The Anatomy of Suspense: What Is This Form and Why Does It Arrive So Late?

People don't think about this enough, but Schedule K-1 is essentially an information slip that acts as a financial mirror. It reflects your specific, sliced-up share of a business or estate's income, deductions, credits, and losses. The document comes in three distinct flavors: Form 1065 for partnerships and multi-member LLCs, Form 1120-S for S-corporations, and Form 1041 for beneficiaries of trusts and estates. Because these larger entities must calculate their entire corporate financial picture before they can divide the spoils among owners, you often won't see your K-1 until late March or even deep into September. That changes everything for your personal timeline.

The Pass-Through Magic (And Its Dark Side)

Why do we tolerate this administrative headache? The answer lies in the avoidance of double taxation. When a traditional C-corporation makes money, Uncle Sam taxes the profit at the corporate level, and then taxes you again when those profits land in your brokerage account as dividends. Pass-through entities bypass that first toll booth entirely. Yet, the issue remains that you are taxed on your share of the profits regardless of whether you actually received a single dollar of cash distribution in your bank account. Can you imagine paying taxes on 50,000 dollars of income you never actually touched? It happens every single year to minority shareholders in family businesses.

The Compliance Lag and the Extension Trap

Here is where it gets tricky for individual taxpayers trying to meet the traditional April 15 deadline. Because partnership returns are due on March 15, and those entities frequently request a six-month extension, you might find yourself waiting indefinitely for the paperwork. As a result: filing a Form 4868 to extend your personal return becomes less of a choice and more of a mandatory rite of passage. I strongly believe that relying on estimated K-1 numbers is a fool's errand that guarantees amended returns and endless correspondence with tax authorities. Expecting a smooth April filing when you own a piece of a hedge fund or a real estate syndicate is just wishful thinking; we're far from that reality.

Cracking the Code: The Mechanics of How Do I Report K-1 on My Tax Return

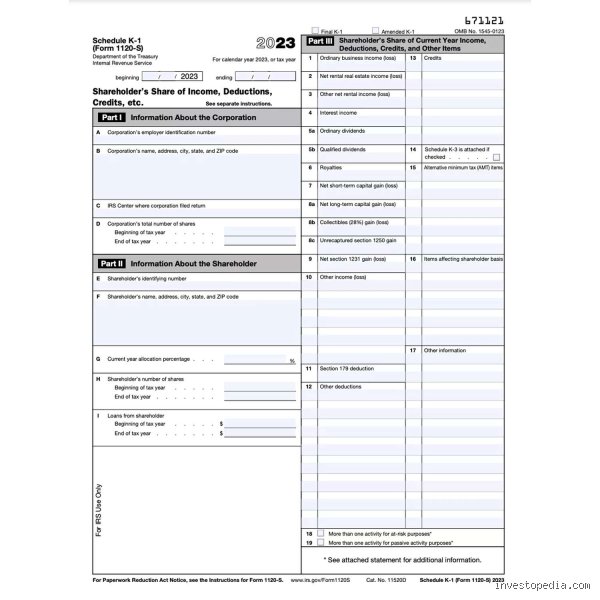

Let's map the physical journey of these numbers because navigating the boxes requires precision. For a standard partnership K-1, Box 1 shows your ordinary business income or loss, which does not just magically appear on line 1 of your Form 1040. Instead, it travels first to Schedule E, Part II (Supplemental Income and Loss), where it sits alongside other passive or non-passive activities. If your K-1 shows net rental real estate income in Box 2, that requires a completely different treatment, potentially triggering passive activity loss limitations under Section 469 of the Internal Revenue Code. It is a highly fragmented process.

Deciphering the Boxes: From Line 1 to the Deep Sub-Schedules

Every box on that form represents a different tax flavor. Box 5 contains your interest income, while Box 6a holds your ordinary dividends. Do these stay on Schedule E? Absolutely not. They must be extracted and manually placed onto Schedule B (Interest and Ordinary Dividends), meaning a single K-1 can splinter across four or five distinct sections of your personal return. Look at Box 9a for net long-term capital gains, which must march over to Schedule D (Capital Gains and Losses). The system expects you to act as a sorting mechanism, disassembling the K-1 piece by piece and scattered across the 1040 landscape.

The Crucial Separation of Passive versus Non-Passive Activities

This is where most DIY filers completely wreck their returns. The IRS cares immensely about whether you materially participated in the business operations. If you are a silent investor who put money into a trendy restaurant in Austin, Texas back in 2024 but never flipped a burger or managed the books, your income is passive. Why does this distinction matter so much? Because passive losses can generally only offset passive income. If that Austin restaurant threw off a 12,000 dollar loss, you cannot use that loss to wipe out your W-2 wage income, except that it gets suspended and carried forward to future years—a nuance that catches thousands of taxpayers off guard every season.

The Phantom Income Conundrum: Distinguishing Distributions from Taxable Allocations

We need to talk about the psychological shock of the discrepancy between Box 1 and your actual bank deposits. Consider a concrete example: imagine you own a 10 percent stake in a manufacturing partnership called Wolverine Components based in Grand Rapids, Michigan. In 2025, the company did incredibly well and allocated 85,000 dollars of ordinary income to you, which is proudly displayed in Box 1. However, the managing partners decided to reinvest most of the cash back into new machinery, distributing only 15,000 dollars in actual cash to you to help cover your tax liability. You are legally required to report and pay income tax on the full 85,000 dollars.

Tracking Your Basis or Risking Double Taxation

To avoid losing your mind over this phantom income, you must maintain an immaculate record of your tax basis. Your basis is essentially your financial skin in the game. Every dollar of income you are allocated but do not receive increases your basis; conversely, every cash distribution you pull out reduces it. If you fail to track this metric—which is notably not always calculated for you by the partnership—you run the very real risk of paying tax on that same money again when you eventually sell your ownership stake. Frankly, experts disagree on the most foolproof way to track basis outside of sophisticated enterprise software, leaving everyday investors in a precarious spot.

Alternative Pathways: Electronic Imports versus Manual Data Entry

When thinking about how do I report K-1 on my tax return, you face a technological fork in the road. Modern tax software packages promise seamless electronic importing via PDF parsing or direct partner portals. It sounds beautiful in theory. In practice, however, these automated systems regularly misinterpret the complex footnotes and supplemental statements attached to the back of the K-1, especially those concerning Section 199A Qualified Business Income (QBI) deductions. Manual data entry, while tedious enough to make you question your life choices, forces you to review every single code in Box 20 individually.

The Nightmare of Box 20 Codes and Supplemental Disclosures

The real teeth of a Schedule K-1 are often hidden on the second page or within the statement attachments, typically triggered by Box 20 on a Form 1065 or Box 17 on a Form 1120-S. These alphanumeric codes indicate everything from state-specific adjustments to advanced alternative minimum tax calculations. For instance, Code V in Box 20 usually signals information needed to compute your QBI deduction, providing a potential 20 percent haircut on your taxable business income. Missing a single code or failing to enter the accompanying spreadsheet data means you are actively leaving money on the table or, worse, triggering an automated underreporter notice from the IRS computer systems in Austin or Cincinnati.

Common mistakes and misconceptions with your Schedule K-1

Taxpayers routinely blunder into the trap of assuming that the figures on this form mirror actual cash distributions received during the fiscal year. They do not. Partners often panic when discovering they owe taxes on phantom income, which represents profits retained by the entity for operational growth rather than distributed to owners. Let's be clear: your tax liability is tied directly to your distributive share of the entity’s net earnings, completely independent of whether a single dollar landed in your personal checking account. If the business generated a profit but chose to reinvest every cent into new machinery, you still face the obligation to report K-1 on my tax return and pay the resulting tax bill.

The passive loss limitation trap

Another frequent oversight involves the blind deduction of losses without examining the strict material participation rules enforced by the IRS. Unless you spent more than 500 hours actively managing the operations of the partnership, the agency classifies your share of losses as passive. The problem is that passive losses cannot offset your ordinary W-2 wage income or active business profits. They are strictly bottlenecked. You can only use them to counteract passive income from other investments, meaning an unexpected loss on Box 1 of Form 1065 might sit stranded on your tax return as a suspended loss for years. Why do investors continuously assume all business losses are immediately deductible against their salary? The issue remains that the tax code divides income into distinct, non-communicating silos, forcing you to carry forward those net operating losses to future tax cycles using Form 8582.

Ignoring the outside basis calculation

Failing to track your adjusted basis represents a catastrophic error that eventually triggers an audit. Your initial investment plus allocated income increases this baseline, while distributions and allocated losses reduce it. Except that the partnership itself does not track this individual metrics for you on the document. If your basis drops to zero, any subsequent cash distribution switches from a tax-free return of capital into a immediate capital gain. Furthermore, you are legally forbidden from deducting losses that exceed your total at-risk basis, which explains why maintaining an independent, multi-year ledger of your capital account is mandatory for survival.

The capital account blind spot and expert strategy

The IRS mandate requires partnerships to report partner capital accounts using the strict transactional transactional basis of tax basis accounting, rather than traditional GAAP methods. This subtle shift means the numbers in Item L of your document might diverge wildly from the economic reality reflected in the company's internal spreadsheets. And this divergence creates a hidden minefield for unsuspecting investors who mistakenly rely on the partnership's reporting to determine their actual tax exposure upon exiting the venture.

The netting strategy for multiple investments

When dealing with a sprawling portfolio of alternative assets, sophisticated investors employ a legal netting methodology to maximize efficiency. If you hold three separate real estate partnerships, you can aggregate the passive income from one to absorb the suspended passive losses of another, provided you file the appropriate grouping election under Section 469. As a result: an otherwise useless paper loss transforms into an immediate tax shield. Yet, executing this maneuver requires pristine synchronization because once you group these activities together, the IRS binds you to that decision for all subsequent years, limiting your future flexibility when you eventually liquidate a single entity.

Frequently Asked Questions

What should I do if my Schedule K-1 is delayed past the April filing deadline?

Partnerships and S-corporations routinely leverage their automatic six-month extensions, frequently delaying the release of these critical documents until September or October. You must file Form 4868 by April 15 to extend your personal filing deadline to October 15, preventing late-filing penalties. However, an extension to file is never an extension to pay. You are required to estimate your potential pass-through income using the prior year's data or quarterly statements, then submit a safe-harbor payment representing at least 110 percent of your previous year liability if your adjusted gross income exceeds $150,000. Failure to make this proactive payment results in failure-to-pay penalties accumulating at a rate of 0.5 percent per month on the unpaid balance.

How do I handle state tax filings when the partnership operates in multiple regions?

When a business generates revenue across state lines, you inherit a fractional tax obligation in every single jurisdiction where that entity established economic nexus. Box 13 or specific state supplements will disclose your portion of sourced income for states like California, New York, or Ohio. Many partnerships offer a composite return option, allowing the entity to pay the individual state taxes on your behalf at the highest marginal rate, which simplifies your life but usually costs you more money. If you decline the composite filing, you must prepare non-resident individual returns for each state, though your home state will typically grant a tax credit for taxes paid to other jurisdictions to mitigate double taxation.

Can I use a standard tax software package to report K-1 on my tax return accurately?

Basic or intermediate online tax software tiers completely lack the complex algorithms required to process the intricate supplementary schedules attached to pass-through documents. You will need to purchase the premium, self-employed, or desktop investor versions of the software to unlock the entry screens for Part III lines, especially concerning Section 199A qualified business income components. (Even then, the automated interview flows often fail to properly capture specialized information like oil and gas depletion or foreign transaction details on Schedule K-3). For investors holding complex real estate syndications or hedge fund allocations, bypassing the software entirely and hiring a specialized Certified Public Accountant remains the only reliable mechanism to prevent devastating processing delays.

Engaged synthesis

The modern tax landscape treats pass-through entities with an extraordinary level of bureaucratic scrutiny, turning what should be a simple reporting task into an administrative nightmare. Navigating this process demands that you discard the dangerous illusion that tax preparation is a passive, automated exercise easily solved by consumer software. The reality dictates that you take an aggressive, defensive posture toward your investments by tracking your own outside basis from day one. Relying solely on the partnership’s internal accounting to protect your financial interests is a recipe for an expensive IRS dispute. In short, mastering the nuances of pass-through reporting is the ultimate boundary line separating casual hobbyist investors from sophisticated wealth builders who understand the true cost of compliance.