The Anatomy of the Great Lithium Rebound: Shifting from Glut to Deficit

To understand where the market is going, you have to look at the wreckage of where it has been. Between 2022 and 2024, the lithium market was defined by a staggering wave of excess supply. A reckless surge of new production, driven predominantly by high-cost lepidolite operations in China and aggressive hard-rock spodumene expansions in Australia, flooded the market exactly as short-term electric vehicle growth temporarily cooled. According to historical tracking from Fastmarkets, the global market surplus peaked at an astonishing 175,000 tonnes of Lithium Carbonate Equivalent (LCE) in 2023, remaining heavily elevated at 154,000 tonnes through 2024. Predictably, this massive inventory mountain absolutely crushed regional spot prices, which plummeted by more than 80% from their historic peaks to bottom out at a miserable $8,259 per tonne in June 2025.

The Extraction Economics Behind the 2026 Supply Contraction

Mining economics always dictates the exact same response: when spot prices drop below the marginal cost of production, operators blink. And blink they did, which explains the violent structural reversal currently playing out across the globe. Throughout 2025, major Chinese chemical refiners aggressively curtailed capacity, while early-stage junior explorers completely slashed their development budgets. The surplus began shrinking rapidly, narrowing to 141,000 tonnes LCE late last year, but 2026 marks the definitive, hard pivot. Where it gets tricky is that a consensus has formed among the world's largest financial institutions that the market is careening toward a severe deficit, yet the exact magnitude remains a moving target. For instance, Fastmarkets models a conservative deficit of 1,500 tonnes LCE, UBS estimates a deeper 22,000-tonne shortfall, and Morgan Stanley has come out with an aggressive projection of an 80,000-tonne structural lithium deficit for the year 2026.

Geopolitical Interventions and the Death of Low Prices

As the old commodity maxim goes, low prices are the ultimate cure for low prices. But people don't think about this enough: government intervention is now artificially magnifying the upswing. Take Zimbabwe’s sweeping raw lithium export restrictions introduced earlier this year, or the ongoing regulatory delays surrounding Contemporary Amperex Technology’s (CATL) massive Jianxiawo lepidolite mine in China. By removing thousands of tonnes of projected feedstock from the global pool, these bottlenecks have injected a heavy risk premium into the physical market. Spot battery-grade lithium carbonate prices in China have already staged a remarkable comeback, surging from their 2025 lows to climb above $24,086 per metric ton in early 2026, while Northeast Asian refined lithium metal reached $18.82 per kilogram by May 2026. Honestly, it’s unclear whether prices will steadily hold these gains or violently overshoot toward $30,000 per tonne, because markets are inherently emotional, forward-looking mechanisms.

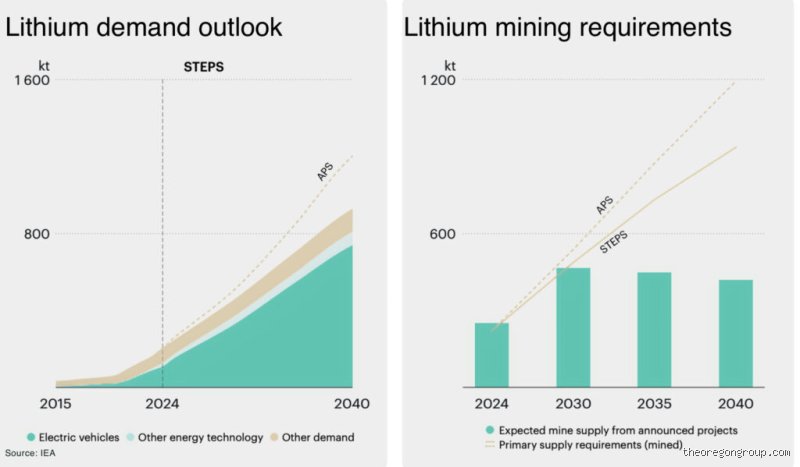

Technical Catalysts Driving the Demand Surge in 2026

The entire demand narrative has fundamentally transformed, and that changes everything. While the mainstream financial press spent the last two years obsessing over a supposed cooling in the automotive transition, the underlying data reveals a completely different reality. Global electric vehicle consumption didn't stop; it grew by a resilient 22% in 2025, continuing to devour roughly 70% of global lithium output. But the real structural wild card for 2026 isn't just cars. It is the unprecedented, explosive expansion of stationary energy storage systems (ESS) tied directly to solar and wind grids, alongside a booming industrial interest in utility-scale backup batteries for AI-driven data hubs.

Stationary Energy Storage Systems Form the New Demand Floor

The grid storage sector has evolved into the definitive swing factor capable of tightening global commodity balances independently of automotive manufacturing. In 2025, global demand for lithium-ion chemised batteries in storage applications skyrocketed by 71%, and analysts widely project another blistering 55% jump through 2026. This means stationary storage now commands nearly a fifth of total global lithium demand. Look at the sheer scale of the deployment: hedge funds like Arcane Capital Advisors note that standard market models are drastically underestimating this segment because renewable energy integrations are compounding exponentially. They project global battery energy storage system capacity to scale toward 1.5 to 2.5 Terawatt-hours by the end of the decade. Because massive solar fields require massive chemical buffers to handle peak loads, the lithium procurement race has expanded far beyond the traditional auto corridors of Detroit and Stuttgart.

Heavy-Duty Fleet Electrification Compounds Procurement Pressure

And then there is the heavy transport sector, an absolute glutton for raw battery materials. An electric class-8 commercial semi-truck requires a battery pack that is up to ten times the size of a standard passenger sedan, meaning even minor upticks in fleet adoption exert massive leverage on upstream chemical miners. During the prolonged market downturn of 2024, dozens of logistics companies quietly finalized their pilot programs. In 2026, those commercial rollouts are going live across North America and Europe, adding a steady, incremental 10% demand pressure directly onto a tightening supply chain. When a single heavy transport vehicle can consume as much lithium as a small neighborhood of passenger vehicles, a localized supply chain squeeze becomes almost mathematically inevitable.

Macroeconomic Volatility and Sovereign Stockpiling Strategies

We are no longer operating in a pure free-market commodity ecosystem; instead, lithium has been pulled into the broader debasement trade and the realm of national security. Western governments have finally woken up to the fact that a complex lithium mine takes an average of 16.7 years to build from initial discovery to commercial production. As a result, industrial policy is shifting away from simple trade tariffs and directly into sovereign buffering mechanisms, transforming how critical minerals are priced on the global stage.

Project Vault and the Institutionalization of Lithium Reserves

The ultimate proof of this paradigm shift arrived in early February 2026, when the United States government launched "Project Vault", a landmark $12 billion public-private strategic mineral stockpile. Structured with $1.67 billion in private capital and a massive $10 billion loan facility from the U.S. Export-Import Bank, this initiative is explicitly designed to aggressively procure and store strategic reserves of battery-grade lithium carbonate and hydroxide. Think of it as the modern equivalent of the Strategic Petroleum Reserve. By entering the open market as a massive, price-insensitive institutional buyer, the U.S. government has effectively established a hard pricing floor for domestic and geopolitical partners. You simply cannot expect prices to drift back toward historical lows when sovereign states are actively printing capital to hoard physical tonnage for national security purposes.

The Fragility of Late-Stage Project Financing

Yet, the physical reality on the ground remains incredibly stubborn. During the depths of the 2024 commodity winter, the number of definitive feasibility studies for greenfield projects plummeted from dozens annually to fewer than ten globally. Mining companies slashed their capital expenditure budgets, walked away from junior joint ventures, and put early-stage hard-rock discoveries on ice. Because of that multi-year investment freeze, the supply pipeline for the late 2020s is fundamentally broken. Even if rising lithium spot prices through 2026 spark a frantic capital response from Wall Street and Bay Street, the physical commissioning of a chemical processing plant cannot be achieved overnight. Restoring a mothballed spodumene operation or stabilizing a brine evaporation pond can easily chew through 12 to 24 months of rigorous engineering work before a single gram of battery-grade material is produced.

Alternative Chemistries: Threat or Distraction to the Lithium Bull Thesis?

No serious analysis of the lithium market can ignore the loud chorus of skeptics pointing toward alternative battery chemistries as an existential threat to long-term demand. The most frequent challenger brought up is the rapid commercialization of sodium-ion technology, a chemistry that completely bypasses lithium in favor of abundant, dirt-cheap rock salt. This development has led plenty of macro-bearish commentators to argue that alternative chemistries will inevitably cap any potential lithium price rally in 2026. My view? I suspect this narrative is a massive near-term distraction that completely misjudges the brutal realities of industrial manufacturing scaling.

Sodium-Ion and Solid-State Realities in 2026

Let's be perfectly clear about the technical trade-offs at play: sodium-ion batteries are an elegant solution for low-range, urban micro-vehicles or stationary stationary grid storage where physical weight is entirely irrelevant. However, their energy density is fundamentally inferior to high-nickel lithium chemistries. A standard sodium-ion cell simply cannot deliver the necessary range required for a premium long-range crossover vehicle or an interstate electric truck. Consequently, while sodium-ion may successfully carve out a niche at the bottom of the stationary market, it acts as a relief valve rather than a true replacement. The issue remains that the high-performance automotive sector remains completely wedded to lithium-based architectures for the foreseeable future. Meanwhile, highly touted solid-state batteries—which are supposed to revolutionize safety and density—actually require up to an estimated 30% more lithium metal per cell than their traditional liquid-electrolyte predecessors, completely flipping the bearish substitution argument entirely on its head.

Common mistakes and misconceptions

The single-commodity illusion

Investors frequently treat the white gold market as a monolith. Except that it is not. You cannot simply look at a single price index and assume you understand the entire picture. The reality reveals a fragmented landscape divided by localized logistics, strict purity requirements, and distinct chemical variants. Spodumene concentrate from hard-rock mining requires completely different processing timelines than the underground brines found in South America. If you track only raw lithium carbonate, you miss the explosive premium currently building up around high-purity, battery-grade lithium hydroxide monohydrate.The EV-only demand trap

Are you assuming that electric car manufacturing is the sole engine driving this entire market? Let's be clear: this narrow focus is an outdated analytical blunder. While passenger vehicles remain massive consumers, the actual narrative has evolved violently due to a massive structural shift. Grid stabilization initiatives and massive battery backups for global artificial intelligence infrastructure are changing everything. This alternative sector has rapidly escalated its footprint, expanding from a minor single-digit share to a massive chunk of total global allocation.Ignoring the hidden inventory pipeline

Another typical mistake involves looking exclusively at visible warehouse stocks. Traders routinely celebrate sudden inventory drawdowns while completely overlooking the massive, opaque stockpiles held domestically within Chinese processing hubs. This off-book material frequently dampens spot market rallies when prices begin to climb. Relying solely on official Exchange data creates a false sense of immediate scarcity. ---Little-known aspects and expert advice

The geopolitics of the hidden midstream

Mining the raw mineral is merely the first step. The real choke point lies in the highly specialized chemical refining sector. China currently controls the vast majority of global conversion capacity, creating a severe bottleneck that mining permits elsewhere cannot solve. Even if Western jurisdictions successfully fast-track new extraction facilities, the physical capacity to transform raw ore into battery-compliant chemicals remains intensely centralized. This bottleneck creates an artificial supply lag that keeps localized spot prices highly volatile.The strategic stockpile wild card

A crucial factor overlooked by casual retail investors is the emergence of sovereign buffer funds. A prime example occurred recently with the introduction of Project Vault, a massive multi-billion public-private initiative backed by a massive ten-billion-dollar loan mechanism. This program explicitly aims to establish a domestic strategic lithium reserve to insulate local supply chains from international shocks. When governments enter the spot market to build permanent stockpiles, historical pricing models based strictly on commercial corporate demand become entirely irrelevant."The rapid financialization of lithium through specialized futures contracts means that speculative capital can detach spot prices from physical supply realities for extended periods."---