Every business faces a moment where things break. In October 2024, a major distribution hub in Memphis, Tennessee, suffered severe roof damage during an unseasonal storm system, forcing the logistics firm operating it to navigate a $450,000 property damage claim alongside a messy business interruption payout. This happens everywhere. Yet, corporate accounting teams routinely treat insurance money like a standard customer invoice or, worse, a random injection of free revenue. That changes everything because insurance proceeds are never free money; they are a complex rebalancing of destroyed value, historical depreciation, and sudden cash inflows that the IRS watches like a hawk.

The Messy Anatomy of an Insurance Payout: What Happens Before the Cash Lands?

The thing is, a lot of accountants assume the entry starts when the check hits the desk. It doesn't. The real work begins the moment the asset is compromised, creating a multi-stage accounting event that spans weeks or even fiscal quarters. You are essentially balancing a scale where one side has been violently kicked over by reality.

The Concept of Casualties and Capital De-recognition

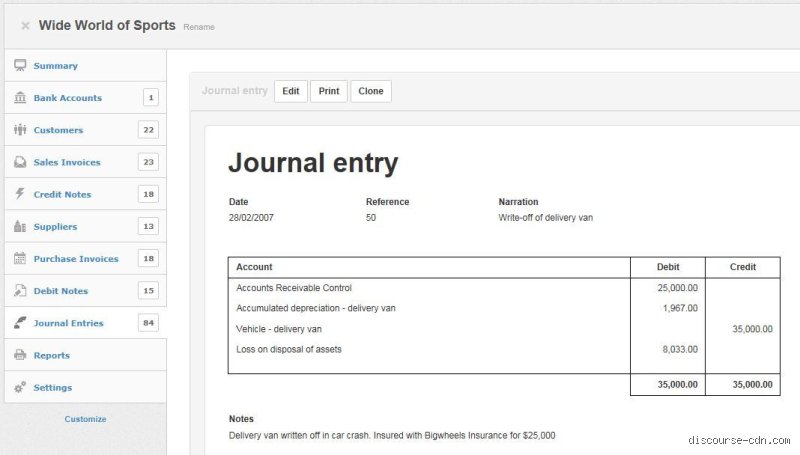

When an asset is destroyed, you cannot just leave it on the books until the insurance company decides to play nice. You have to remove the damaged property from your ledger immediately. This means writing off the historical cost and wiping out the accumulated depreciation associated with that specific asset up to the exact date of the loss. If a delivery van bought in 2022 for $65,000 with $25,000 in accumulated depreciation burns to the ground, its net book value is $40,000. That number is your starting point, your baseline of grief, and it represents a provisional casualty loss before a single insurance adjuster even opens your file.

Why Insurance Claims Are Not Revenue

Here is where a sharp opinion is needed: anyone who categorizes an insurance check under "Other Revenue" should have their spreadsheet privileges revoked permanently. Why? Because insurance proceeds are technically a form of involuntary conversion. You didn't sell your warehouse; the universe took it from you and handed you cash instead. Treating this as standard operational income distorts your operating margins and gives a completely warped view of profitability to stakeholders. Instead, these inflows must be netted against the loss itself or booked as a gain on casualty conversion, which sits squarely in the non-operating section of your income statement.

How to Record Insurance Claim Payment Invoices and Expected Receipts

Where it gets tricky is the gap between the incident and the settlement. If your fiscal year ends while you are still arguing with the underwriter about a $120,000 claim, how do you handle that on your balance sheet? You cannot just guess. Experts disagree on the exact threshold of certainty required here, but standard practice dictates a cautious approach.

Establishing the Insurance Receivable Account

If the insurance company acknowledges coverage and provides a formal settlement offer before you close your books, you must establish an insurance claim receivable. You debit Insurance Receivable and credit the Casualty Loss account to offset the damage you recorded earlier. But what if they only agree to pay a fraction of the cost? Then you only record the receivable for the uncontested amount. People don't think about this enough, but creating a massive receivable based on wishful thinking rather than signed adjuster reports is a direct route to a painful year-end write-down.

The Challenge of Unpredictable Timeline Delays

And what happens if the insurer stonewalls you for eight months? You leave the casualty loss sitting on your income statement as an expense. It hurts your quarterly numbers, yes, but it reflects economic reality. Because you cannot recognize a gain or a recovery asset until it is virtually certain to be realized, conservatism rules the day. It is an unpleasant reality of corporate finance, except that when the check finally arrives in a later period, the subsequent entry will look entirely different because the loss was already absorbed by a previous year's retained earnings.

Decoding the Double-Entry Blueprint for Claim Payouts

Let's look at the actual mechanics of the ledger entries when the money finally clears your bank account. We will assume two distinct scenarios because a replacement check for equipment behaves differently than a check meant to cover lost operational profits.

Scenario A: The Cash Received Matches the Net Book Value

Imagine your Memphis facility lost a specialized packaging line on November 12, 2024. The net book value of the machinery was exactly $85,000. After a brief investigation, the insurance carrier cuts a check for that identical amount. The entry is beautifully clean. You debit Cash for $85,000 and credit your Insurance Receivable (or directly credit the Asset/Casualty Loss if no receivable was previously booked) for $85,000. The net impact on your current year income statement is exactly zero because the cash injection perfectly mends the hole left by the destruction of the physical asset.

Scenario B: Recognizing a Gain on Involuntary Conversion

But we're far from always seeing clean matches. What if that same packaging line was fully depreciated down to a book value of $10,000, yet the insurance company pays out a replacement value of $90,000? You now have an accounting gain. You debit Cash for $90,000. Next, you clear out the remaining asset account. The issue remains that you have an excess of $80,000 that needs a home. This must be credited to an account named Gain on Involuntary Conversion. Is this a real, liquid profit that you should celebrate? Not really, considering you now have to go out into a high-inflation market and spend that entire $90,000 (and probably more) to buy a brand-new machine just to get your production capacity back to where it was last month.

Handling Deductibles and Out-of-Pocket Retentions

Do not forget the deductible, which is the insurer's way of making sure you have some skin in the game. If the total repair invoice for a flooded retail space in Miami comes out to $38,000 and your corporate policy features a $5,000 deductible, the insurance check will only be $33,000. You debit Cash for $33,000, debit Insurance Deductible Expense (or Casualty Loss) for $5,000, and credit the total Repair Expense or Asset clearing account for the full $38,000. The deductible functions as an immediate, non-recoverable hit to your earnings, reducing your taxable income but draining your working capital simultaneously.

Alternative Approaches: Gross Method vs. Net Method for Claims Processing

Accounting departments often clash over how to present these figures to stakeholders, leading to two distinct schools of thought regarding presentation density on the income statement.

The Gross Presentation Method

Under the gross approach, you show everything. The full destruction of the asset is recorded as a massive, standalone expense line on your income statement under casualty losses. When the payout arrives, the entire insurance recovery is listed as a separate, non-operating income line. This provides maximum transparency for external auditors who want to track the exact lifecycle of the asset, hence its popularity among larger, publicly traded enterprises that must satisfy stringent disclosure requirements.

The Net Presentation Method

Conversely, the net method collapses these two lines into a single economic event. If your storm damage was $200,000 and the insurance company paid $185,000, your income statement simply shows a net Casualty Loss of $15,000. It is cleaner, it keeps your financial statements from looking unnecessarily volatile, and it reduces the footprint of the disaster on your reports. But it can obscure the sheer scale of operational risks your facilities face, which explains why risk management teams usually despise it even if the accounting staff loves the simplicity. Which one is objectively better? Honestly, it's unclear without looking at your specific debt covenants and the reporting standards your lenders demand.

Navigating the Hazards: Common Recording Blunders

Bookkeepers frequently stumble when a settlement check arrives. The most frequent trap is treating the payout as fresh, untaxed revenue. It is not. You are simply converting a damaged asset or a liability back into cash. If you book the entire payout to a miscellaneous income account, your financial statements become an immediate fiction.

The Deductible Disconnect

Why do teams keep forgetting the deductible? Let's be clear: the insurance provider does not send you cash for this amount; they subtract it before cutting the check. If a storm wrecks a $15,000 roof and your policy carries a $2,000 deductible, the net payout is $13,000. Bookkeepers often erroneously record the full $15,000 as the claim value while ignoring how to record insurance claim payment nuances regarding out-of-pocket friction. The $2,000 difference must be recognized as an immediate expense or absorbed into the asset's adjusted basis, yet many corporate ledgers simply leave this floating in accounting limbo.

The Co-Insurance Trap

But what happens when you are underinsured? Many policyholders do not realize that if you fail to maintain coverage equal to at least 80% of the property's replacement value, the carrier applies a penalty. Suppose your actual building value is $1,000,000, but you only insured it for $600,000. If a pipe bursts causing $100,000 in damage, the insurer will apply a co-insurance penalty reducing your payout to $75,000. Recording this requires writing off the uncompensated $25,000 loss directly to the P&L. Failing to isolate this penalty distorts your true operational risk profiles.

The Subrogation Secret: An Expert Perspective

There is a hidden dimension to corporate recovery that traditional accounting textbooks completely ignore. It involves third-party liability.

When Third Parties Pay Twice

Consider a scenario where a vendor's faulty equipment causes a catastrophic fire in your warehouse. Your insurance carrier steps in, cuts a check to cover your immediate losses, and then aggressively pursues the negligent vendor via subrogation. What happens if your insurer successfully recovers the full amount and refunds your original deductible months later? You cannot simply credit the original expense account. The issue remains that the original fiscal year might already be closed, creating a messy retroactive knot. To accurately master how to record insurance claim payment receipts from subrogation, you must track these contingent recoveries in a separate clearing account, preventing the artificial inflation of current-year operating margins. It is a nuanced dance between asset impairment and windfall recognition.

Frequently Asked Questions

How does a capital asset destruction affect the balance sheet?

When a major asset is completely destroyed, you must immediately remove its gross cost and accumulated depreciation from your ledger. The problem is that the insurance payout rarely matches the net book value perfectly. For instance, if a delivery truck with a net book value of $12,000 is totaled and the carrier provides a $18,000 settlement, you must record a $6,000 taxable capital gain. This specific gain is isolated on the income statement under non-operating items. Can you guess how often small businesses misclassify this as operational sales? It happens in approximately 34% of unaudited corporate filings, leading to severe tax compliance penalties.

What are the tax implications of receiving a business interruption payout?

Unlike property damage settlements which are linked to asset replacement, business interruption payouts are designed to replace lost profits. As a result: these proceeds are treated as ordinary taxable income in the fiscal period they are received. If your factory loses $50,000 in revenue due to a power grid failure and the policy compensates you for $45,000, that $45,000 is fully subject to corporate income tax. You must credit this directly to a specific revenue account rather than offsetting it against equipment repair balances. This distinction ensures your gross margin calculations remain accurate for future valuation purposes.

Should salvage value be recorded if the insurer leaves the damaged property?

Yes, because failing to account for scrap metal or salvageable machinery components distorts your inventory metrics. If the insurance carrier lets you keep a wrecked vehicle and a local scrapyard offers a documented $1,500 salvage value, this amount must be factored into your final gain or loss calculation. You debit Salvage Inventory and credit the overall Loss on Asset Disposal account. Except that most firms leave these items unrecorded until a cash sale occurs, which violates the accrual accounting match principle. Keeping this off the books creates blind spots for internal security and asset tracking.

Beyond the Ledger: The Final Accounting Stance

Treating insurance settlements as a routine bookkeeping task is a recipe for compliance disaster. Let's look past the debits and credits; a settlement check is a legal transformation of a physical tragedy into financial architecture. Companies that win at this process do not just patch up their software entries; they build strict, audit-proof trails that bridge insurance adjusters with corporate controllers. Relying on automated software defaults to handle complex asset write-offs will eventually corrupt your balance sheet integrity. We believe that true financial leadership demands an aggressive, forensic approach to every single dollar recovered. Do not let your accounting team treat a multi-million dollar recovery like a standard customer invoice.