The Evolution of Digital Trust: What is a Type 2 Audit Report and Where Did It Come From?

The tech industry throws acronyms around like confetti, yet few carry the heavy weight of the Service Organization Control framework. Let's look at the actual roots here. Historically, auditors relied on SAS 70, a standard originally designed to evaluate internal controls over financial reporting. But then the SaaS boom exploded in the early 2000s, pushing legacy frameworks past their breaking point because security isn't just about financial ledgers anymore. The American Institute of Certified Public Accountants (AICPA) realized the market needed a specialized framework, leading to the creation of SSAE 16, and eventually, the SSAE 18 attestation standard used today. That is how the modern SOC 2 framework emerged.

The Architecture of the Trust Services Criteria

You cannot talk about a type 2 audit report without unpacking the foundational Trust Services Criteria (TSC). Auditors evaluate your systems against five specific pillars: Security, Availability, Processing Integrity, Confidentiality, and Privacy. Security is the mandatory baseline—often called the common criteria. But here is where it gets tricky: companies foolishly over-engineer their audits by opting into all five criteria during their first year, which ends up crushing their engineering velocity under a mountain of unnecessary evidence collection. I believe most early-stage B2B startups should strictly focus on the Security and Confidentiality criteria initially because attempting a full-five sweep out of the gate is usually an expensive exercise in vanity.

Why an Auditor's Opinion Statement Matters

When an independent CPA firm like A-LIGN or Schellman issues the final document, the entire exercise hinges on the auditor's opinion section. This isn't a simple pass-or-fail test. The firm issues an unqualified opinion if your controls are designed and operating effectively, a qualified opinion if there are notable gaps, or an adverse opinion if your security posture is a total train wreck. Is an unqualified opinion a guarantee that you will never suffer a data breach? Absolutely not, and anyone who tells you otherwise is selling compliance automation software. Yet, it proves to Fortune 500 procurement teams that you have a functioning security culture.

The Core Mechanics: Measuring the Crucial Element of Time

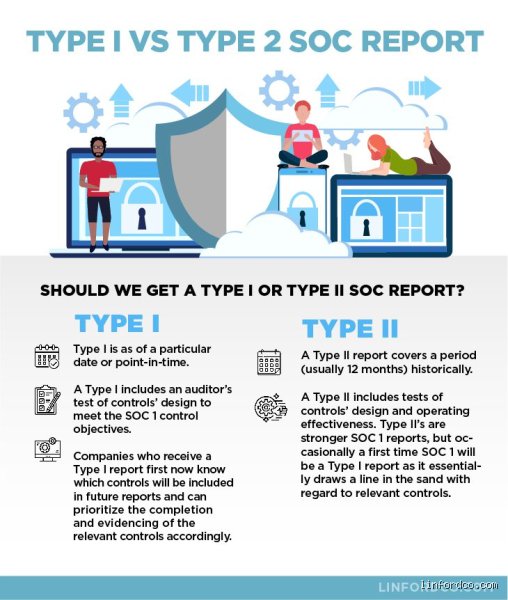

People don't think about this enough: a Type 1 report is just a snapshot of a single day, whereas a Type 2 report is an enduring historical record. Imagine a nightclub bouncer. A Type 1 audit simply verifies that the bouncer is standing at the door at 9:00 PM on a Tuesday, looking professional and holding a flashlight. But what happens at 2:00 AM on a frantic Saturday night when the crowd turns chaotic? A type 2 audit report watches that same bouncer via CCTV footage for six consecutive months to ensure they consistently check IDs and turn away troublemakers when nobody is actively watching them.

The Dreaded Evidence Collection Window

The standard observation window for a Type 2 assessment requires a minimum of six months of historical data, though established enterprise players usually default to a rolling 12-month coverage period to avoid compliance gaps. During this phase, your engineering, HR, and IT infrastructure teams are under a microscope. Every single employee termination must trigger an automated ticket showing access revoke within 24 hours. If your policy states that code reviews require two distinct approvals before a production merge into GitHub, you must prove that this rule held true for every single deployment across that entire timeframe. Skip it once on a frantic Friday afternoon patch, and you risk a qualified opinion.

How Sampling Methodologies Expose Control Failures

Auditors don't just look at a couple of clean logs you hand-selected; they employ rigorous statistical sampling based on the frequency of your controls. For an operational control that executes daily—like automated database backups—an auditor might use AICPA sampling tables to randomly select 25 to 45 individual instances across the review period. What happens if three of those randomly selected days show failed backups with no remediation tickets? That changes everything, as the auditor will note a control deviation, forcing your compliance team into defensive mode during the executive review.

Anatomy of the Final Attestation Document

A complete type 2 audit report is a dense, multi-page artifact that regularly clears 100 pages of technical documentation. It is definitely not light bedtime reading. The document follows a rigid structure prescribed by the AICPA, designed so compliance officers can skip the fluff and immediately locate systemic vulnerabilities.

The Four Vital Components of the Report

Section I contains the Independent Auditor's Report, which provides the high-level opinion and formal signatures from the CPA firm. Section II is management's formal assertion, where your own executive team signs their names on the dotted line, legally stating that they haven't lied about the infrastructure. Then comes Section III, providing a narrative overview of the entire system, covering everything from your AWS infrastructure setup in the us-east-1 region to your background check policies for remote workers in Europe. Finally, Section IV delivers the raw data: a granular table listing every single control, the test performed by the auditor, and the explicit results of those tests.

Decoding Section IV: The Testing Matrix

This is where the rubber meets the road. If your control states "Firewall rules are reviewed quarterly," Section IV will explicitly document the exact dates those reviews occurred—say, March 15, June 14, September 12, and December 11 of the prior year. If a deviation occurred, it is listed right here in plain sight for your prospective clients to read. The issue remains that many sales teams treat this document like a marketing brochure, handing it over to prospects without realizing their own report contains multiple operational deviations that their engineering team conveniently forgot to mention.

Type 1 vs. Type 2: The Strategic Fork in the Compliance Road

When organizations kick off their compliance journey, the immediate dilemma is whether to jump straight into a Type 2 or take a pit stop at Type 1. Conventional compliance wisdom says you must always start with Type 1 to establish a baseline. But honestly, it's unclear if that legacy playbook still makes sense for modern cloud-native startups utilizing automated compliance platforms like Vanta or Drata.

The Hidden Costs of the Type 1 Shortcut

While a Type 1 report can be completed in a matter of weeks since it only looks at today's setup, sophisticated enterprise procurement departments are increasingly rejecting them. They know a Type 1 can be easily gamed by temporarily tightening up access controls the day before the audit and loosening them up the day after. Hence, choosing a Type 1 often means you end up paying double audit fees within the same calendar year because your ultimate destination is always the Type 2 anyway. As a result: you save a bit of time upfront but decimate your quarterly cash flow.

Common Pitfalls and Dangerous Misconceptions

Many procurement officers treat a Type 2 audit report like a golden ticket, a magical shield that instantly absolves a vendor of all security sins. Except that it doesn't. A common blunder involves ignoring the actual scope of the examination, assuming every single server and software module is covered under that shiny seal. It is a classic trap. If your vendor utilizes a subservice organization for hosting, say an AWS or Azure instance, and the auditor carved out that infrastructure from the examination boundaries, you are staring at a massive security blind spot. You must verify whether the inclusive or carcass-carve-out method was deployed before celebrating.

The Pass-or-Fail Illusion

Let's be clear: CPAs do not issue a pass or fail grade. They provide an opinion on whether controls are designed appropriately and operate effectively over a specific period. You might open a Type 2 audit report and discover dozens of operating exceptions scattered across the testing matrices. Does that mean the vendor failed? Not necessarily. The business might still maintain effective overall security if compensating controls mitigated those specific failures. Conversely, a report with zero exceptions could merely mean the auditor sampled the luckiest days of the fiscal year.

Confusing Type 1 with Type 2

Why do organizations keep buying the wrong document? Because a Type 1 report is cheaper, faster, and requires far less stamina from the vendor's compliance team. But a Type 1 only looks at design at a single point in time, perhaps a random Tuesday in November. It proves nothing about operational history. Relying on it for long-term vendor risk management is like marrying someone because they looked nice in a single photograph.

The Hidden Machinery: Complementary User Entity Controls

Here is the dirty secret of third-party risk management that compliance officers rarely whisper aloud: the report is a two-way street. Tucked away in Section III or IV of a comprehensive SOC 2 Type 2 verification lies a list of obligations called Complementary User Entity Controls (CUECs). The vendor is explicitly telling you that their systems are only secure if you, the client, do your homework. If the vendor builds a secure API but you fail to rotate the access keys on your end, who is to blame when a data breach occurs? The issue remains that companies rarely read this section, essentially leaving the back door wide open while marveling at the deadbolt on the front door.

Mastering the Bridge Letter Gap

What happens when an audit period ends on December 31st, but you are signing a major contract in April? You enter the compliance dead zone. Auditors will not cover those four missing months without a fresh engagement, which explains why smart buyers demand a gap or bridge letter. This is a signed statement where management swears under penalty of corporate embarrassment that no material changes have broken their control environment since the last report ended. It is not a legal guarantee, yet it provides the necessary paper trail to satisfy your internal legal counsel during contract negotiations.

Frequently Asked Questions

How long does a Type 2 audit report remain valid for vendor risk assessments?

A standard type 2 audit report typically covers a historical testing window of 6 to 12 months, meaning its formal validity expires the moment the period ends. However, most financial institutions and enterprise buyers accept a finalized report for up to 12 months following its issuance date, provided it is accompanied by a corporate bridge letter if more than 90 days have elapsed. In highly regulated sectors like healthcare or fintech, 84% of compliance officers reject reports that look at a historical window of less than six consecutive months because shorter periods fail to demonstrate true operational consistency. As a result: organizations must establish a continuous intake pipeline to refresh these documents annually rather than treating vendor governance as a one-time onboarding chore.

What is the average cost and timeline for a service organization to obtain this report?

For a mid-sized software provider, generating a comprehensive historical internal controls report requires an investment ranging from $35,000 to $90,000 in direct auditor fees alone. The timeline spans anywhere from 7 to 14 months because the organization must first endure a readiness assessment, remediate broken workflows, and then allow the auditor to observe their active environment for a minimum testing period. Why would any startup willingly subject themselves to this administrative torture? Because enterprise buyers increasingly refuse to sign deals without seeing this documentation, making the hefty price tag a mandatory cost of doing business in the modern B2B marketplace.

Can a company redact sensitive information from the report before sharing it?

Service organizations frequently remove specific customer names, proprietary network architecture diagrams, or granular IP addresses from the final document to protect their internal security boundaries. They cannot, however, alter the independent auditor's opinion, remove listed control exceptions, or delete entire sections of the text without completely destroying the document's professional credibility. If a vendor hands you a heavily sanitized PDF where the testing tables are missing or the independent accountant's letter has been truncated, you should immediately halt procurement. A legitimate attestation of operational effectiveness requires full transparency regarding the control objectives tested, otherwise the document becomes an expensive marketing brochure instead of an objective security assessment.

The Reality of Trust in a Distributed Ecosystem

We live in an era where data is scattered across dozens of unverified cloud systems, making blind trust a corporate suicide strategy. A Type 2 audit report is not a flawless guarantee of safety, nor does it mean a vendor is completely immune to sophisticated cyber attacks. It simply proves that an independent third party spent months verifying that the vendor actually follows the security rules they claim to practice. If you are not actively reading the exceptions, checking the CUECs, and demanding annual updates, you are just collecting PDFs to satisfy an insurance checklist. True risk management requires looking past the clean opinion on the first page and auditing the actual substance of the report.