Deconstructing the billion-dollar startup ecosystem: what constitutes a unicorn today?

The mechanics of arbitrary valuation thresholds

To truly grasp why certain sectors breed these entities like rabbits, we need to strip away the romantic venture capital mythology. A private tech enterprise crossing a one-billion-dollar post-money valuation via institutional financing rounds sounds precise, yet the thing is, these metrics are often engineering marvels cooked up by aggressive boardrooms. Founders negotiate complex liquidation preferences and ratchets with late-stage financiers, pushing paper valuations into the stratosphere while masking real underlying operational health. The criteria are technically uniform across the globe, but a software-as-a-service firm hitting this mark in the Silicon Valley ecosystem behaves entirely differently than an asset-heavy logistics player operating out of Bangalore or Shanghai. Honestly, it's unclear whether half of these valuations would survive a sudden macroeconomic freeze or a forced public offering, yet this remains our primary metric for benchmarking generational innovation.

The shifting hierarchy of decacorns and hectocorns

As the global registry of privately held tech giants swells past 1,700 entities, the traditional yardstick has lost some of its luster. We have been forced to invent new tiers because the top tier of hyper-growth firms has completely outgrown the original baseline. Enterprises crossing the ten-billion-dollar milestone are now routinely tagged as decacorns, while a rarified group of entities valued above one hundred billion dollars—such as the generative AI pioneer OpenAI or Elon Musk’s aerospace giant SpaceX—occupies the hectocorn tier. This stratification matters immensely because the operational velocity required to move from a single billion to ten billion depends entirely on the addressable market of the host sector. Some fields have a natural ceiling; others appear totally limitless.

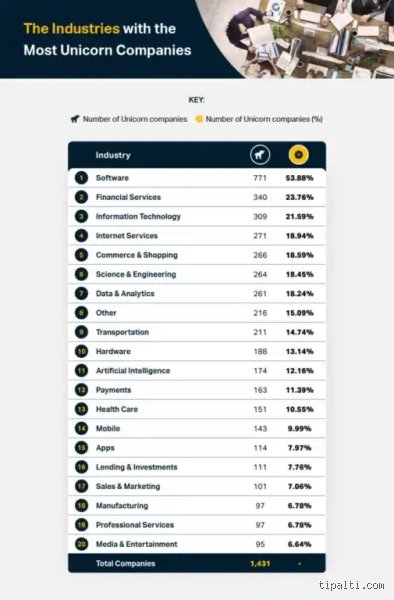

The reigning champion: enterprise software dominates the global startup tracker

Why business-to-business models scale with terrifying efficiency

There is a prevailing cultural narrative that the most successful ventures are those sitting on the home screens of our smartphones. We are far from it. If you scrub the raw data compiled by international database authorities like CB Insights, enterprise software consistently claims the highest absolute count, capturing roughly 15.7% of the total global private market pool. Why does corporate infrastructure crush consumer-facing tech so convincingly? The answer lies in the beautiful, predictable monotony of contract-based recurring revenue. When a venture sells cloud database tools or developer platforms, they lock clients into multi-year enterprise agreements with high switching costs.

Consider the data storage giant Databricks, a powerhouse headquartered in San Francisco that commanded a mind-boggling private valuation of $134 billion following its late-2025 internal adjustments. Businesses cannot simply unplug their core data pipelines because a cheaper alternative pops up next month. This immense stickiness allows corporate tech ventures to maintain high gross margins—frequently hovering above 80%—which makes them the ultimate darlings of growth equity firms. It is an environment where predictability breeds immense premium multipliers.

The structural mechanics of enterprise software saturation

Where it gets tricky is analyzing the sheer diversity tucked inside this single umbrella category. We are not just talking about basic human resources software or generic project management tools here. The modern B2B venture ecosystem is heavily weighted toward hyper-specialized cloud security architecture, data governance frameworks, and developer operations tools. Every single old-world corporate entity on the planet is currently undergoing some flavor of digital overhaul, which explains the endless demand for these underlying software layers. It requires far less capital to scale a software platform to a billion-dollar run rate than it does to build a global physical delivery network or clear strict medical regulatory hurdles. Consequently, institutional money flows down the path of least resistance, minting software firms at a clip that physical product industries simply cannot match.

The disruptive contenders: artificial intelligence and fintech battle for the crown

The unprecedented acceleration of generative machine learning platforms

If enterprise software is the steady king of the mountain, artificial intelligence and machine learning represent the volatile, rocket-fueled challenger aiming for the throne. The speed at which machine learning ventures are reaching ten-figure status has completely shattered historic venture capital playbooks. Look at Anthropic, which managed to secure multi-billion-dollar commitments from major tech conglomerates within a staggering eight months of launching its core models. According to industry tracking data from April 2026, the AI and machine learning sector now commands approximately 9.0% of the active global registry, boasting a velocity that makes older software verticals look positively arthritic. Investors are completely bypassing traditional revenue-to-valuation multiples, frequently pricing these entities based on raw compute capacity and the academic pedigree of their research teams. But is this sustainable, or are we witnessing a massive capital allocation anomaly driven by pure FOMO? Most independent analysts disagree sharply on the terminal value of these foundational models, creating a fascinating schism at the top of the market.

Financial technology maintains its systemic market footprint

Despite experiencing a brutal valuation correction during the high-interest-rate cycles of recent years, financial technology refuses to yield its position near the top of the global sector distribution. The segment remains anchored by generational titans like payment infrastructure provider Stripe—holding strong at a post-money valuation of $159 billion—and European digital banking pioneers like Revolut, valued at $75 billion. Fintech thrives because it directly sanitizes and extracts a toll from the global movement of money. The sector splits neatly into distinct sub-pockets: payments, neo-banking networks, automated lending engines, and decentralized ledger platforms. Because these companies plug directly into the transactional bloodstream of global commerce, their scaling architecture is incredibly linear; more transactions equals more top-line revenue, which changes everything for an analyst looking at operational longevity.

A comparative analysis of sectoral mechanics and capital velocity

Contrasting the underlying dynamics of the top three industries

To really appreciate how these distinct sectors create outsized private corporate value, we have to look directly at the unit economics that drive their growth trajectories. The financial profiles of enterprise software, artificial intelligence, and financial technology could not be more divergent, yet they all arrive at the same destination of ten-figure capitalization. We can unpack their distinct structural differences by mapping out their core operational realities side-by-side.

| Core Evaluation Metric | Enterprise Software (SaaS) | Artificial Intelligence (AI/ML) | Financial Technology (Fintech) |

|---|---|---|---|

| Average Gross Margin Profile | 75% to 85% | 40% to 60% (High Compute Costs) | 60% to 70% (Toll-booth Model) |

| Primary Capital Sink | Enterprise Sales & Marketing Teams | Raw GPU Infrastructure & Specialized Talent | Regulatory Compliance & Capital Reserves |

| Median Time to Reach $1B Status | 7.2 Years | 3.4 Years | 5.9 Years |

| Dominant Regulatory Headwinds | Data Localization and Privacy Laws | Copyright Injunctions and Safety Mandates | Anti-Money Laundering (AML) Protocols |

The hidden friction points that data tables leave behind

The issue remains that numbers on a chart do not capture the operational friction experienced on the ground. A software company can cruise along smoothly on standard Amazon Web Services instances, whereas an AI pioneer is constantly bleeding cash to secure cutting-edge semiconductor hardware. People don't think about this enough: the capital intensity of training massive neural networks means that an AI venture might raise half a billion dollars just to keep its research servers humming for twelve months. As a result, its true capital efficiency is drastically lower than a boring B2B accounting software company that grew organically via disciplined enterprise sales teams. Hence, looking solely at market caps and funding round announcements gives you an incomplete view of systemic sector health.

Common Mistakes and Misconceptions About Tech Titan Ecosystems

People look at the venture capital landscape and instantly assume that consumer-facing applications drive the highest volume of billion-dollar valuations. They see ride-hailing apps or trendy delivery services daily. They mistake visibility for volume. Fintech and enterprise software routinely crush consumer apps in total valuation metrics, yet the public remains obsessed with viral social media platforms.

The Valuation Trap of Paper Wealth

Why do we fall for this? Because a flash billion-dollar valuation on paper feels like a done deal. The problem is that paper wealth does not equal liquidity. Many observers fail to realize that late-stage funding rounds frequently include heavy liquidation preferences that protect investors but artificially inflate the headline price tag. Which industry has the most unicorn startups? If you only count companies with sustainable, cash-generative operational metrics rather than those propped up by complex financial engineering, the leaderboard shifts dramatically away from speculative Web3 projects and back toward boring, predictable Software-as-a-Service (SaaS) enterprises.

Misreading Geography as Destiny

Another classic blunder is assuming Silicon Valley holds a permanent, unassailable monopoly on these elite private entities. It is a comforting myth for Western tech purists. Let's be clear: while California remains an absolute powerhouse, the geographical distribution of massive tech valuation events has decentralized radically. European climate-tech firms and Asian logistics networks are capturing massive market shares. If you restrict your strategic horizon to just one valley, you miss the systemic global shifts rewriting the valuation rulebooks.

The Hidden Leverage of B2B Infrastructure

Everyone wants to talk about artificial intelligence chatbots, but nobody wants to talk about the data plumbing that keeps those chatbots online. That is where the real wealth concentrates. Unspectacular infrastructure software consistently breeds more private market value than flashy front-end systems.

The Compound Interest of B2B SaaS

Consider the sheer resilience of enterprise subscriptions. A consumer can cancel their streaming app during a minor personal budget crunch. A multinational corporation cannot simply unplug its cybersecurity defensive perimeter or its core cloud database architecture without triggering catastrophic operational failure. This extreme stickiness generates predictable, recurring revenue streams that venture capitalists happily overpay for. As a result: B2B infrastructure providers command premium valuation multiples that consumer brands could only dream of achieving. You cannot build a shiny digital economy without digging the digital trenches first.

Frequently Asked Questions

Which industry has the most unicorn startups globally today?

Fintech firmly holds the crown, accounting for over 20% of the global unicorn population with enterprise software-as-a-service trailing closely behind. Data from recent market indexes shows that financial technology firms command an aggregate valuation exceeding $1 trillion. This dominance persists because these platforms monetize transaction flows directly rather than relying on fickle digital advertising models. Stripe and Revolut serve as prime examples of this lucrative dynamic. The issue remains that sector boundaries are blurring as every company slowly integrates embedded banking elements into their core software offerings.

How long does it take an average startup to reach a billion-dollar valuation?

The historical trajectory required roughly seven to eight years of aggressive operational scaling for an enterprise to hit the ten-figure mark. However, artificial intelligence enterprises are currently obliterating this traditional timeline by achieving elite status in less than three years. OpenAI and Anthropic catalyzed this paradigm shift, driven by unprecedented capital inflows from massive corporate tech syndicates. But is this hyper-accelerated timeline actually healthy for long-term market stability? Which industry has the most unicorn startups depends entirely on whether these accelerated AI firms can actually sustain their massive operational costs over a decade.

What percentage of these highly valued private companies actually fail?

Data indicates that approximately 90% of all venture-backed startups fail, and even those reaching the billion-dollar threshold are not immune to spectacular collapses. Historical analysis of post-2020 market corrections reveals that nearly one in five elite private firms eventually undergoes a down-round or files for restructuring. We saw this stark reality play out with high-profile flameouts like WeWork and various overhyped electric vehicle ventures. In short, a private valuation of ten figures acts as a lagging indicator of investor enthusiasm rather than a guarantee of permanent fiscal viability.

The New Reality of Private Capital Markets

The obsession with tracking which industry has the most unicorn startups obscures a much harsher economic reality. We have exited the era of cheap, abundant capital where raw growth metrics excused horrific capital burn rates. Investors no longer tolerate businesses that burn fifty million dollars a month just to acquire market share that vanishes the moment subsidies stop. The future belongs exclusively to capital-efficient platforms that solve genuine infrastructure bottlenecks rather than creating artificial consumer conveniences. (We all know deep down that another food delivery app won't save humanity anyway.) Focus your attention on the unglamorous layers of industrial software, automated logistics, and defensive cybersecurity. Those are the sectors that will dictate the next decade of macroeconomic dominance because they build the actual foundation upon which the rest of the digital world operates.