The Evolution of Assurance: Why a Type 1 Report in Audit Matters Today

We used to live in a corporate world where a handshake and a vague Statement on Auditing Standards number 70 (SAS 70) letter sufficed to seal multimillion-dollar enterprise software deals. Then the cloud exploded. The American Institute of Certified Public Accountants (AICPA) realized that the old ways were dead, births of new frameworks happened, and eventually, the Statement on Standards for Attestation Engagements number 18 (SSAE 18) became our modern bible. The thing is, many executives still treat compliance like a checkbox exercise, completely ignoring how a Type 1 report in audit acts as the literal foundation for institutional trust.

From SAS 70 to SSAE 18: A Shift in Accountability

The transition was not just semantic; it changed the entire landscape of vendor risk management. When the SSAE 16 framework was updated to SSAE 18 in May 2017, the auditing world demanded something radical: service organizations had to take actual responsibility for their subservice organizations. I find it fascinating how many modern CTOs do not realize that if they host their application on Amazon Web Services (AWS) in Northern Virginia, their own Type 1 report must explicitly account for that infrastructure dependency. It is no longer acceptable to point a finger at your cloud provider and shrug.

The Point-in-Time Reality Check

Let us be entirely honest here. A Type 1 report in audit is a snapshot, not a movie. If an independent Certified Public Accountant (CPA) walks into your headquarters in Austin, Texas, on June 15, 2026, and verifies that your firewalls are configured correctly, that your password complexity policies require twelve characters, and that termination procedures remove ex-employees from the system within twenty-four hours, you pass. But what happens on June 16? People don't think about this enough: a company can look like a fortress on Monday and revert to complete operational chaos by Tuesday morning. That changes everything regarding how risk officers interpret these documents.

Anatomy of the Attestation: What Actually Goes into the Document?

A standard Type 1 report in audit is not a brief two-page certificate you can frame on a lobby wall, despite what some aggressive marketing departments might lead you to believe. It is a dense, often dry, multi-page architectural blueprint. The final artifact contains specific components that must adhere strictly to AICPA guidelines, leaving very little room for creative writing or corporate obfuscation.

The Independent Auditor's Opinion

This is where the rubber meets the road. The auditor provides a formal opinion on whether the description fairly presents the system that was designed and implemented, and whether the controls were suitably designed to achieve the specified control objectives. Experts disagree on how much weight this opinion holds compared to historical data, but if you receive a qualified opinion—meaning the auditor found significant flaws in your design logic—your enterprise sales pipeline will grind to an immediate, painful halt.

The Management Assertion

Before the auditors even write their first sentence, your own leadership team must officially state that the system description is accurate. It is an exercise in radical self-honesty. Why is this included? Because it prevents corporate officers from claiming ignorance if a massive data breach occurs later; you signed the paper stating these controls were active on that specific date.

The System Description: Mapping the Infrastructure

This section reads like a technical biography of your product. It outlines the boundaries of your system, the services provided, the nature of the data processed, and the software, people, and procedures involved. For example, a fintech platform operating out of New York might detail its use of Advanced Encryption Standard 256-bit (AES-256) for data at rest, alongside its physical security measures for its secondary data center in New Jersey.

The Mechanics of Suitability of Design

Where it gets tricky for most operational teams is understanding what "suitability of design" actually means in a practical framework. The auditor is not testing if your employees followed the rules for six consecutive months. Instead, they are looking at the math and the logic of your governance structure to determine if your theoretical plan is capable of preventing a catastrophic failure.

The Logic Gap: Design vs. Operating Effectiveness

Imagine building a digital vault to protect sensitive financial records. The auditor reviews your blueprints and notes that the vault walls are made of reinforced steel, the biometric scanner requires a dual-factor cryptographic key, and the logging system records every entry attempt to an immutable ledger. That is an excellent design. The Type 1 report in audit validates that these features exist on the blueprint and are installed on the day of inspection. Yet, the issue remains: what if the vault door is left propped open with a plastic chair because the air conditioning broke? That is a question of operating effectiveness, which is entirely outside the scope of a Type 1 engagement.

Control Objectives and Their Financial Relevance

Because a SOC 1 framework is explicitly tied to Internal Control over Financial Reporting (ICFR), every single control objective must tie back to user entities' financial statements. If a SaaS company processes payroll batches totaling $50,000,000 monthly, their control objectives must ensure that data inputs are complete, accurate, and authorized. A control that simply states "we have a nice office culture" is completely useless here; the focus is strictly on data integrity, change management, logical access, and physical security configurations that prevent unauthorized financial manipulation.

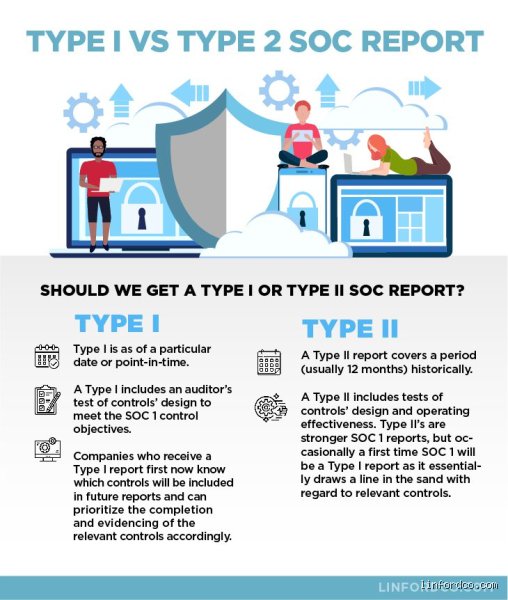

Type 1 vs. Type 2: The Perpetual Compliance Dilemma

Every compliance officer eventually faces the ultimate dilemma: do we stop at a Type 1 report in audit or immediately invest the capital and operational hours into pursuing a Type 2 report? The conventional wisdom states that Type 1 is just a stepping stone, a lesser certification that sophisticated buyers look down upon. But we're far from it being completely useless, and nuance dictates that your current corporate maturity should dictate the path.

The Immediate Cost-Benefit Analysis

A Type 1 engagement is faster and significantly less expensive than a Type 2 review. While a full Type 2 audit requires a historical testing window—usually between 6 and 12 months—a Type 1 can be completed in a fraction of that time because the auditor only needs to verify a single instance of each control. For a cash-strapped startup aiming to close a critical Series A funding round or land an anchor enterprise client by the end of the quarter, choosing a Type 1 report is often the only viable strategic move available. Except that you cannot stay there forever.

The Client Trust Threshold

Large institutional buyers, especially tier-one banks and healthcare conglomerates, are increasingly hesitant to accept a standalone Type 1 report for long-term vendor relationships. They know the loopholes. They understand that a company can clean up its act for a brief 24-hour window, pass the Type 1 audit, and immediately slide back into risky operational habits. Hence, many procurement departments accept a Type 1 report only under a strict contractual caveat: you must deliver a comprehensive SOC 1 Type 2 report within 180 days of signing the master services agreement.

Common mistakes and misconceptions surrounding the SOC 1 assessment

Many procurement officers glance at a vendor compliance folder, spot a logo, and check a box. They assume any SOC stamp guarantees absolute security. This is a massive blunder because a type 1 report in audit documents a single, fleeting microsecond in time. It proves nothing about operational history. It is the architectural blueprint of a house, not proof that the roof will withstand a Category 5 hurricane tomorrow morning.

Confusing design with operational execution

Why do smart compliance managers fall into this trap? The issue remains that a Type 1 evaluation merely confirms that control objectives are suitably designed as of a specific date, such as October 31. If a disgruntled system administrator rogue-deletes a primary database on November 1, the previous day's report remains technically accurate. It represents a static snapshot. It does not evaluate whether your vendor actually executes these processes consistently over a six-month window.

Assuming a Type 1 replaces a Type 2

Let's be clear: relying solely on this limited assessment for long-term vendor governance is reckless. Startups love them because they are cheaper, requiring fewer auditor hours and costing around $15,000 to $25,000 compared to the $40,000+ price tag of a Type 2. Yet, substituting the former for the latter leaves a gaping hole in your risk management framework. If your enterprise handles sensitive financial data, a Type 1 is merely your stepping stone, a temporary hall pass before the real examination begins.

The hidden leverage of Complementary User Entity Controls

There is a dark corner in these documents that almost every reader ignores. Service organizations hide their own vulnerabilities behind a section known as Complementary User Entity Controls, or CUECs. If you do not read this section, you are essentially flying blind.

The poison pill in your compliance report

The problem is that a service organization control overview is a two-way street. A cloud payroll provider can design the most impenetrable cryptographic key management system on earth. But what happens if their report stipulates that you, the client, must securely manage your own administrative passwords? If your staff leaves credentials written on sticky notes, the provider's compliance posture disintegrates. As a result: your organization becomes the weakest link, invalidating the entire security apparatus. You cannot outsource your ultimate fiduciary responsibility.

Frequently Asked Questions

How long is a type 1 report in audit considered valid by regulators?

A static attestation has an incredibly short shelf life, typically decaying in value the moment the ink dries on the auditor's signature. Most financial institutions and institutional auditors accept a type 1 report in audit as valid for only 90 to 180 days from the specified point-in-time date. After this window closes, relying parties will invariably demand a bridge letter or a full Type 2 rollover. In fact, a recent industry survey indicated that 74 percent of enterprise risk officers reject point-in-time reports that are older than six months without accompanying compensating controls. Do not expect a report from last fiscal year to satisfy a modern, cynical IT auditor.

Can a Type 1 assessment cover security and privacy principles?

Yes, though it requires shifting from a SOC 1 framework to a SOC 2 framework while maintaining the point-in-time methodology. While a SOC 1 targets internal controls over financial reporting, a SOC 2 investigates security, availability, processing integrity, confidentiality, and privacy. The underlying mechanics of the point-in-time audit opinion remain identical across both frameworks, evaluating design suitability at a specific calendar milestone. Because of this structural alignment, organizations frequently utilize a Type 1 SOC 2 to establish a baseline before committing to a grueling 12-month observation period.

What is the average duration required to complete this specific audit?

The timeline for executing this assessment is surprisingly brief, which explains its immense popularity among early-stage tech firms. Because the practitioner does not need to gather transaction samples over a multi-month testing window, the fieldwork phase usually wraps up in 2 to 4 weeks. The CPA firm focuses entirely on walkthroughs, system narrative reviews, and policy inspections to verify that control mechanisms are in place. But are you truly prepared to mistake a brief 20-day inspection for a bulletproof guarantee of operational resilience? Once fieldwork concludes, the final report issuance takes another 14 days of internal quality control review.

A definitive stance on point-in-time compliance

We need to stop pretending that a type 1 report in audit is a comprehensive shield against operational failure. It is an initial diagnostic tool, nothing more. Relying on it for permanent vendor oversight is the corporate equivalent of checking a car's oil level while the engine is turned off and assuming the transmission will never fail on the highway. Organizations must aggressively push their critical third-party vendors toward continuous operational testing frameworks. Security is an ongoing, exhausting marathon rather than a photogenic pose struck for an auditor on a random Tuesday afternoon. Demand the deeper scrutiny of behavioral testing, or prepare to answer for the gaps when an avoidable breach inevitably shatters your compliance illusion.