The Messy Reality Behind Financial Categorization: Why Your Bank Statement Looks the Way It Does

Let’s be real for a moment. The financial sector loves to invent arbitrary names for things that are fundamentally just digital ledgers holding your hard-earned cash. Walk into a branch of Chase in downtown Chicago or open an app based in Silicon Valley, and you will be bombarded with marketing jargon masquerading as financial innovation. The thing is, beneath the slick user interfaces, the banking system relies on century-old architecture designed to segment capital based on how fast you need to move it.

The Liquidity Spectrum: From Cold Hard Cash to Locked-Up Capital

Money is not static, or at least, it shouldn't be. Experts disagree on the exact threshold of optimal liquidity, but the core tension always lies between accessibility and yield. If you can swipe a plastic card at a grocery store and instantly transfer value, you are operating on one end of this spectrum. But lock that money into an account that penalizes you for early withdrawal—and suddenly you’re playing a completely different game where the rules favor the institution rather than your immediate survival needs.

Velocity Over Volume

Where it gets tricky is assuming that a high balance in a single account signals financial health. It doesn't. A 2024 Federal Reserve study indicated that holding excessive cash in transactional buckets costs consumers billions annually in lost opportunity. Because inflation acts as a silent tax, keeping your wealth stagnant is a losing proposition, which explains why savvy navigators split their reserves across distinct financial instruments rather than hoarding it under one digital roof.

The Everyday Engine: Unpacking the Transactional Power of Checking Accounts

The checking account is the undisputed workhorse of modern existence. You cannot survive in a cashless economy without one. It is the primary landing pad for your employer’s direct deposit and the launchpad for your recurring monthly bills. But because it sits on the frontline of your daily financial life, it is also the most exposed to institutional friction.

High Volume, Low Friction, Zero Yield

You use it constantly, yet it gives back absolutely nothing. Data from the FDIC in late 2025 showed the average national checking interest rate hovering at a pathetic 0.07%, a figure that makes traditional hoarding look almost competitive. It’s designed for velocity. You want money in, money out, with instant settlement mechanisms like Zelle or debit networks processing your morning coffee run without a hitch. And yet, we tolerate this lack of growth because the utility of immediate access is unmatched. That changes everything when you realize your checking account is a logistical tool, not a wealth-building one.

The Trap of Institutional Fees

But the issue remains that banks make an absolute killing on these accounts through maintenance fees and overdraft penalties. If your balance dips below a specific threshold—say, $1,500 at a legacy institution—you are slapped with a monthly penalty that quietly bleeds your reserves. People don't think about this enough, but you are essentially paying a corporation to let them lend out your money to other borrowers overnight. It’s a brilliant business model for them, but a raw deal for you unless you navigate the fine print with extreme paranoia.

The Vault Concept: How Savings and Money Market Accounts Protect Against Economic Erosion

If checking accounts represent movement, savings and money market accounts are meant to represent stability. This is where you park your emergency fund—ideally three to six months of living expenses—to protect your household from sudden macroeconomic shocks.

The High-Yield Evolution

Traditional savings accounts offered by brick-and-mortar institutions are a joke, frequently paying the same insultingly low rates as checking products. Except that the digital banking revolution completely disrupted this landscape. Online-only entities, unburdened by the immense overhead of physical real estate in places like Manhattan or San Francisco, started offering High-Yield Savings Accounts (HYSAs) that paid significantly more. Suddenly, consumers were seeing returns climb past 4% or 5% during aggressive Federal Reserve rate hike cycles. It proved that geographical loyalty to your local bank branch is an expensive habit you need to break.

Money Market Accounts: The Hybrid Alternative

Then we have the Money Market Account (MMA), which occupies a strange, twilight zone between saving and checking. It behaves like a savings vehicle because it offers competitive interest rates, but it frequently comes with limited check-writing privileges or a debit card. Hence, it offers a bit more flexibility. But do not confuse these with Money Market Funds offered by brokerages; these are bank deposits backed by the Federal Deposit Insurance Corporation (FDIC) up to $250,000, meaning your principal is safe even if the broader stock market enters a terrifying tailspin.

Beyond Savings: The High-Stakes Arena of Investment and Brokerage Accounts

To truly build generational wealth, you have to cross the rubicon from saving to investing. This is where brokerage accounts and retirement vehicles come into play, shifting your financial strategy from defensive preservation to aggressive growth. We are far from the safety of FDIC insurance here; this is where you embrace volatility in exchange for historical upward trajectories.

Tax-Advantaged Versus Taxable Accounts

This is where the strategy requires sharp precision. A standard taxable brokerage account lets you buy stocks, bonds, and mutual funds whenever you want, with no limits on how much you can inject into the market. But Uncle Sam will demand his cut every time you realize a gain or receive a dividend. On the flip side, retirement vehicles like a Traditional 401(k) or a Roth IRA offer massive tax advantages. With a Roth setup, you invest after-tax dollars today, but your capital grows completely tax-free, allowing you to withdraw wealth in your golden years without owing the IRS a single dime. Because who honestly wants to hand over twenty percent of their retirement nest egg to the government if they don't have to?

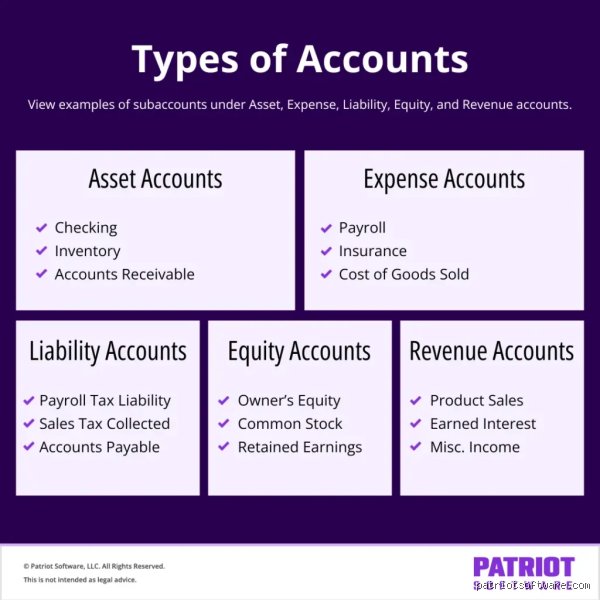

Common Misconceptions Surrounding the Four Pillars of Ledger Architecture

Most corporate treasurers nod along when discussing basic accounting structures, assuming the definitions are set in stone. The problem is, they usually conflate liquidity tracking with genuine value generation. Let's be clear: confusing an expense account with an asset acquisition is the fastest way to trigger a devastating audit flag.

The Dangerous Mirage of Cash Flow as Income

Revenue does not equal cash in the bank. Startups frequently commit this cardinal sin because their billing software registers an invoice as immediate wealth. Except that, under accrual rules, that unpaid invoice sits in accounts receivable—an asset, not income. If your client files for bankruptcy before settling that $45,000 balance, your projected earnings vanish instantly. Accrual accounting mechanics demand absolute separation between realized cash and recognized revenue, a distinction that amateur bookkeepers regularly obliterate during quarterly Closings.

Misclassifying Liabilities as Operational Costs

When you sign a three-year lease on an enterprise server array, where does that transaction live? Many founders dump the monthly installments directly into the operating expense column. Wrong. Modern frameworks require you to recognize the present value of that long-term commitment as a robust liability. Treating it as a mere recurring utility bill fundamentally distorts your debt-to-equity ratio. Why does this matter? It matters because savvy venture capitalists will dissect your balance sheet and spot the hidden leverage immediately, which explains why so many seed-stage funding rounds collapse during due diligence.

The Hidden Velocity of Capital: Expert Structural Insights

Understanding the basic definitions of what are the four different types of accounts is just entry-level compliance. The real mastery lies in optimizing the interaction between these distinct categories to engineer artificial tax advantages and optimize cash utilization strategies.

Exploiting Contra Accounts for Asset Valuation Accuracy

You cannot simply adjust the primary value of a corporate vehicle or building when depreciation hits. Enter the contra account. This specialized sub-category acts as a financial shadow, accumulating negative value right next to the original asset. By maintaining the historical purchase price of $120,000 for manufacturing hardware while simultaneously tracking $40,000 in accumulated depreciation, you present a transparent window into your operational reality. It reveals exactly how much production life your machinery has left before requiring a massive capital injection. (Smart CFOs use this exact friction point to negotiate lower property tax assessments with local municipalities).

Frequently Asked Questions

How do international financial reporting standards modify what are the four different types of accounts compared to domestic GAAP?

The core divergence rests on the strict permissibility of asset revaluation models across different jurisdictions. Under domestic GAAP rules, historical cost remains absolute, meaning a commercial property purchased for $2.4 million in 1998 cannot be arbitrarily adjusted upward on the balance sheet despite skyrocketing market values. International frameworks, however, allow corporations to revalue those exact holdings to reflect a current fair value of $7.1 million, directly inflating the equity section. This single regulatory pivot shifts debt-to-equity metrics by as much as 35% for multinational enterprises. As a result: cross-border mergers require extensive reconciliation templates just to normalize basic balance sheet health before any acquisition can legally proceed.

Can a single transaction simultaneously trigger an increase in both asset and liability categories?

Absolutely, because double-entry book-keeping dictates that every financial event must possess an equal and opposite balancing entry. When an expanding logistics enterprise purchases a new delivery fleet valued at $850,000 using an institutional bank loan, the physical vehicles immediately expand the equipment asset ledger. Simultaneously, the signed promissory note creates a matching obligation within the long-term debt liabilities column. The net effect on the overarching corporate net worth remains completely neutral at the exact moment of execution. Yet, the broader operational capacity of the business scales instantly, proving that debt utilization is the primary engine behind aggressive corporate expansion strategies.

Why do temporary expense summaries need to reset to zero at the conclusion of every fiscal cycle?

Did you ever wonder why your net income figure does not continuously accumulate year after year like a savings account? Income statement components are inherently ephemeral, designed exclusively to measure operational velocity over a predefined 365-day window. If we allowed last year's $500,000 marketing expenditures to linger in the active ledger, calculating current-year profitability would become an impossible nightmare. Bookkeepers must execute closing entries that forcefully migrate those balances into the retained earnings section of the permanent equity ledger. In short, this annual flushing mechanism resets the operational scoreboard, ensuring that the new fiscal year begins with a pristine canvas for performance evaluation.

A Definitive Verdict on Modern Financial Architecture

Relying on software automation to sort your transactional data is a recipe for systemic corporate blindness. The traditional categorization frameworks are not historical relics to be managed by cheap algorithms; they represent the literal nervous system of your business. We spend far too much time obsessing over real-time revenue dashboards while ignoring the slow-moving liabilities that actually sink modern enterprises. A business can survive years of erratic profitability, but it will collapse in forty-eight hours if the structural integrity of its ledger architecture fails to mirror reality. True financial leadership means treating these accounts as active strategic levers rather than passive compliance buckets.