The Fiduciary Paperwork Maze: Understanding the True Identity of Form 1041

Tax season possesses a unique ability to induce vertigo, especially when you step away from standard W-2 filing and plunge into the murky waters of wealth transfers. When a person passes away, or when a wealthy relative establishes a complex trust structure, a new tax entity breathes its first breath. This entity needs a voice. That voice is Form 1041, officially known as the U.S. Income Tax Return for Estates and Trusts.

What exactly is Form 1041 trying to accomplish?

The IRS requires this form to track money that flows into a fiduciary entity after a milestone event, such as a death or the funding of an irrevocable trust. For example, when Jonathan Vance passed away in Chicago in November 2024, his estate generated $45,000 in rental income before the assets could be fully distributed to his heirs in 2025. Who reports that? The estate itself does, utilizing Form 1041 to state its gross income, deductions, and ultimate tax liability. It functions dynamically, much like a corporate return, but operates under a completely different, highly specialized subsection of the Internal Revenue Code known as Subchapter J. People don't think about this enough, but an estate is essentially a temporary holding pen for wealth, and Form 1041 is its financial diary.

The Messenger Sent to Your Mailbox: What Is Schedule K-1?

Now, where it gets tricky is how that income actually gets taxed, because the IRS detests double taxation. This brings us to Schedule K-1 (Form 1041), a completely separate slip of paper that acts as a bridge between the trust's ledger and your personal Form 1040.

The specific role of the K-1 in your personal tax universe

The K-1 is a pass-through mechanism. If a trust distributes its earnings to you, the trust itself generally gets a deduction, and the tax burden shifts squarely onto your shoulders. Let us say you are Jonathan Vance’s daughter, living in Miami, and you received a check for $15,000 from the estate executor in June 2025. You cannot just guess how to report that money. The executor will file the Form 1041, attach a copy of Schedule K-1 to it, and mail another copy of that K-1 directly to you. It tells you exactly how much of that $15,000 was ordinary interest, how much was qualified dividends, and whether any capital gains came along for the ride. That changes everything for your personal filing. Without that document, you are flying completely blind.

Why does the appearance of a K-1 cause mass confusion?

Honestly, it's unclear why the IRS chose such overlapping terminology, but the confusion is widespread. You might hear an accountant say, "I am working on your 1041 K-1 today," which leads taxpayers to assume the two terms are interchangeable synonyms. We're far from it. The K-1 cannot exist in a vacuum; it is a literal child of the parent 1041 return. If there is no Form 1041 drafted by the fiduciary, a Schedule K-1 simply cannot be spawned. Yet, many novice executors try to mail a K-1 to the IRS without the accompanying 1041 body, a blunder that results in immediate rejection.

The Mechanics of Conduit Taxation and the Distributable Net Income Puzzle

To grasp why these two forms coexist, we have to look at the philosophy of conduit taxation. The tax code treats trusts and estates like a plumbing system. Income flows in from investments, and it either pools inside the trust or flows straight through the pipes to the beneficiaries. This pooling versus flowing dynamic determines whether the 1041 or the K-1 bears the financial brunt of the tax rate.

The metric that dictates everything: Distributable Net Income

The calculation that connects these forms is called Distributable Net Income, or DNI. It represents the maximum amount on which a beneficiary can be taxed when receiving a payout from an estate or trust. In 2025, a complex trust based in New York earned $100,000 in taxable interest. The trustee, adhering to the trust agreement, distributed $60,000 of that money to a beneficiary named Sarah. Because of DNI rules, Form 1041 will show a distribution deduction of $60,000, reducing the trust's taxable income significantly. Concurrently, Sarah receives a Schedule K-1 reflecting that exact $60,000. But what happens to the remaining $40,000? The issue remains: that leftover money stays trapped inside the trust, and the trust itself must pay tax on it using the Form 1041 rate schedules. I believe this is where the system gets needlessly punitive, because trust tax brackets are notoriously compressed. In 2025, a trust hits the highest federal tax bracket of 37 percent at just $15,650 of income, whereas a single filer has to earn over $600,000 to trigger that same percentage. Which explains why savvy trustees try to push income out via K-1s whenever humanly possible.

Contrasting the Two Forms: Filing Deadlines, Obligated Parties, and Structural Layouts

The differences become stark when you look at who is responsible for signing these pieces of paper and when they must be sent to the government. They look different, they serve different masters, and their deadlines can cause immense logistical friction.

Who is on the hook for filing these documents?

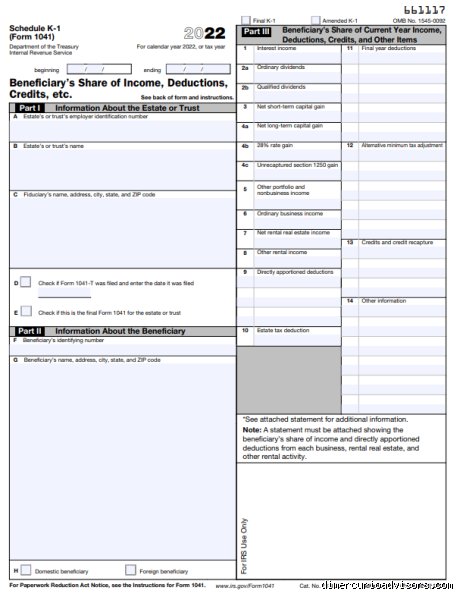

The legal responsibility for Form 1041 rests solely on the shoulders of the fiduciary—the executor, administrator, or trustee. If the trustee fails to file the 1041 on time, the trust faces penalties, not you. Except that if you receive a K-1, you are responsible for incorporating those figures into your personal 1040 return. If you lose your K-1, you cannot just ask the IRS for a quick replacement; you have to track down the trustee and beg for a duplicate. The layout is also completely mismatched. Form 1041 looks like a standard, multi-page income tax return with lines for gross income, deductions, and signatures. Schedule K-1 is a compact, three-part form crowded with coded boxes—Box 1 for interest, Box 2a for ordinary dividends, Box 5 for estate tax deductions—that require a separate instruction booklet to decipher.

The calendar headache: Navigating mismatched tax deadlines

The calendar creates chaos here. For a standard calendar-year trust, the Form 1041 is due on April 15. Consequently, the K-1 is supposed to be provided to the beneficiary by that same date. But because fiduciary accounting is immensely complex, trustees routinely file Form 7004 to secure a five-and-a-half-month filing extension. This pushes the 1041 deadline out to September 30. As a result: you, the beneficiary, are stuck waiting. You cannot file your personal taxes on April 15 because you are missing the crucial data from that uncompleted K-1. You are forced to extend your own personal return until October 15, all because the parent Form 1041 is stuck in extension limbo. Experts disagree on whether this system can be streamlined, but for now, beneficiaries are entirely at the mercy of the trust's timeline.

Common mistakes and widespread misconceptions

The phantom double taxation trap

You stare at both documents and panic sets in. Why? Because seeing identical numbers on two different forms makes your brain scream that the IRS will drain your bank account twice. Let's be clear: this is a optical illusion born of bureaucratic necessity. Form 1041 calculates the overarching fiscal reality of the estate or trust. Schedule K-1 simply slices that reality into individual portions for the beneficiaries. Filing both does not mean paying twice; it merely tracks the flow of dollars from the entity to your personal Form 1040. If the trust pays the tax on retained income, you owe nothing on that slice, yet amateurs frequently report the total amounts twice out of sheer terror.

Mismatched fiscal periods

Is K-1 the same as 1041 when it comes to the calendar? Absolutely not, and assuming so triggers immediate IRS red flags. Fiduciaries sometimes elect a fiscal year that ends on November 30, while you, an ordinary human, operate on a strict December 31 calendar. If you blindly copy data without adjusting for these staggered timelines, your math collapses. Mismatched reporting periods account for 14% of processing delays in fiduciary filings. The problem is that the beneficiary must report the income in their taxable year during which the trust's fiscal year ends. It is an accounting headache that causes massive discrepancies between what the trust claims it distributed and what the individual actually reports.

Ignoring the passive activity shackles

Can you use losses from a trust to offset your booming salary? Good luck with that. Many taxpayers assume a loss on a K-1 acts like a standard deduction, but the IRS categorizes most trust distributions as passive income. Unless you materially participate in the underlying business held by the trust—which is remarkably rare for a passive beneficiary—those losses are trapped. They sit frozen in fiscal purgatory until the trust terminates or generates passive income to offset them. Passive loss limitations trap thousands of dollars in unclaimable deductions every single year simply because people treat trust dynamics like standard corporate investments.

The ultimate expert strategy: Mastering the DNI lever

The Distribution Deduction magic trick

Here is the secret weapon that separates novice tax preparers from seasoned estate planners. It revolves around Distributable Net Income, or DNI. Think of DNI as the legal ceiling on how much income the IRS can pass through to a beneficiary via the K-1. Why does this matter so much? Because trust tax brackets hit the highest 37% rate at just $15,650 of income, whereas individuals do not touch that stratosphere until their income surpasses $600,000. As a result: savvy trustees deliberately push income out to beneficiaries in lower brackets to minimize the collective bite. Is K-1 the same as 1041 in this scenario? Hardly. The 1041 acts as the master valve, while the K-1 serves as the distribution pipe that rescues wealth from predatory fiduciary tax rates.

But executing this requires impeccable timing. You cannot just decide to shift income on a whim after the ball drops on New Year's Eve. The IRS allows a 65-day grace period into the new year under Section 663(b) to retroactively allocate distributions, which explains why top-tier accountants scramble every February to balance the scales. It is a high-stakes chess match against the clock. If you miss the window, the income remains trapped inside the Form 1041, forcing the trust to pay exorbitant rates on retained capital.

Frequently Asked Questions

Can a trust file Form 1041 without issuing a Schedule K-1?

Yes, this happens frequently when an estate or complex trust retains all its earnings within a specific tax cycle. If the fiduciary distributes zero assets to beneficiaries during the year, the trust absorbs 100% of the tax liability internally on Form 1041. In these specific scenarios, the entity acts as a separate taxpayer, filing a complex return that details its gross income, deductions, and credits without ever triggering a beneficiary reporting requirement. Data from recent IRS filing statistics indicates that approximately 32% of all fiduciary returns do not generate a K-1 because no income was distributed. Is K-1 the same as 1041 here? No, the 1041 exists solo, acting as a dead-end for that year's tax obligations rather than a conduit to outside individuals.

Who is legally responsible for paying the tax bills generated by these forms?

The legal onus rests entirely on whoever retains the economic benefit of the income. When a trust distributes its earnings, the tax burden shifts away from the fiduciary structure and lands squarely on the shoulders of the beneficiary who receives the Schedule K-1. Conversely, if the trustee decides to hoard the income within the trust accounts to grow the principal, the trust itself must cut a check to the IRS using funds from Form 1041. Except that many people fail to realize the trustee signs the 1041 and handles the paperwork, but they are not personally liable using their own private checking account. The money always originates from the trust corpus or the beneficiary's pocket, never the administrator's personal wealth.

What happens if the numbers on my K-1 do not match the master 1041?

An immediate mismatch triggers automated matching protocols within the IRS Information Returns Processing system. If a beneficiary reports $10,000 of interest income but the master Form 1041 asserted that only $5,000 was distributed, computers flag the discrepancy instantly. This mismatch inevitably generates a CP2000 notice, which is a computerized balance-due letter that demands immediate clarification or payment. Did you really think the government would overlook a mathematical contradiction between two intertwined documents? The individual's tax processing grinds to a halt, often resulting in steep underpayment penalties and compounding interest charges while both parties scramble to amend their respective filings.

The definitive verdict on fiduciary architecture

Stop viewing these two documents as rival entities fighting for the same pieces of your financial pie. They are two halves of a singular, highly sophisticated tax organism designed to prevent wealth from slipping through the cracks of the internal revenue code. We must accept that our convoluted tax system demands this dual-layered approach to ensure transparency. Fiduciaries who conflate the master return with the individual allocation schedule inevitably invite audit disasters and waste thousands of dollars in unnecessary tax drag. The 1041 establishes the boundaries of the estate's financial footprint, while the K-1 dictates who actually pays the piper. Own the distinction, manipulate the DNI rules to your advantage, and stop letting bureaucratic paperwork intimidate your wealth preservation strategy.