The Hidden Machinery of Global Beverage Giants

Let us look at what we are actually measuring here. Wall Street does not judge a corporate empire solely by the cash sitting in its bank vault, which explains why comparing these two requires a bit of financial dissection. Coca-Cola, trading under the ticker symbol KO, operates as a pure-play beverage company. PepsiCo, known as PEP on the New York Stock Exchange, is a radically different beast altogether.

The Pure-Play Focus of the Atlanta Giant

Coca-Cola has spent over a century perfecting a single trick: selling liquid refreshment. They do not own the trucks that deliver every bottle to your local corner store in Madrid or Tokyo, nor do they typically own the bottling plants themselves. Instead, they sell highly concentrated syrup to independent bottling partners. It is an incredibly asset-light model that generates staggering profit margins because they avoid the massive overhead of manufacturing and distribution logistics.

The Purchase New York Diversification Play

PepsiCo chose a completely different path back in 1965 when CEO Donald Kendall shook hands with Frito-Lay wizard Herman Lay. That single moment changed the trajectory of the corporate soda wars forever. By merging sugar water with salty snacks, PepsiCo created a consumer goods monster that controls everything from Quaker Oats to Doritos. Where it gets tricky is managing the sheer physical weight of this operation, which demands thousands of delivery trucks, massive factories, and complex agricultural supply chains.

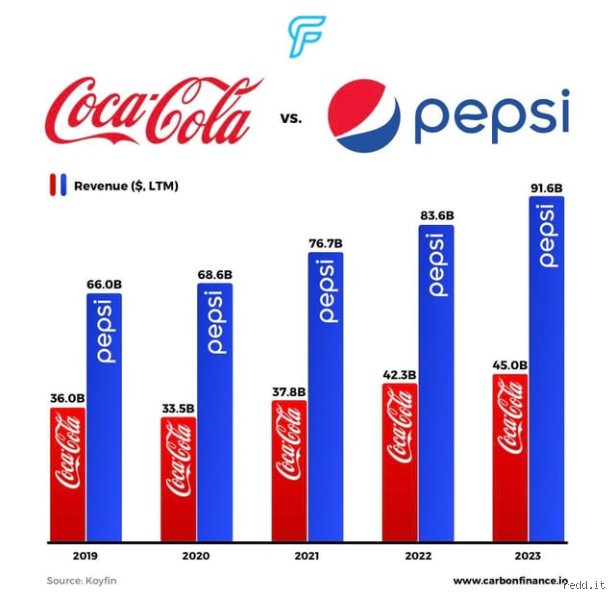

Deconstructing the Revenue Machine: A Tale of Two Balances

When you stack their recent annual filings side by side, the sheer scale of the disparity becomes obvious. PepsiCo routinely posts annual revenues exceeding $91 billion across its global footprint. Coca-Cola, by contrast, brings in roughly $45 billion in top-line revenue. That changes everything if your only metric for being richer is the total amount of money flowing through the register. But we are far from a simple conclusion because revenue is only what you collect, not what you actually keep.

The Margin Miracle of Coca-Cola

This is where the Atlanta playbook shines. Because Coca-Cola focuses almost exclusively on syrup and licensing, its operating margins frequently hover around a staggering 28 percent to 30 percent. When you strip away the costs of doing business, Coke routinely converts its smaller revenue stream into more than $10 billion in pure net income. I have analyzed corporate balance sheets for years, and few massive conglomerates can match the sheer wealth-generating efficiency of the classic Coke formula.

The Heavy Toll of the Frito-Lay Empire

PepsiCo operates on much thinner ice when it comes to profitability. Delivering millions of bags of Lay's potato chips to supermarkets requires an army of workers and immense fuel costs, forcing their overall operating margins down into the 13 percent to 14 percent range. The food business is a brutal, low-margin slog. Even though Pepsi generates double the sales of its rival, its annual net income usually lands around the same $10 billion mark as Coca-Cola. The issue remains: more work for the exact same reward at the bottom of the ledger.

Market Capitalization: What the Global Investors Say

To truly understand who is richer, Pepsi or Coke, we have to look at market capitalization, which represents the total value of all outstanding shares on the stock market. Investors pay a premium for predictability and high margins. As a result, Wall Street frequently values Coca-Cola at a higher total market cap than PepsiCo, with Coke often hovering around $270 billion while PepsiCo trails slightly behind near $230 billion.

Why Wall Street Loves the Red Brand

Investors hate risk. Coca-Cola owns an unparalleled distribution network that functions almost like a global utility, ensuring that whether someone is walking through a market in Nairobi or a stadium in Los Angeles, they can buy a Sprite or a Dasani. This hyper-focused beverage ecosystem allows the company to weather economic downturns easily. Which explains why Warren Buffett has held his massive multi-billion-dollar stake in KO through his firm Berkshire Hathaway since 1988 without selling a single share.

The Battle of Tangible Assets and Brand Valuation

If a sudden global catastrophe wiped out every stock market on earth, who would own more actual stuff? PepsiCo owns an astronomical amount of real estate, processing plants, and fleet vehicles. Yet, brand value consulting firms like Interbrand consistently rank the Coca-Cola trademark as one of the most valuable intangible assets in human history, often pricing the brand name alone at over $58 billion. Honest analysts disagree on how to balance physical trucks against cultural dominance, making it unclear who holds the ultimate upper hand when the dust settles.

The Real Estate and Factory Footprint

PepsiCo owns hundreds of massive snack-processing facilities across continents, from massive Quaker Oats mills in Iowa to crisp factories in the United Kingdom. These are hard, tangible assets that hold immense liquidated value. Coca-Cola simply does not need this level of heavy infrastructure. Except that if the global supply chain fractures, owning the physical means of production, as Pepsi does, provides a unique layer of industrial security that a mere brand recipe cannot match. This structural divergence ensures the debate remains fiercely contested among financial experts who evaluate corporate power through radically different lenses.

Common Mistakes and Misconceptions Regarding Corporate Wealth

The Revenue Mirage Versus Profit Realities

Most amateur investors fall into the trap of staring blindly at top-line revenue, completely forgetting that PepsiCo operates a massive food business alongside its beverage empire. You might look at the raw numbers and assume the snack giant crushes its historic rival because it brings in billions more in absolute cash inflows every single year. Except that, Frito-Lay chips and Quaker Oats require colossal supply chains, agricultural raw materials, and heavy manufacturing infrastructure. Coca-Cola, by contrast, operates an incredibly streamlined model focused primarily on selling highly concentrated syrups to independent bottling partners. Consequently, Coke boasts significantly higher net profit margins, often hovering around 20% to 25%, while Pepsi struggles to cross the 11% threshold. Who is richer, Pepsi or Coke? The answer shifts dramatically the moment you stop measuring the size of the truck and start measuring the weight of the actual gold inside it.

Confusing Brand Value With Market Capitalization

Another classic blunder involves equating global cultural ubiquity with actual balance sheet dominance. We see the red script logo everywhere, from remote villages to high-end restaurants, which leads to the assumption that Coke is an untouchable financial monolith. Let's be clear: brand equity is an intangible asset, not liquid wealth. Wall Street values these entities based on future cash flows and risk diversification, not just sentimentality. While Interbrand consistently ranks the Coca-Cola trademark as vastly more valuable than Pepsi's, the stock market capitalization tells a parallel story where both giants frequently dance around the $250 billion to $300 billion valuation mark. Is a company richer because its logo is worth more, or because its diversified portfolio cushions it against a sudden global war on sugar?

The Hidden Engine: Snack Subsidies and Asset Velocity

The Frito-Lay Monopolistic Shield

To truly understand the modern dynamic of who is richer, Pepsi or Coke, one must look deep into the salty snack aisle. PepsiCo owns over 60% of the United States chip market, a terrifyingly dominant position that generates immense, predictable cash flows. This junk-food empire effectively subsidizes their endless cola price wars against Atlanta. When carbonated soft drink sales dip due to health trends, Doritos and Cheetos pick up the slack seamlessly. The issue remains that Coca-Cola possesses no such savory fallback option, meaning they are completely tethered to the liquid refreshment landscape. Yet, this extreme specialization allows Coke to rotate its assets with surgical precision, achieving a return on equity that makes tech companies jealous.

The Dictatorship of the Bottling System

We must also dissect how these empires actually hold their tangible wealth. Decades ago, Coca-Cola spun off much of its capital-intensive bottling operations into independent entities, removing heavy machinery and massive truck fleets from its own books. PepsiCo chose a contrasting path, re-acquiring major bottlers to command absolute control over its entire distribution matrix. (This logistical nightmare is precisely why Pepsi has double the employee count of Coke.) As a result: Pepsi controls the actual physical shelf space in supermarkets with brutal efficiency, but they pay a heavy toll in maintenance costs. Coke travels light, leaving the heavy lifting to its global network of partners while it cashes high-margin syrup checks.

Frequently Asked Questions

Which company has higher total annual revenue?

PepsiCo consistently generates vastly more top-line revenue than Coca-Cola, with recent annual figures showing Pepsi pulling in over $91 billion compared to Coke's roughly $45 billion. This massive gap exists because PepsiCo is a sprawling food and beverage conglomerate, whereas Coca-Cola remains almost exclusively dedicated to drinks. The snack division, powered by international giants like Lay's and Ruffles, accounts for more than half of Pepsi's total intake. However, this massive influx of cash does not automatically make them wealthier, as their operational costs are exponentially higher. Therefore, looking at revenue alone provides a highly distorted view of who is richer, Pepsi or Coke.

Who wins the battle of market capitalization on Wall Street?

The crown for the highest total market valuation fluctuates constantly, but Coca-Cola frequently commands a higher or equal market capitalization despite having half the revenue of its rival. Investors willingly pay a premium for Coke's stock because the company boasts superior capital efficiency and remarkably steady dividend payouts. For instance, Coca-Cola's net income regularly matches or exceeds PepsiCo's, often landing right around $10.5 billion annually for both firms. This parity means Wall Street values Coke's concentrated, high-margin beverage strategy just as highly as Pepsi's diversified snack empire. Because market cap changes daily with stock ticker movements, neither company maintains a permanent, definitive lead in total paper wealth.

Does Warren Buffett own shares in both companies?

The legendary billionaire investor Warren Buffett is famously a massive shareholder in Coca-Cola through his conglomerate, Berkshire Hathaway, holding a stake worth over $24 billion for decades. He notoriously shuns PepsiCo, consuming multiple cans of Cherry Coke every single day while praising Coke's impenetrable competitive moat. Buffett loves the simplicity of Coke's business model, which requires very little capital reinvestment to maintain its global dominance. Which explains why he has never accumulated a major position in Pepsi, despite recognizing their formidable strength in the snack industry. His unwavering loyalty reinforces the perception among institutional investors that Coke is the safer, more resilient cash generator.

The Ultimate Verdict on Corporate Wealth

Declaring a definitive victor in this centennial war requires choosing between raw muscle and pure efficiency. If you define wealth as sheer size, operational footprint, and total cash moving through the system, PepsiCo reigns supreme without question. But if wealth means profitability, brand power, and the ability to extract massive margins from simple commodities, Coca-Cola takes the crown. The problem is that we are comparing an agile software-like syrup machine with a colossal industrial food titan. Our view is that Coca-Cola is fundamentally richer because its financial engine is far more elegant, requiring less effort to generate identical net profits. They turned colored sugar water into the ultimate printing press, and that is a masterpiece of capitalism no bag of potato chips can ever truly match.