The Concrete Foundations: What is GAAP and Where Did It Come From?

We need to stop viewing accounting rules as mere bureaucratic box-checking. They are, in fact, the rules of engagement for capitalism. Concocted over decades of economic triumphs and catastrophic market crashes—most notably the Wall Street collapse of 1929—GAAP represents a massive, evolving collection of standards maintained by the Financial Accounting Standards Board (FASB). The thing is, people don't think about this enough: money flows where trust exists, and trust cannot exist without a shared rulebook.

The Historical Imperative of Financial Standardization

Before the SEC was established via the Securities Exchange Act of 1934, companies could pretty much report whatever numbers they felt like concocting. It was wild. To fix this, the federal government essentially outsourced the creation of accounting standards to the private sector, which eventually birthed FASB in 1973. Since then, this Norwalk, Connecticut-based independent board has been issuing Accounting Standards Updates (ASUs) that form the current FASB Accounting Standards Codification. This is not a static document; it changes whenever new financial instruments or economic realities emerge. Did anyone anticipate the complexity of revenue recognition for cloud computing subscriptions back in the seventies? Obviously not, which explains why the rules must adapt continually.

The Core Principles That Govern the Numbers

At its heart, this framework relies on a few non-negotiable concepts. You have the monetary unit assumption, the economic entity assumption, and the notoriously tricky matching principle. This last one dictates that expenses must be matched with the revenues they helped generate in the same reporting period. This is where it gets tricky for tech startups. If an enterprise software firm spends $50,000 on marketing in December 2025 to secure a contract that starts in January 2026, GAAP forces them to handle those numbers with absolute precision regarding timing. It prevents corporations from accelerating revenues or burying losses to look more appealing to investors before a big quarterly announcement.

Publicly Traded Giants: The Non-Negotiable Mandate for Wall Street

For any company listed on the New York Stock Exchange (NYSE) or NASDAQ, adopting these standards is not a polite suggestion. It is a strict legal requirement enforced with iron fists by the SEC. Whether you are looking at an behemoth like Apple Inc. or a newly public tech unicorn, your chief financial officer must sign off on financial statements that adhere strictly to these principles. Every 10-K annual report and 10-Q quarterly filing must be scrubbed by independent certified public accountants (CPAs) who issue an official opinion on whether the books fairly present the financial position in conformity with GAAP.

The SEC Enforcement Engine and Investor Protection

Why is the federal government so obsessed with this? Because without a uniform standard, comparing a retail giant like Walmart with an energy firm like ExxonMobil would be completely impossible. I believe that market liquidity depends entirely on this forced uniformity. When an asset manager at BlackRock looks at a company's balance sheet, they need to know that accounts receivable means the exact same thing across the board. When Enron famously manipulated its books using off-balance-sheet vehicles in 2001, it wasn't just a failure of morals; it was a violent manipulation of accounting loopholes that eventually forced Congress to pass the Sarbanes-Oxley Act, tightening the screws on financial reporting even further.

The Reality of Earnings Season and Public Perceptions

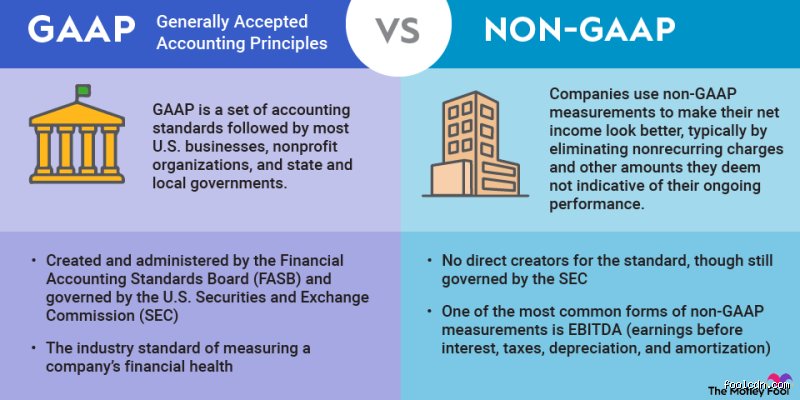

Every quarter, the financial world holds its breath for earnings season. Companies report their net income and diluted earnings per share (EPS). But here is a subtle irony: many corporations actually report two sets of numbers simultaneously. They give you the official GAAP metrics, and then they introduce their own custom Non-GAAP adjusted earnings, usually stripping out stock-based compensation or one-time restructuring costs to make themselves look a whole lot healthier. Analysts love to debate which number matters more. Honestly, it's unclear which metric truly reflects a company's long-term value, but the official numbers remain the anchor that keeps corporate imaginations grounded in reality.

The Private Sector Paradox: Why Non-Public Companies Volunteer for Accounting Torture

If you own a private company, the SEC does not care about your bookkeeping. You could theoretically track your revenue on a series of napkins. Yet, thousands of mid-sized private firms across America spend tens of thousands of dollars annually to ensure their financials are fully GAAP-compliant. Why subject yourself to that nightmare voluntarily? Because the moment you need serious money, everything changes.

The Gatekeepers of Capital: Commercial Banks and Private Equity

Imagine you run a manufacturing plant in Ohio and want to secure a $10 million credit line to purchase new automated machinery. The commercial lending officers at JPMorgan Chase or local regional banks will immediately demand audited financial statements. If those statements are not prepared using GAAP, the loan application is effectively dead on arrival. Lenders require this because they need to calculate debt-service coverage ratios and leverage metrics using formulas they trust. The issue remains that banks are inherently risk-averse; they have no desire to decode a proprietary accounting system that you or your local bookkeeper dreamt up over the weekend.

Preparing for the Ultimate Liquidity Event

Moreover, private companies often dream of being acquired or going public via an initial public offering (IPO). If a venture capital firm or a private equity fund decides to buy a stake in your business, their due diligence team will tear your ledger apart. If they discover you have been using cash-basis accounting instead of accrual accounting, it will delay the transaction for months—or kill it entirely. They will force you to restate your historical earnings, a painful process that frequently reveals the business is far less profitable than the founders believed. In short, adopting rigorous standards early is a strategy for survival and scale.

The Global Divide: Navigating the Friction Between GAAP and IFRS

It is easy to forget that American rules only dominate within the borders of the United States. The rest of the civilized world operates on a completely different system known as International Financial Reporting Standards (IFRS), which is managed by the International Accounting Standards Board (IASB) based in London. This creates an immense amount of friction for multinational corporations that operate across borders.

Rules-Based Rigidness versus Principles-Based Flexibility

The fundamental philosophical difference between these two systems comes down to rules versus principles. The American framework is notoriously rules-based, featuring thousands of pages of highly specific, granular guidance for almost every imaginable scenario. It is a defensive shield designed to protect auditors from litigation. If the book says you can do it, you can do it. IFRS, by contrast, is principles-based, offering broader conceptual frameworks and trusting the professional judgment of the accountants to reflect the economic substance of a transaction. That changes everything when it comes to international business deals.

Inventory Valuation and the LIFO Prohibitions

Let us look at a glaring, concrete example of this clash that affects billions in corporate valuations: the Last-In, First-Out (LIFO) inventory valuation method. Under U.S. accounting rules, companies are allowed to use LIFO, which assumes that the last items placed in inventory are the first ones sold. In times of high inflation, like the economic environment of 2022 and 2023, LIFO allows companies to report higher costs of goods sold, which conveniently lowers their reported net income and slashes their corporate tax bill. Except that IFRS completely bans LIFO. European companies must use First-In, First-Out (FIFO) or weighted-average cost methods. Consequently, an American auto parts distributor and a German competitor could have identical physical warehouses but report wildly different financial realities on paper, which makes global market analysis a minefield for the uninitiated.

Common mistakes and misconceptions about GAAP

The illusion of global ubiquity

You probably think every major corporation on Earth bows to the same financial deity. Except that they do not. A massive blunder is conflating US Generally Accepted Accounting Principles with International Financial Reporting Standards. They are distinct beasts. While over 140 jurisdictions mandate IFRS, Uncle Sam stubbornly clings to his domestic framework. If you analyze a German automaker using American metrics, your valuation will collapse spectacularly. The rules governing revenue recognition and inventory valuation diverge wildly between these two systems.

The myth of absolute mathematical truth

Accounting sounds rigid, like concrete. Yet, financial statement compilation under GAAP is actually an art form masquerading as arithmetic. Many novice investors believe net income is an immutable fact. It is not. Management exercises immense discretion through estimates, depreciation schedules, and asset impairment calculations. A company might report a $50 million net profit while bleeding operational cash flow. Why? Because accrual accounting records economic events when they occur, regardless of when the actual greenbacks change hands. Let's be clear: numbers lie when you ignore the footnotes.

Size does not grant automatic immunity

Does a tiny startup need to bother with these complex rulebooks? Because many founders assume compliance is strictly for the Fortune 500, they neglect standardized reporting entirely. This is a fatal miscalculation. The moment you seek a $2 million Series A funding round or a traditional bank line of credit, institutional gatekeepers will demand standard-compliant historical ledgers. Ignoring these principles early on merely defers a massive, expensive cleanup bill from a CPA firm later.

Expert advice: Navigating the gray areas of accounting principles

Exploiting the disclosure footnotes for alpha

The real magic does not happen on the balance sheet. It lurks in the dense, uninviting pages of the notes to the financial statements. As a result: this is where companies bury their radioactive secrets. You should hunt for changes in accounting estimates, pending litigation liabilities, and off-balance-sheet arrangements. For example, a sudden shift from the First-In, First-Out inventory method to Last-In, First-Out can artificially inflate or deflate reported earnings during inflationary cycles. Is anyone actually reading these三百page documents? Rarely. That is precisely where your analytical edge lies.

The issue remains: Substance over form

Aggressive corporate attorneys love structuring transactions that technically satisfy the letter of the law while violating its spirit. They build complex special purpose entities to hide debt. To combat this, master the principle of conservatism, which dictates that expenses should be recognized sooner rather than later, and gains only when certain. (This is the financial equivalent of expecting rain but hoping for sunshine). When evaluating a company, always penalize management teams that walk right up to the regulatory ledge without jumping.

Frequently Asked Questions

Does every single business in the United States have to use GAAP?

No, there is no blanket federal law forcing the mom-and-pop bakery on your corner to adopt these tortuous rules. In fact, out of the roughly 33 million small businesses operating across America, the vast majority utilize simple cash-basis accounting or tax-basis frameworks instead. However, the mandate aggressively kicks in for the approximate 7,000 publicly traded corporations regulated by the Securities and Exchange Commission. Furthermore, any private entity seeking serious capital will find that over 85% of commercial lenders require standardized audited statements before approving seven-figure commercial loans.

How do these principles impact private equity valuation?

Private equity firms rely heavily on standardized metrics to normalize earnings before buying out a target company. The issue remains that private sellers often present manicured, non-compliant books that mask structural weaknesses. By forcing a target's historical data into a strict regulatory mold, private equity analysts can accurately calculate historical EBITDA without entrepreneurial distortion. This standardization allows institutional funds to compare a software firm in Texas with a manufacturing plant in Ohio on an identical playing field. Without this baseline, setting a fair acquisition multiple becomes an impossible guessing game.

Can a company switch from GAAP to IFRS voluntarily?

American domestic issuers are strictly forbidden from choosing international standards for their SEC filings. Foreign companies listed on US exchanges enjoy this luxury, but domestic entities must stick to the home team rules. Which explains why multinational conglomerates maintain dual ledgers, a staggeringly expensive logistical nightmare. If an American firm wants to switch entirely, it must legally relocate its corporate headquarters overseas and change its regulatory domicile. In short, you are locked into the system unless you flee the American financial jurisdiction entirely.

An honest take on the future of financial reporting

We must stop pretending that these accounting standards are a perfect shield against corporate malfeasance. They are an evolving, bureaucratic compromise that frequently lags behind technological innovation, particularly concerning digital assets and intellectual property. Yet, abandoning a unified framework would plunge global capital markets into absolute chaos. Standardized financial reporting provides the friction-free trust that allows trillions of dollars to move across borders daily. Investors do not need flawless rules; we need a predictable, transparent yardstick to measure risk. Demanding total perfection from a human-made system is a fool's errand, but demanding unwavering consistency is non-negotiable.