Decoding the Schedule K-1: Why This Paperwork Torments Every Business Partner

The IRS Schedule K-1 is the tax document issued to individuals who hold an equity stake in pass-through entities like partnerships, limited liability companies, or S-corporations. Instead of the corporation itself paying federal income taxes, the profits (and losses) flow straight onto your personal Form 1040 Schedule E. Because of this architectural design of the US tax code, you are legally responsible for paying taxes on money you might never even touch.

The Lethal Distinction Between Allocations and Distributions

Where it gets tricky is the gap between allocations and distributions. Suppose you own 25% of Apex Logistics LLC in Columbus, Ohio. In 2025, the company had a spectacular year and generated $400,000 in net taxable income. Your Schedule K-1, specifically in Box 1 or Box 2, will show a $100,000 allocation of that profit, which you must report to the IRS. But what if the managing partners decided to reinvest every single penny into buying new delivery vans? You receive exactly $0 in cash distributions (Box 19, Code A), yet you still owe taxes on that $100,000 phantom income. I find it utterly absurd that someone can face a massive tax bill without the liquidity to pay it, but that is the law.

Why Traditional W-2 Workers Fail to Understand the K-1 Trap

People don't think about this enough: a W-2 employee receives cash, pays taxes on that cash, and goes home. The K-1 world flips this logic on its head. Your taxable income is completely uncoupled from your bank balance, which explains why partnership accounting feels like a hall of mirrors to the uninitiated.

The Mortgage Underwriting Nightmare: When Paper Profits Met the Underwriter

Let us look at how lenders handle this document because this is where the real panic sets in for self-employed borrowers. You walk into a bank expecting a red carpet because your K-1 shows a six-figure sum. Except that the underwriter does not care about your Box 1 numbers. They immediately flip to Fannie Mae Form 1084 or Freddie Mac Form 91 to calculate what they call stable monthly income.

The Two-Year Rule and the Hunt for Distributions

If you own less than 25% of the business, lenders generally consider you a passive investor. They will strictly look at the actual cash distributed to you over a consecutive 24-month period. Why? Because you lack the corporate control to force the company to pay you. If your K-1 shows $150,000 in ordinary business income but your cash distributions are a big fat zero, the lender will count your income from this source as exactly zero. We're far from it being an open-and-shut case of "income is income."

How Debt and Declining Revenues Can Evaporate Your Borrowing Power

What happens if you own 51% of that S-corporation? Now you are an owner. The bank will demand two years of full corporate returns (Form 1120-S). They will analyze the business liquidity, checking if the company can afford to keep paying you without draining its operational cash. If the business shows a net loss of $50,000 on Form 1040 Schedule E, that loss gets subtracted directly from your other income sources. Are you prepared to watch your spouse's steady W-2 income get devoured by your company's paper depreciation losses during a routine pre-approval check?

Guaranteed Payments vs Ordinary Business Income: The Hidden Nuances

Not all boxes on a K-1 are created equal, and treating them as a homogenous blob of money is a fast track to an audit or a loan rejection. For partners in a traditional partnership, Box 4 contains guaranteed payments for services. This is the closest a partner gets to a standard salary.

The Self-Employment Tax Sting of Box 4

Unlike ordinary business income, a guaranteed payment is paid to you regardless of whether the partnership made a profit or a loss that year. It is predictable. Lenders love it for that reason. Yet, the catch is that these payments are almost always subject to the full 15.3% self-employment tax (SECA), making them incredibly expensive from a tax perspective. Ordinary income from an S-corp, conversely, escapes this specific tax hit, which is why business owners fight tooth and nail to structure their payouts this way.

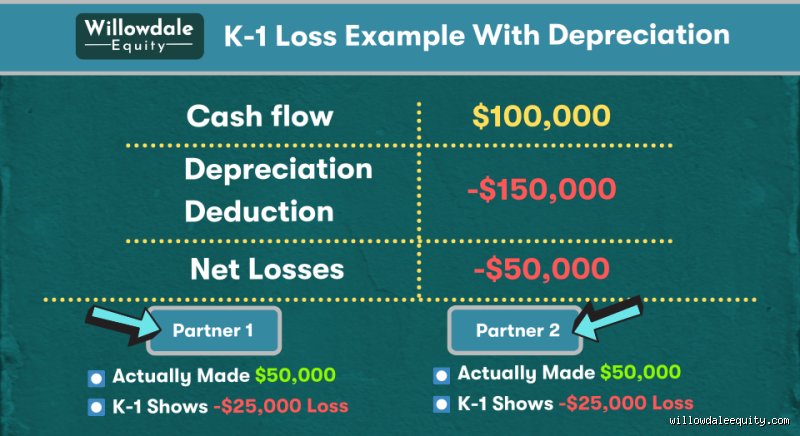

When Income Losses Become a Golden Tax Shield

Sometimes a K-1 shows a massive negative number. Thanks to strategies like Section 179 bonus depreciation, real estate syndicates routinely issue K-1s with large losses. To the untrained eye, it looks like a disaster. To a high-earning investor, it is a masterpiece because those losses might offset other passive income streams. Experts disagree on the long-term sustainability of using these paper losses to qualify for institutional leverage, but for tax mitigation, it is a classic play.

K-1 Income vs W-2 Wages: The Ultimate Battle for Liquidity and Proof

To truly grasp whether a K-1 counts as income, we must pit it against the gold standard of financial proof: the humble W-2. A W-2 is clean, verified by paystubs, and represents actual liquid currency deposited into a bank account. A K-1 is a lagging indicator, issued months after the tax year ends—often as late as the September 15 extended deadline—leaving a massive gap in your current financial timeline.

The Disastrous Timeline Gap for Real Estate Buyers

Imagine you are trying to buy a home in Denver in May 2026. You haven't filed your 2025 taxes yet because the partnership is on extension. The lender is looking at a 2024 K-1 that is nearly ancient history. In short: you are trapped in a bureaucratic limbo because your K-1 income cannot be verified with the same real-time precision as a simple Friday afternoon paycheck.