The Byzantine Maze of Schedule K-1 and Why It Terrifies Average Taxpayers

Let's strip away the corporate jargon for a moment. A Schedule K-1 is the IRS's way of ensuring that businesses structured as pass-through entities—think partnerships, S corporations, and limited liability companies—don't pay a dime of entity-level income tax. Instead, the profits, losses, deductions, and credits literally "pass through" the corporate firewall directly to you, the stakeholder. But people don't think about this enough: you are taxed on your allocated share of the profits, regardless of whether the business actually distributed a single dollar of cash to your bank account. It sounds fundamentally unfair, right?

Partnerships versus S Corporations: The Structural Chasm

Where it gets tricky is the structural DNA of the entity issuing the form. If you hold a stake in a general partnership or a typical multi-member LLC, your earnings are frequently subjected to both ordinary income tax and a heavy 15.3% self-employment tax for Social Security and Medicare. S corporations, however, play by vastly gentler rules. An S corp shareholder splits their income between a reasonable W-2 salary and a K-1 distribution, completely shielding that K-1 portion from the self-employment tax drain, which explains why so many mid-sized enterprises flee partnership structures the moment their revenue spikes past the $100,000 threshold. Yet, many founders botch the "reasonable salary" requirement, triggering aggressive IRS audits that reclassify distributions back into taxable wages.

The Phantom Income Trap That Ruins Holiday Budgets

Imagine owning a 15% stake in an Ohio-based manufacturing partnership that nets $500,000 in 2025. Your K-1 will boldly declare $75,000 of taxable income. But what if the managing partners decided to reinvest every single penny of that profit into a new warehouse facility in Columbus instead of cutting you a check? You still owe taxes on that $75,000. That changes everything for an unsuspecting investor who suddenly faces a five-figure tax bill with zero liquidity to pay it, a phenomenon seasoned accountants dryly refer to as "phantom income." Honestly, it's unclear why more boilerplate operating agreements don't mandate tax distribution clauses, but the issue remains that minority investors get burned by this omission every single spring.

Deconstructing Your K-1: The Line Items Driving Your Tax Percentage

Look at the form itself. It is a dense, confusing grid of boxes, each carrying a different tax destiny that collides with your personal tax bracket. Ordinary business income sits in Box 1, but as you move down the page, the IRS segments your earnings into distinct, isolated silos that cannot easily mix.

Ordinary Income Versus the Sanctuary of Capital Gains

Box 1 income is the workhorse, taxed at those standard progressive federal brackets topping out at 37% for high earners. But shift your eyes down to Boxes 9a and 9b, where net long-term capital gains and qualified dividends hide. These lines enjoy preferential tax treatment, maxing out at a 20% federal rate for individuals earning over $518,400 in single filer status, or even 15% for those comfortably nestled in the middle class. I argue that this bifurcated system is the single greatest wealth-generation tool in the American tax code, though populists routinely condemn it as an unfair loophole for the investor class. Why should active sweat equity be taxed at nearly double the rate of passive capital deployment?

The Real Estate Anomaly and the 25% Unrecaptured Section 1250 Trap

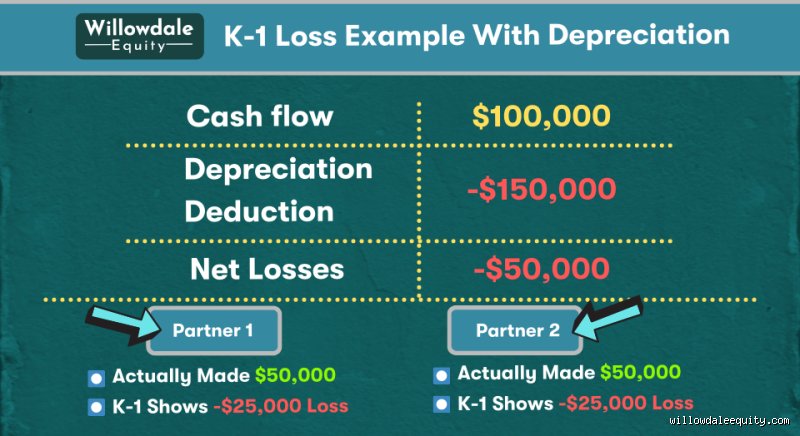

If your K-1 originates from a syndication or a commercial real estate fund—perhaps a multi-family complex in Austin purchased back in 2022—you will likely encounter Box 2, net rental real estate income. This area operates under its own physics. Thanks to non-cash depreciation deductions, your K-1 might actually show a net loss even while the property yields monthly cash flow. But wait. When that property eventually sells, the IRS demands its pound of flesh via the Unrecaptured Section 1250 depreciation recapture tax, which caps out at a flat 25% rate. It is a steep price to pay, except that savvy investors frequently dodge this bullet entirely by rolling their gains into a subsequent 1031 exchange, delaying the day of reckoning indefinitely.

Advanced Pass-Through Mechanics: The Hidden Add-Ons and Deductions

Determining how much tax do I pay on K1 requires factoring in more than just basic brackets. The modern tax code is a layering cake of penalties and bonuses that can radically alter your final liability.

The Qualified Business Income Deduction: A 20% Saving Grace

Enacted under the Tax Cuts and Jobs Act, Section 199A provides a massive silver lining known as the Qualified Business Income deduction. If your K-1 qualifies—and this is where the math gets incredibly dizzying due to phase-outs based on your total taxable income and whether you operate a Specified Service Trades or Businesses—you can deduct up to 20% of your pass-through business income right off the top. For an eligible business owner in the peak 37% bracket, this single provision can effectively slash their operational tax rate down to 29.6%. It is a massive win, but the rules are so convoluted that even veteran CPAs routinely disagree on which entities qualify for the full deduction.

The Quiet Assassins: Net Investment Income Tax and State Levies

But we're far from a simple deduction story. If you are a passive investor rather than an active manager in the business, your K-1 income could trigger the 3.8% Net Investment Income Tax once your modified adjusted gross income crosses the $200,000 mark for single filers. And let's not ignore state taxation. States like California or New York will happily tack on their own double-digit income tax rates, while others utilize Pass-Through Entity Taxes to let the business pay state taxes directly as a federal deduction, a brilliant workaround to the hated $10,000 SALT cap. Hence, a K-1 that looks cheap in Florida becomes an absolute nightmare if the partnership did business within the borders of Manhattan.

Comparing K-1 Taxation to W-2 and 1099 Income Streams

To truly understand how much tax do I pay on K1, it helps to contrast it against the familiar landscapes of traditional employment and freelance independent contracting.

The Structural Superiority Over W-2 Employment

A W-2 employee is trapped in a rigid cage. Taxes are withheld from every paycheck, and your ability to write off expenses against that income is essentially non-existent under current tax laws. Conversely, K-1 income arrives after the business entity has already deducted everything from corporate mileage to country club client dinners, drastically reducing the net taxable number before it ever touches your personal tax return. As a result: a dollar earned via a K-1 is often fundamentally cheaper from a tax perspective than a dollar earned on a corporate W-2, provided you have a skilled accountant steering the ship.

K-1 versus 1099-NEC: The Ultimate Freelance Showdown

When you receive a Form 1099-NEC as an independent contractor, you are viewed as a sole proprietorship. You face the full brunt of self-employment tax on every single dollar of net profit you generate. A K-1 from an S corporation, by comparison, allows for that exquisite separation of labor and capital. By splitting your income, you can legally avoid self-employment taxes on a massive chunk of your earnings, an option that a standard 1099 freelancer simply cannot access without restructuring their business. This structural arbitrage is precisely why wealthy operators rarely operate as simple freelancers, preferring instead the complex protective embrace of corporate pass-through entities.

Common mistakes and dangerous misconceptions

The phantom income trap

You received a piece of paper stating you made $50,000, yet your bank account remains stubbornly empty. How much tax do I pay on K1 when there is literally no cash in hand? You pay the exact same amount as if the money were sitting in your wallet. Partners frequently conflate accounting profit with actual cash distributions. The IRS does not care about your liquidity problems; they tax the underlying economic engine. If the business reinvested every single dollar into new machinery or real estate, your taxable liability remains unchanged. Because of this, unprepared investors often find themselves writing massive checks to Uncle Sam using personal savings just to cover the taxes on money they never actually touched.

Mishandling the basis calculations

Your tax basis is the invisible tether anchoring your investment to reality. Yet, it remains one of the most routinely butchered figures on modern tax returns. Every dollar of income increases your basis, while every distribution and loss drags it down. What happens if you claim a fat partnership loss without having enough basis to back it up? The IRS will summarily disallow it during an audit. The problem is that tracking this requires meticulous, year-over-year record-keeping that standard software rarely automates properly. In short, assuming your tax software magically knows your historical outside basis is a fast track to an aggressive audit notice.

The capital account hidden variable

The power of Section 199A and passive vs active status

Let's be clear: not all K-1 income is created equal. Your active participation determines whether your financial destiny involves a heavy self-employment tax burden or a beautifully sheltered stream of passive income. Active partners in a general partnership typically face an additional 15.3% self-employment tax on their distributive share. Conversely, limited partners generally escape this extra bite, but they face a different hurdle: passive activity loss rules. If the business bleeds cash, you can only offset those losses against other passive income streams. Except that the qualified business income deduction introduces a glorious loophole. Under Section 199A, eligible taxpayers can deduct up to 20% of their qualified business income directly from their taxes. This deduction completely recalibrates how much tax do I pay on K1, transforming what looked like a brutal tax bill into a highly manageable expense, provided you fall under the stringent taxable income thresholds ($182,300 for single filers or $364,600 for joint returns before phase-outs kick in).

Frequently Asked Questions

Do I have to file a tax return in every state where the partnership operates?

Yes, multi-state partnerships frequently trigger composite filing requirements or force individual partners to file non-resident state returns. If a fund operates across fifteen states, you might suddenly owe compliance fees in jurisdictions you have never even visited. Many partnerships offer a composite return option where they pay the state-level tax on your behalf at the highest marginal rate, which usually sits around 5% to 13.3% depending on the state. While this slashes your administrative headache, it often means you overpay compared to filing individually. As a result: you must carefully weigh the cost of hiring a CPA to file twelve separate state returns against the raw financial loss of the high composite tax rates.

Why is my Schedule K-1 always arriving so late in the year?

Partnerships must aggregate data from dozens of internal sources, which explains why they almost universally utilize the automatic six-month filing extension. While standard corporate forms land in your mailbox by February, a complex K-1 rarely materializes before July or August. The issue remains that your personal Form 1040 is still due on April 15th, forcing you to file an extension based on rough estimates. Did you know that an extension to file is absolutely not an extension to pay? You must project your liability perfectly or face interest penalties on the shortfall when you finally compute exactly how much tax do I pay on K1 later in the year.

Can a K-1 form show negative numbers and how do they affect my taxes?

Negative numbers indicate ordinary losses, capital losses, or foreign tax deductions that can potentially lower your overall tax obligations. But can you actually use them right away? If you are an active owner, these losses can generally offset your other ordinary income, like W-2 wages or investment dividends, up to certain excess business loss limits. For passive investors, those numbers simply enter a state of suspended animation (known as suspended passive losses) until the partnership generates profit or you sell your entire stake. It is a frustrating game of financial chess where your immediate tax relief is entirely held hostage by the rigid structure of your initial investment contract.

A definitive verdict on pass-through taxation

Stop treating your Schedule K-1 like a standard tax document because it is actually a highly sophisticated legal instrument disguised as an IRS form. The absolute obsession with minimizing the immediate tax bill causes too many investors to ignore the long-term structural damage of eroded basis. We must collectively abandon the naive delusion that pass-through entities offer a simple, frictionless path to wealth accumulation without administrative pain. If you choose to play in the arena of partnerships, S-corporations, or complex master limited partnerships, you are willfully choosing complexity. Pay the premium for specialized human intelligence instead of trusting basic consumer tax software to navigate these waters. Ultimately, the true cost of your K-1 is never just the percentage you write on the check to the government; it is the mental bandwidth consumed by managing the structural reality of pass-through mechanics.