slots a 740 into the "Very Good" credit tier, a territory occupied by roughly 25% of the American borrowing public. You are firmly above the national average, which currently hovers around 715, yet you are still hovering just outside the pearly gates of the "Exceptional" 800-plus club.

The FICO Calculation Matrix

Where it gets tricky is how you actually arrive at this number. Your history consists of moving parts—payment history accounts for 35%, amounts owed takes up 30%, and the remaining 35% is split between length of history, new inquiries, and your overall credit mix. A person can hit 740 because they have a pristine ten-year history with a minor credit card balance, or conversely, because they are a 24-year-old coding prodigy in San Francisco who has never missed a payment but only opened their first account three years ago. The algorithms do not judge your character; they simply calculate statistical default probabilities, meaning your 740 signals to lenders that there is roughly a 1% chance you will become ninety days delinquent in the next twenty-four months.

VantageScore vs FICO: The Great Disconnect

People don't think about this enough, but a 740 on a FICO 8 model is fundamentally different from a 740 on a VantageScore 4.0. While FICO requires at least six months of history on an account to spit out a metric, VantageScore can generate a profile using just a few weeks of data. Because VantageScore penalizes high utilization much more aggressively, a sudden weekend shopping spree at a Home Depot in Atlanta can tank your VantageScore by forty points while barely scratching your FICO score. Honestly, it's unclear why some fintech apps push VantageScore so heavily when over 90% of top lenders still rely exclusively on FICO variants during the actual underwriting process.

Mortgages, Auto Loans, and Plastic: How Real-World Lenders React to Your Profile

This changes everything. When you walk into a dealership or submit an online mortgage pre-approval, nobody throws a party because you hit 740, but nobody slams the door either. You are in the tier where you get approved almost instantly, yet you might find yourself arguing over the final sixteenth of a percentage point on your interest rate.

The Cutthroat World of Tier 1 Financing

For auto financing, a 740 is your golden ticket to the absolute lowest interest rates available. Dealerships categorize anyone above 720 or 730 as Tier 1 borrowers. This means if Ford Motor Credit is running a 0% APR promotional financing campaign on new electric trucks, you qualify without having to beg or provide three years of tax returns. The issue remains that while you get the best auto rates, the mortgage sector behaves with far less generosity.

Fannie Mae, Freddie Mac, and the Dreaded LLPA Matrix

Mortgage lending is where the question "is 740 a bad score?" actually becomes relevant. Fannie Mae and Freddie Mac utilize Loan-Level Price Adjustments (LLPAs), which are essentially risk-based fees tacked onto conventional loans based on your down payment and credit rating. If you put 20% down on a house with a 740 score, your fee is 0.5% of the total loan amount. But if you can somehow push that number up to 760? That fee drops to 0.25%, which translates to saving thousands of dollars over a thirty-year timeline. I once watched a colleague obsess over a 738 score while buying a home in Denver, and by simply paying off a small retail card to cross the 740 threshold, they altered their total lifetime loan cost by nearly four thousand dollars.

The Hidden Costs of Sitting on the 740 Fence

Complacency is the enemy here. Sitting comfortably at this level feels safe, but it is actually a financial no-man's-land where you are paying a hidden premium for not being perfect. You are clean, but you are not pristine.

The Premium Card Conundrum

Take high-end travel rewards cards like the Chase Sapphire Reserve or the Capital One Venture X. While the marketing materials claim a good rating is sufficient, the actual approvals for these premium products with high minimum limits often favor those with deep, established files. A 740 backed by only two years of history might face a swift rejection or get saddled with a paltry five-thousand-dollar limit. That limits your ability to utilize the card for major business expenses or international travel booking without constantly bumping against your utilization ceiling.

The Psychological Trap of the "Good Enough" Mindset

Why settle for being merely good? The danger of this specific tier is that it breeds a false sense of financial security. You look at your banking app, see the green color coding next to your 740, and assume you have maxed out your economic leverage. We're far from it. If a sudden medical emergency or an administrative error at an insurance company causes a single erroneous late payment to hit your report, a 740 will plummet like a stone into the mid-600s, completely destroying your borrowing power for years. A borrower sitting at 820 has a cushion—a seventy-point drop still leaves them in the premium tier, whereas your 740 leaves you with zero margin for error.

How 740 Compares to the Mythical 850: Is the Chase Worth the Effort?

Experts disagree on whether chasing the perfect score actually yields any tangible, real-world benefits or if it is just a form of digital vanity for financial nerds. Let us look at the actual math rather than the marketing hype.

The Diminishing Returns of Credit Perfection

Once you cross the 760 threshold, the financial advantages begin to flatten out dramatically. A lender offering a conventional mortgage will give the exact same prime interest rate to someone with a 765 as they will to an eccentric billionaire boasting a perfect 850. Hence, stressing over those extra eighty-five points is usually a waste of mental energy that could be better spent optimizing your actual investment portfolio or negotiating a salary increase. The only real difference is bragging rights and the psychological satisfaction of seeing that perfect number on a dashboard.

Real-World Scenarios: The 740 in Action

Consider two buyers, Sarah and Marcus, shopping for the same three-hundred-thousand-dollar home. Sarah has a 740, while Marcus has spent years micromanaging his accounts to maintain an 810. When they apply for their mortgages, their monthly payments might differ by a mere fifteen dollars because they both sit within the prime underwriting brackets for their specific regional bank. As a result: Sarah can use her extra free time to build a side business or remodel her kitchen, while Marcus is still logging into three different banking portals every Tuesday to ensure his utilization never crosses the 1% mark. Perfection has an opportunity cost that nobody talks about.