The Hidden Friction of Instant Liquidity and Why True Speed Costs Money

Let's be real for a second. The internet is absolutely plagued with listicles promising easy money, yet they conveniently omit the fact that a standard ACH transfer takes three business days. That changes everything when your bank account is sitting at negative twelve dollars on a Tuesday night. The thing is, when we talk about how to get $50 immediately, we are actually discussing the monetization of urgency. Fintech companies know you are in a tight spot. Because of this, true instant gratification almost always comes with a small, annoying convenience fee—usually a flat $2.99 to $4.99 for immediate debit card disbursement.

The Disconnect Between Earning and Payout Speed

You can spend four hours taking mind-numbing surveys on a random platform, but if their minimum cash-out threshold is twenty bucks and they only process payments on the first of the month, you are still broke today. It is an exhausting trap. This discrepancy between the time you invest and the actual movement of data across the banking ledger is where most people get tripped up. Why do we still tolerate processing delays in an era of instant global communication? Honestly, it’s unclear. Experts disagree on whether banks are just lazy or if they profit off the float, but the issue remains: speed is a premium feature, not a default setting.

The Psychology of the Micro-Cash Crunch

Desperation makes people sloppy. When you are frantically typing queries into a search engine at midnight, you become prime real estate for predatory payday lenders or sketchy applications that harvest your contacts. I have analyzed dozens of these fast-cash schemes, and my sharpest opinion is that 90% of them should be avoided like the plague. Except that sometimes, you just need to put gas in the tank to get to work tomorrow. Nuance dictates that we acknowledge the utility of these modern financial bridge tools, even if they charge an APR that would make a traditional banker wince.

Fintech Cash Advances: Borrowing From Your Future Self Instantly

This is where the landscape gets incredibly fascinating for anyone tracking how to get $50 immediately without begging friends. Over the last few years, app-based cash advances have completely cannibalized the traditional storefront lender market. If you have a steady paycheck and a checking account with a positive history, apps like Chime or Dave will literally hand you fifty bucks within five minutes. They do not run a traditional hard credit check through Experian, which is a massive relief for anyone whose credit score has taken a beating recently.

How the Chime SpotMe Mechanism Operates in Real Time

Take Chime's SpotMe feature, for example. It is not technically a loan; it is an fee-free overdraft protection system that lets you overdraw your account at the cash register or ATM. If your account qualifies based on a history of at least $200 in monthly direct deposits, they will instantly boost your spending power. You walk into a CVS, buy a pack of gum, and ask for fifty dollars cash back. Boom. Done. The system automatically reconciles the negative balance the very second your next paycheck lands, making it a frictionless, albeit cyclical, way to manage sudden financial speedbumps.

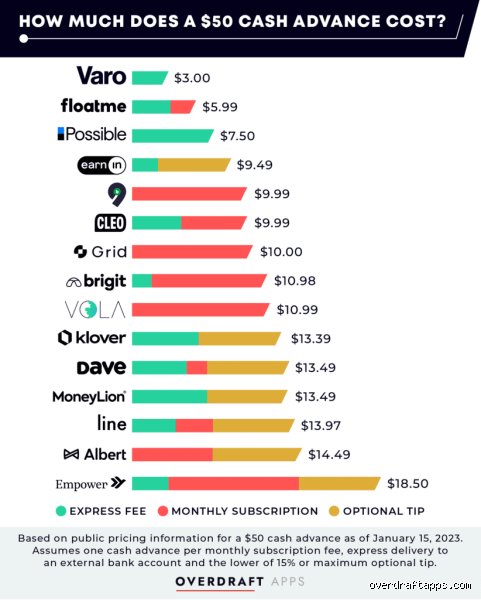

Navigating the Small Print of Instant Transfer Fees

But here is where it gets tricky. If you do not have their proprietary debit card or you need the money moved to an external account right this second, you are going to pay the "express fee" tax. Is a five-dollar fee on a fifty-dollar advance steep? Absolutely—that is technically a 10% interest rate for a transaction that might only last four days. Yet, compared to a standard bank overdraft fee, which currently averages a brutal $35 per occurrence across major US institutions, paying four bucks to get your hands on fifty is actually the cheaper financial decision. As a result: you save thirty dollars by willingly paying a premium for speed.

Rapid Monetization of Underutilized Digital Assets

If you do not want to borrow against your next paycheck, your next best bet involves hunting through your digital junk drawer. People don't think about this enough, but the average American household sits on roughly $21 billion in unredeemed gift cards and loyalty points. That old Starbucks or Walmart card you got from your aunt two Christmases ago is literally sitting there acting as a zero-interest loan to a mega-corporation while you are scrambling for grocery money.

The Digital Secondary Market for Gift Cards

Platforms like Raise or CardCash allow you to flip these unused balances for immediate digital cash. You simply type in the serial number and PIN, the platform instantly verifies the balance via an automated API call, and they offer you a wholesale price—usually between 70% to 85% of the face value. If you have a seventy-dollar gift card, you can walk away with fifty dollars in your PayPal account within roughly twenty minutes. It hurts a bit to lose that percentage of the value, but we are far from having the luxury of patience right now.

Immediate Peer-to-Peer Marketplaces and Hyper-Local Labor

When algorithmic options fail, you have to pivot to human networks. The fastest way to get fifty bucks from another human being without borrowing it is to solve an immediate, highly localized problem. Forget applying for a job on a corporate portal; we are talking about digital gig boards where the transaction happens entirely on the sidewalk.

The Facebook Marketplace Quick-Sale Strategy

Do you have an old video game, a functional microwave, or a pair of sneakers you barely wear? List it on Facebook

Common traps and myths about fast liquidity

The instant-payout illusion

You see the glittering banners everywhere promising $50 immediately without any human interaction. Let's be clear: genuine instantaneous processing is a mechanical rarity because automated clearing houses require verification windows. Most applications that advertise immediate distribution actually hold your funds in a pending status for twenty-four to forty-eight hours unless you forfeit an outrageous tier of processing fees. Some platforms siphon off up to 10% of your requested balance just to fast-track the deposit. If you surrender three to five dollars of your fifty-dollar target just for expedited processing, your effective annualized interest rate skyrockets into the triple digits. The problem is that desperation blinds us to these micro-transactions.

The predatory payday trap

Why do people fall for localized cash advance kiosks when trying to figure out how to get $50 immediately? Because they perceive micro-loans as harmless bridge financing. Except that the mathematical reality of these operations relies entirely on your failure to repay the capital within the standard fourteen-day cycle. A seemingly benign fifty-dollar advance can mutate into a multi-headed debt monster if regional regulations allow triple-digit annual percentage rates. According to data tracking consumer lending behavior, over 80% of payday loans are rolled over or followed by another loan within a single month. You are not solving a liquidity crunch this way; you are merely renting expensive capital that compromises your next paycheck.

The online survey delusion

Do you honestly believe completing digital questionnaires will yield rapid, spendable currency before sunset? The internet loves promoting survey aggregators as the ultimate remedy for financial shortfalls, yet the actual mechanics of these platforms tell a vastly different story. Most panels implement mandatory minimum cash-out thresholds that sit stubbornly at twenty-five or fifty dollars. You might spend six exhausting hours answering demographic queries only to discover you have accumulated nine dollars in unredeemable tokens. It is an algorithmic hamster wheel where the system disqualifies you halfway through a study, ensuring you never actually cross the payout finish line.

The hidden leverage of unbundled asset liquidation

Fractional secondary markets

If you need a rapid influx of capital, stop looking at your traditional checking account and start analyzing your digital footprint. Every modern household possesses a fragmented portfolio of unused digital gift