The Messy Evolution of Corporate Ledger Keeping

We have this romanticized, entirely inaccurate view of accountants as quiet clerks wearing green eyeshades, mechanically logging numbers into a dusty book. People don't think about this enough, but modern financial tracking wasn't born out of a desire for neatness; it was forged in the fires of corporate scandals and market crashes. When the South Sea Bubble burst in 1720, investors realized that numbers could be easily manipulated without standardized frameworks. This realization eventually gave rise to the rigid structures we navigate today. Yet, the system remains imperfect, a reality that became painfully obvious during the 2001 Enron collapse.

Why a Single Financial Record No Longer Suffices

A modern multinational corporation like Apple or Toyota cannot operate on a single, catch-all set of books. Why? Because the person deciding whether to lend a company $50 million needs an entirely different dataset than the internal factory manager trying to reduce the scrap rate of aluminum chassis in a Shenzhen facility. If you try to mix these perspectives, the data becomes useless mud. That changes everything for growing businesses. Accountants had to split their DNA into specialized functions, creating distinct pathways for external reporting and internal optimization.

The Friction Between Compliance and Strategy

Here is where it gets tricky. There is an inherent, almost violent tension between keeping the regulators happy and steering a company toward future profits. I have seen countless executives prioritize GAAP compliance over internal cost visibility, which often leads to disastrous strategic decisions. Honestly, it's unclear why so many business schools teach these disciplines as complementary sisters. In reality, they are often at war with one another, fighting for the limited time and attention of corporate controllers.

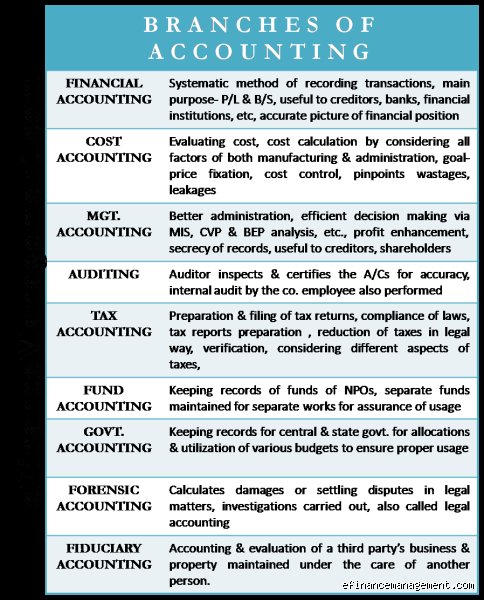

Financial Accounting: The Public Face of Corporate Worth

Financial accounting is the highly regulated process of aggregating historical transaction data into standardized financial statements for external consumption. When Wall Street analysts tear apart a company’s quarterly earnings release, they are looking exclusively at the output of this specific branch. It is backward-looking by nature, functioning like a corporate rearview mirror that logs what happened between January 1st and December 31st of any given fiscal year.

The Iron Cage of GAAP and IFRS Frameworks

You cannot simply invent your own way of calculating profit. External stakeholders demand uniformity, which explains why financial accountants must adhere strictly to either Generally Accepted Accounting Principles (GAAP) in the United States or International Financial Reporting Standards (IFRS) across the European Union and much of the developing world. This rigidity creates bizarre anomalies. For instance, under GAAP, a company's internal brand value—even a massive one like Coca-Cola—cannot be listed as an asset on the balance sheet, but if another firm buys that brand, suddenly billions of dollars in goodwill appear overnight. It is an arbitrary system, yet it remains the only language global markets collectively understand.

The Holy Trinity of External Reporting

The ultimate output of this branch consists of three core documents: the income statement, the balance sheet, and the cash flow statement. Each serves a distinct purpose. The balance sheet offers a static snapshot of assets and liabilities at a single point in time, while the income statement tracks profitability over a specific duration. But the cash flow statement is where the real truth hides—reconciling net income back to actual, cold hard cash. A company can report magnificent paper profits while simultaneously hurtling toward bankruptcy because its cash is trapped in unpaid accounts receivable.

Public Trust and the Double-Entry Safeguard

Every transaction requires a debit and a corresponding credit. This elegant mathematical symmetry, codified by the Franciscan friar Luca Pacioli in 1494, ensures the fundamental accounting equation always balances. But don't mistake balancing for accuracy. A transaction can be completely fraudulent and still balance perfectly if the fake numbers are entered on both sides of the ledger.

Managerial Accounting: The Internal Engine of Decision Making

If financial accounting is a rigid history lesson for strangers, managerial accounting is a lawless, forward-looking crystal ball designed exclusively for insiders. No regulators care about this data. No external investor will ever see these reports. As a result, companies can structure this information however they see fit, abandoning GAAP entirely to focus on granular operational reality.

Predicting the Future Through Cost Volatility

Managerial accountants spend their days obsessing over cost behavior, variance analysis, and future budgeting. They slice the company into tiny pieces, evaluating the profitability of a single product line, a specific retail location, or even an individual employee's output. The focus shifts from historical precision to rapid estimation. A rough, 80% accurate report delivered on a Tuesday morning is infinitely more valuable to a CEO making a critical manufacturing decision than a flawless audited statement delivered three months too late.

The Nuance of Overhead Allocation

Where do corporate costs actually belong? This question causes endless internal warfare within organizations. Imagine a Tesla factory producing both Model 3s and Model Ys on the same assembly line. How much of the factory's electricity bill should be charged to each vehicle type? Managerial accountants use sophisticated methods like Activity-Based Costing (ABC) to trace these indirect expenses back to specific activities, preventing managers from accidentally subsidizing unprofitable products.

Comparing External Compliance with Internal Agility

The divergence between these two systems creates a fascinating corporate paradox. A company can look incredibly healthy to external investors utilizing financial accounting metrics, while its internal managerial reports show systemic rot in its core supply chain. Conversely, heavy upfront research expenditures might make a biotech firm look disastrously unprofitable on its public income statement, yet internal projections indicate a massive payout within five years.

The Structural Divergence of Data Requirements

The structural differences are stark, as seen when comparing the foundational rules, target audiences, and temporal focus of both systems. Financial reporting demands precision down to the last penny, whereas internal management reports frequently round to the nearest thousand or million dollars to facilitate faster decision-making. The table below outlines how these two halves of the accounting world diverge across key operational vectors.

Comparison of Reporting Philosophies and Constraints| Operational Vector | Financial Accounting Framework | Managerial Accounting Framework |

| Primary Audience | External stakeholders (investors, creditors, SEC) | Internal leadership (executives, plant managers) |

| Regulatory Compliance | Mandatory adherence to GAAP or IFRS | Completely optional; custom-built formats |

| Level of Aggregation | Holistic corporate entity viewpoint | Segmented view (by product, region, or division) |

The Fallacy of the Unified Database

Many software vendors will try to convince you that a single enterprise resource planning system can effortlessly bridge this divide without human intervention. We are far from it. The issue remains that data categorization requires human judgment. A single shipping invoice from FedEx can be classified as a generic period expense for external reporting, but internally, it must be dissected to see if that specific shipment was expedited due to a preventable manufacturing delay in Ohio.

Common mistakes and dangerous misconceptions

You probably think numbers never lie. The problem is, they behave exactly like a liquid, shaping themselves entirely to the container of the specific discipline you choose. A massive blunder is assuming that financial reporting rules apply to internal cost metrics. They do not. If a factory manager uses rigid GAAP principles to determine whether to drop a lagging product line, disaster strikes. Why? Because compliance frameworks deliberately ignore opportunity costs and behavioral psychology. Corporate leaders frequently conflate these boundaries, expecting a standard tax return to double as a strategic growth map. Let's be clear: a document optimized to legally starve the tax collector is utterly useless for convincing a venture capitalist to fund your expansion.

The trap of looking backward

Historical data acts as a security blanket for corporate executives. Because tax and financial branches demand a precise autopsy of the past twelve months, professionals assume this retrospective lens solves future dilemmas. It fails. Management accounting requires a forward-looking posture where imprecise projections outweigh historical perfection. Waiting for audited, immaculate statements before adjusting prices ensures your business dies with beautifully balanced books.

Confusing cash flow with profitability

This is where the three branches of accounting become dangerously tangled in the minds of novice entrepreneurs. Your tax return might show a glowing net profit of $450,000, yet your corporate checking account sits in the red. Accrual methodologies required by external stakeholders paint a picture of theoretical wealth, ignoring the brutal reality of unpaid invoices and inventory holding costs. Which explains why solvent companies routinely go bankrupt during rapid scaling phases.

The hidden engine: behavioral accounting and expert advice

Look past the balance sheets and you will find a psychological battlefield. Budgets are not neutral spreadsheets; they are invisible mechanisms that dictate human behavior. When an organization designs an internal metric system, it inadvertently tells employees exactly how to game the system. If you measure a purchasing department solely on lowering unit costs, they will bulk-buy inferior components, destroying product quality. This hidden dimension of management reporting determines whether an enterprise thrives or cannibalizes itself from within.

Decoupling compliance from strategy

How do you weaponize this knowledge? My advice is uncompromising: completely separate your compliance machinery from your operational pulse. Hire a ruthless specialist for your tax strategy, but do not let them near your weekly operational meetings. You must treat financial, tax, and management functions as three distinct languages spoken by the same entity. Intermingling them creates a corporate tower of Babel where no one understands the true definition of performance.

Frequently Asked Questions

Which of the three branches of accounting commands the highest starting salary?

Corporate reality dictated that management and strategic positions pulled ahead significantly over the last fiscal cycle. Recent labor metrics indicate that specialized cost analysts and corporate controllers command an average starting compensation of $92,000, outstripping entry-level tax preparers who average closer to $68,000. This variance exists because corporate enterprises willingly pay a premium for predictive insights that directly inflate profit margins. The issue remains that compliance roles are increasingly vulnerable to automated algorithmic processing, which suppresses entry-level wage growth in traditional bookkeeping sectors. Consequently, positioning yourself at the intersection of data analytics and internal corporate strategy yields a 35% higher earning trajectory over a ten-year horizon.

Can a small business survive by utilizing only one specific branch?

Is it truly possible to navigate a ship with only a rearview mirror? A lean startup might initially survive solely on tax compliance methods to satisfy annual government mandates, but this minimalist approach guarantees stagnation. Without internal cost tracking, you blindly guess at product pricing while praying your cash reserves outlast your mistakes. As a result: overhead costs secretly balloon, quietly bleeding the enterprise dry while the owner celebrates a phantom profit margin. True operational longevity requires an immediate, albeit basic, integration of internal tracking tools the moment your enterprise surpasses $100,000 in gross revenue.

How is artificial intelligence reshaping these traditional accounting disciplines?

Automation has thoroughly demolished the tedious data-entry tasks that historically clogged the tax and financial reporting workflows. Software now categorizes 94% of standard bank ledger transactions without human intervention, shifting the professional focus toward complex regulatory interpretation. Yet, the internal management branch remains highly resistant to complete automation due to the erratic nature of human corporate politics and subjective forecasting. Machines excel at calculating what occurred, but they flounder when predicting how a sales team will react to a restructured commission framework. In short, AI transforms modern accountants from data historians into strategic corporate navigators.

The final verdict on financial architecture

We must stop viewing these three branches of accounting as mere administrative chores to be tolerated. They form a interconnected trinity of corporate survival, where weakness in a single pillar compromises the structural integrity of the entire enterprise. It is a mistake to worship financial compliance while ignoring the behavioral undercurrents of internal cost metrics. Step away from the illusion that a perfectly filed tax return means your business model is inherently healthy. Winners aggressively exploit the tension between these disciplines to extract actionable truth from their operational data. (And yes, it requires messy, continuous calibration.) Command all three viewpoints simultaneously, or watch your enterprise become a statistic.