The Anatomy of a Schedule K-1 and Why the IRS Views It Differently

Tax season arrives, and you receive a document that looks vastly different from a standard W-2 or 1099. That is the Schedule K-1, an information return used to report your share of an entity's income, deductions, and credits. Unlike corporate structures that pay taxes directly, pass-through entities—think partnerships, S corporations, and limited liability companies—shift their entire tax burden directly onto the owners. But do not make the mistake of assuming all incoming money is treated equally.

The Pass-Through Illusion

People don't think about this enough, but receiving money is not the same as earning it through labor. When a partnership distributes cash to its investors, the IRS views this merely as a return on capital, similar to a stock dividend. In 2025, the distinction between active participation and passive investment determined billions in tax liabilities. If you just cut a check to a real estate syndicate in Austin, Texas, and sat back waiting for quarterly distributions, that K-1 reflects passive income. It cannot be used to fund a Roth IRA, nor does it face the 15.3% self-employment tax. That changes everything for casual investors who thought they were building a nest egg of qualifying retirement income.

S Corporations: A Unique Beast

The rules twist into a pretzel when we look at S corporations. If you own an S corp, say a boutique marketing agency based out of Chicago, your K-1 distributions are strictly non-earned income. Even if you work eighty hours a week! Yet, the IRS demands that you pay yourself a "reasonable salary" via a W-2, which *is* earned income. The remaining corporate profits pass through to your K-1 free of payroll taxes. Honestly, it's unclear why the system permits this massive loophole while hammering traditional partnerships, but that is the current landscape.

When a K-1 Unexpectedly Transforms Into Self-Employment Earnings

This is where the neat definitions break down. Sometimes, a K-1 does report income that counts as earned, specifically via Box 14, labeled Self-Employment Earnings.

The Active Partner Dilemma

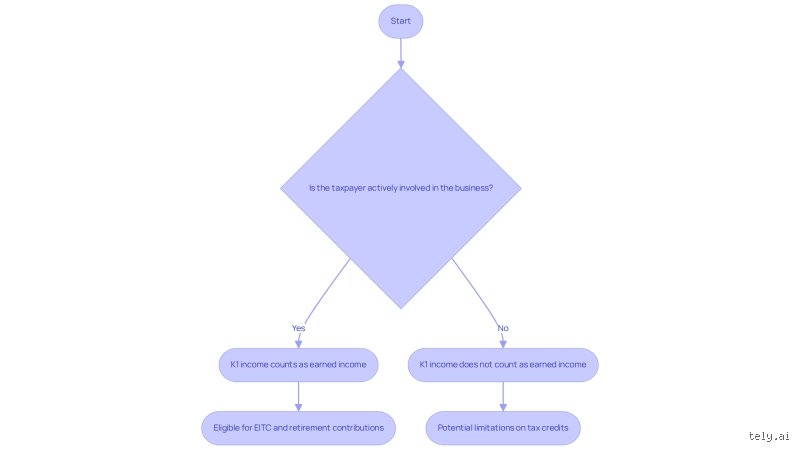

Are you a general partner who actually manages the day-to-day operations of the business? If so, your share of the ordinary business income from Box 1 of the K-1 is pulled down into Box 14. Suddenly, you are on the hook for self-employment tax. And because it is considered self-employment income, it miraculously qualifies as earned income for retirement account calculations. I have seen countless tech startup founders in Silicon Valley get blindsided by this because they assumed partnership distributions were always passive. The issue remains that your level of sweat equity dictates the tax classification, not just the name of the form you receive in the mail.

Guaranteed Payments: The Financial Substitute for a Salary

Partners do not get W-2s, except that they still need a regular paycheck to survive. Enter guaranteed payments, found in Box 4 of the K-1. Think of these as a hybrid between a salary and a partner draw. Whether the business makes a profit or loses its shirt during a tough quarter, the partnership owes you this money for your services or capital. For instance, if you manage a local medical practice in Miami and receive $120,000 in guaranteed payments annually, that specific amount is treated as earned income. You must pay self-employment taxes on it, but you can also use it to maximize your solo 401k contributions.

How Passive Loss Rules and Material Participation Alter the Equation

The IRS uses a complex framework known as material participation to separate the workers from the mere investors, a system established under Internal Revenue Code Section 469.

The Seven Tests of Material Participation

To prove your K-1 income should be treated as active—which has massive implications if the business is running a loss—you must pass one of seven distinct tests. The most common hurdle is the 500-hour rule. Did you spend more than 500 hours working for the entity during the tax year? If a restaurateur in New York opens a second location and hits 501 hours of management time, those losses or gains cease to be passive. Yet, if they only log 499 hours and have no other involvement, the IRS locks that income into the passive bucket. Which explains why keeping a meticulous, contemporaneous calendar log is the single most defensive move a business owner can make.

Comparing K-1 Classifications With Traditional Income Forms

To truly grasp why the question "does a K-1 count as earned income?" plagues accountants, we have to contrast it against the standard payroll ecosystem.

W-2 Versus K-1 Box 1

A W-2 is simple, predictable, and clean. You clock in, your employer withholds federal taxes, FICA, and Medicare, and the number in Box 1 is indisputably earned income. A K-1 Box 1 amount, conversely, is an accounting abstraction. It represents your slice of the company’s net taxable profit, regardless of whether you actually drew a single penny out of the business bank account! Imagine owing taxes on $50,000 of allocated profit when the partnership decided to reinvest all cash into new inventory, leaving you with zero liquidity to pay the bill. We are far from the safety of a standard paycheck here, as a result: you face phantom income that may or may not satisfy the criteria for retirement contributions depending entirely on your operational role.

Common Mistakes and Misconceptions Regarding K-1 Distributions

The Myth of the Blank Check

Many novice entrepreneurs assume every dollar landing in their bank account from a business entity behaves identically. It does not. You might receive a hefty distribution check from your S-Corporation and assume it qualifies for your IRA contribution. The problem is that the IRS views this movement of liquidity as a return on investment rather than sweat equity. Passive investment distributions never equal earned income for retirement calculation purposes. Confusion peaks when taxpayers see positive numbers in Box 1 of their Schedule K-1 and automatically assume it grants them IRA eligibility. It feels like money you worked for, yet the tax code remains completely indifferent to your feelings.

The General Partner Trap

Partnerships complicate this landscape exponentially. If you operate as a limited partner, your share of ordinary business income escapes self-employment tax. But does a K1 count as earned income under those exact circumstances? Absolutely not. Conversely, general partners face the exact opposite reality where their Box 14 figures trigger a 15.3% self-employment tax liability. We often see taxpayers trying to have it both ways by claiming the income is passive to avoid the Medicare levy, while simultaneously trying to use those same funds to back a maximum solo 401k contribution. You simply cannot bypass the tax and keep the benefit.

Misinterpreting Box 14 Metrics

Let's be clear about the mechanics of the Schedule K-1 paperwork. Box 14 is specifically designed to track self-employment earnings, which explains why auditing federal agents head straight for this section. A common oversight involves ignoring the specific alphanumeric codes attached to these amounts. Code A indicates net earnings from self-employment, which fundamentally alters how the IRS classifies your cash flow. If your accountant files without cross-referencing this code against your personal Form 1040 Schedule SE, you risk major compliance penalties.

An Advanced Strategy: Structuring for Maximum Advantage

The Dual-Status Framework

Savvy business owners refuse to leave their tax classification to chance. If you operate an entity taxed as an S-Corporation, you possess the unique ability to split your financial inflows into two distinct categories. You can pay yourself a reasonable W-2 salary which undeniably provides qualifying compensation for retirement accounts. The remaining corporate profits can then flow through as a distributions check. Is this approach complex? Yes, because determining what constitutes a reasonable wage requires analyzing strict industry benchmarks and geographic salary data. However, optimizing this ratio allows you to minimize payroll taxes while ensuring your legitimate retirement provisions remain fully funded.

Navigating the Material Participation Thresholds

To bend the rules of the partnership framework to your advantage, you must master the IRS material participation tests. If you log more than 500 hours of direct service for the entity within a single tax year, your passive status dissolves. As a result: your financial stake transforms into an active endeavor. This operational shift fundamentally changes how your pass-through losses and gains are treated on your individual return. It forces a recalculation of your adjusted gross income, which directly influences your legal capacity to shield wealth from the fiscal authorities.

Frequently Asked Questions

Does a K1 count as earned income for making traditional or Roth IRA contributions?

No, the baseline rule dictates that standard flow-through profit listed on a Schedule K-1 does not qualify as compensation for IRA purposes. The IRS requires matching W-2 wages or explicit net earnings from self-employment to legitimize a maximum $7,000 annual IRA contribution, or $8,000 for those over age fifty. If your document only displays numbers in Box 1 without corresponding data in Box 14, your contribution room sits at zero. Attempting to fund an account using ineligible passive distributions triggers a 6% annual excise tax penalty on the excess amount until corrected. Therefore, you must possess independent source wages to validate your retirement savings strategy.

Can I use my S-Corp Schedule K-1 ordinary income to qualify for the Child and Dependent Care Credit?

The statutory framework governing the Child and Dependent Care Credit strictly demands earned revenues to determine the specific dollar limits of your tax break. S-Corporation shareholders who do not draw a formal salary cannot use their corporate profit distributions to clear this legislative hurdle. Even if the business generates a net profit of $150,000 through your daily efforts, that specific figure remains classified as investment return rather than employment compensation on your personal tax return. To unlock the credit, which tops out at a maximum of $3,000 for a single qualifying dependent, you must establish a formal payroll infrastructure. Without a verified W-2, the IRS will automatically disallow the care credit during processing.

How does a guaranteed payment to a partner affect my earned income calculation?

Guaranteed payments represent a unique mechanism because they function as a hybrid between a salary and a profit share. When a partnership issues a guaranteed payment for services rendered, this specific sum is designated under Box 4 of the Schedule K-1. The IRS treats these payments as self-employment revenues, meaning they are subject to the standard 15.3% self-employment tax rate. Consequently, this specific subset of partnership revenue does satisfy the legal definitions of earned compensation. It allows you to safely fund retirement vehicles and access various family tax credits that passive investors are blocked from utilizing.

Strategic Verdict on Pass-Through Compensation

The intersection of partnership accounting and personal tax compliance is littered with expensive administrative traps. Relying entirely on a pass-through entity to generate retirement-eligible income without a deliberate payroll strategy is a recipe for fiscal disaster. We must reject the lazy assumption that all business revenue is viewed equally by federal auditors. The IRS will gladly penalize your retirement over-contributions while simultaneously collecting self-employment taxes on your misclassified general partnership distributions. If you want your business distributions to actively work for your long-term wealth strategy, you must implement a rigorous dual-status compensation system. Do not leave your financial definitions to chance when proactive corporate structuring solves the problem completely.