It happened to a colleague of mine in Chicago back in October 2024; a single leaked PDF from a routine dental appointment ended up funding a three-bedroom apartment lease in Phoenix. He had no clue until the eviction notice hit his actual mailbox. Identity theft is no longer just about a stolen credit card number being used for a quick electronics spree before the fraud department freezes the account. No, the modern ecosystem of data brokers and dark web marketplaces has turned personal info into a slow-burn commodity. Which explains why the average victim takes more than eighteen months to even realize their data has been weaponized by a stranger thousands of miles away.

The Evolution of Synthetic Identity Theft and Why You are Looking in the Wrong Places

The landscape of digital fraud has shifted beneath our feet. We used to worry about pickpockets or skimmers at the gas station pump, yet today the threat is entirely abstract. Criminals do not just steal your persona anymore—they build entirely new, Frankenstein-like configurations known as synthetic identities using your genuine Social Security number combined with a completely fabricated name and address. Because these ghosts do not trigger traditional banking alerts, they can operate undetected for years.

The Anatomy of a Ghost Profile

Where it gets tricky is the credit bureaus themselves. Equifax, Experian, and TransUnion create a new "sub-file" when a lender inquiries about a name that does not match the SSN on file. This means a fraudster can open accounts under your SSN but using the name "John Smith," and it will not automatically show up on your standard credit report unless you specifically request a search for all names associated with your number. People don't think about this enough. It is a massive structural flaw in the global financial architecture, one that allows a parasite to drain credit capacity without ever triggering a flag on your phone.

The Statistical Reality of Digital Impersonation

The numbers are frankly staggering. According to the Identity Theft Resource Center, data breaches skyrocketed by 72% in recent years, eclipsing all previous historic highs. The Federal Trade Commission received over 1.1 million reports of identity theft in a single calendar year, with imposter scams topping the list of financial disasters. If you think your regional bank or local utility company is keeping your data safe under lock and key, we're far from it. Every single week, another legacy database gets dumped onto Telegram channels or public forums, making the question of how do I find out if my identity is being used a matter of "when," not "if."

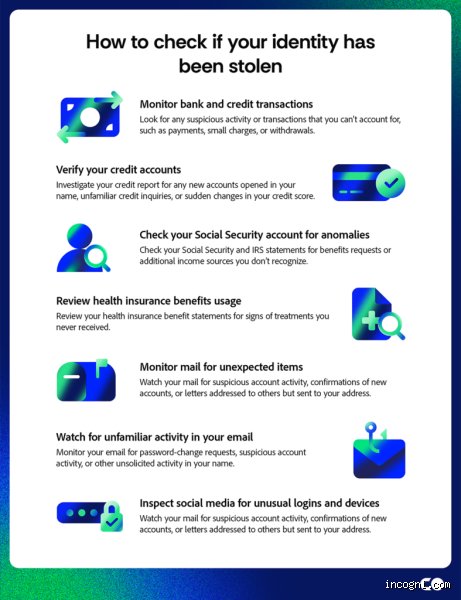

Unearthing the Evidence: The Primary Digital Registries You Must Audit Now

Do not wait for a court summons to start digging. The first line of defense is pulling your reports from the big three credit bureaus, but honestly, it's unclear why everyone stops there when the most damaging fraud happens entirely outside the traditional banking system. You need to look at the specialized consumer reporting agencies that track things you probably did not even know were being tracked.

The Bureaucratic Paper Trail Most People Ignore

Start with the Annual Credit Report service, which is legally mandated to provide free documents. But here is the thing: you must look at the "soft inquiries" section at the bottom of the page. These are the footprints left by insurance companies, employers, and payday loan outfits checking your background. Did a car dealership in Ohio look at your file last November? If you live in Seattle and have not bought a car since 2021, that changes everything. It is the smoking gun of a compromised profile.

The Secret Databases: ChexSystems and LexisNexis

Next up is ChexSystems. Think of it as the blacklist database that banks use to track bounced checks, closed accounts, and suspected fraud. If a criminal opens a fraudulent checking account in your name to launder money or cash bad checks, it won't show up on a standard Experian report—except that it will be logged instantly in ChexSystems. You must request your Consumer Disclosure Report from them annually. Furthermore, requesting your Full File Disclosure from LexisNexis will reveal a terrifyingly detailed history of every address, phone number, and piece of real estate ever linked to your name, allowing you to spot anomalies before they mutate into legal nightmares.

Advanced Identification: Tracking Medical and Government Imperialism

Medical identity theft is arguably the most dangerous variant of this crime because it does not just destroy your finances; it alters your actual medical records. If an impostor uses your health insurance to undergo surgery or obtain prescription narcotics, their blood type, allergies, and diagnoses can get permanently spliced into your charts.

Decoding the Explanation of Benefits

How do you spot this? You have to read every single Explanation of Benefits statement sent by your insurer. Every time you see a line item for a clinic you have never visited or a doctor you have never heard of, you need to treat it like an active crime scene. A bizarre bill from a radiology lab in Miami when you have never left New England is not a clerical error. The issue remains that hospital billing departments are notoriously disorganized, which explains why victims often dismiss these warning signs as simple administrative noise until collection agencies start calling.

The Social Security Administration Blind Spot

And then there is the tax angle. Log into your mySocialSecurity account on the official government portal. Check your earnings history column by column. If the database shows you earned $85,000 in employment income from a logistics company in Texas last year—but you actually work as a graphic designer in Maine—someone is using your SSN for employment verification purposes. As a result: you will likely face a massive, terrifying tax bill from the IRS for unreported income that you never actually received.

Comparing Self-Auditing Versus Automated Identity Monitoring Services

The market is flooded with heavily advertised subscription services promising to protect your digital footprint for twenty dollars a month. But do these platforms actually provide real protection, or are they just selling a false sense of security to anxious consumers?

The Illusion of the All-Seeing Eye

Most commercial monitoring services do nothing more than automate the exact steps detailed above. They ping the credit bureaus, scan public court records, and scrape known dark web marketplaces for your email address or password. Yet, experts disagree on their efficacy. While they are convenient for busy people, they often suffer from a severe time lag. A monitoring service might alert you three weeks after a fraudulent account has been opened—but by then, the credit line has already been maxed out and sold to a secondary collector. Manual vigilance remains far more precise because you can spot nuanced inconsistencies that a generalized algorithm completely misses. In short, paying for a service does not absolve you from the responsibility of checking your own government accounts.

Common Myths and Misconceptions About Identity Theft

Most people assume a clean credit report means they are completely safe. It does not. The problem is that traditional credit monitoring only tracks financial institutions, completely ignoring medical fraud, criminal record cloning, and synthetic identity construction. Synthetic identity theft occurs when a criminal combines a real, stolen Social Security number with fake names and addresses to build an entirely new persona. Because the perpetrator is not opening accounts in your exact name, standard credit alerts remain eerily silent while debt accumulates under your government identifier. Why do we keep falling for the illusion of total digital security?

The Fallacy of the Instant Notification

Waiting for a magical text message from your bank telling you that your data is compromised is a dangerous strategy. Hackers routinely purchase compromised credentials on the dark web but sit on them for months, even years, waiting for the perfect moment to exploit the data. But you cannot rely on automated systems alone. A 2024 security study revealed that 42% of identity fraud victims only discovered the breach themselves through manual statement audits or when denied a legitimate loan. Relying solely on passive alerts is like locking your front door but leaving the windows wide open.

The Micro-Transaction Blind Spot

Many consumers believe fraudsters only go after massive sums of money right away. Except that modern criminals actually prefer to test the waters with micro-transactions, often charging nominal amounts between $0.50 and $2.00 to see if an account is active. These tiny discrepancies are easily overlooked on busy monthly statements, yet they represent the precise mechanism used to validate stolen financial credentials. In short, ignoring a random two-dollar charge from an unknown digital merchant could mean handing over the keys to your entire financial livelihood.

The Hidden Threat of Synthetic Identity Creation

There is a darker, more sophisticated vector of fraud that rarely makes the evening news. Criminals are no longer just stealing your existing identity; they are stitching parts of it into completely new, fabricated profiles. Synthetic identity generation represents the fastest-growing type of financial crime in the modern era, accounting for billions of dollars in losses annually. By pairing a child’s unblemished Social Security number with a fictitious name and birthdate, fraudsters create an entirely fresh credit profile that can remain undetected for over a decade. Let's be clear: this is not a problem that a simple password change can fix.

Exploiting the Credit Invisible

Children, the elderly, and those without active credit histories are the primary targets for this particular scheme. The issue remains that these demographics rarely check their credit files, allowing criminals to nurture these fake profiles over several years to secure massive auto loans and credit lines. How do I find out if my identity is being used in a synthetic scheme? You must actively attempt to create an online credit bureau account for your minor children to see if a file already exists. (It should not, and if it does, it is an immediate red flag.) Vigilance requires digging into the dark corners of the financial system where automated alerts simply do not reach.

Frequently Asked Questions

How can I verify if someone is illegally using my Social Security number?

You can check your official earnings history annually by creating a personal account through the Social Security Administration website. If the recorded annual earnings listed on your statement are higher than what you actually earned, someone is likely using your credentials for employment purposes. According to recent federal statistics, employment-related fraud accounts for approximately 15% of all identity theft reports filed nationally. As a result: you must immediately file an Identity Theft Report with the FTC if you detect these specific discrepancies. Taking this step creates a legal paper trail that protects you from erroneous tax liabilities stemming from income you never actually received.

What are the immediate warning signs that my medical identity has been compromised?

Receiving bills for medical procedures, pharmaceutical prescriptions, or clinical devices you never received is the primary indicator of medical identity compromise. This happens because thieves use your health insurance information to receive expensive treatments, which can disastrously alter your real medical records with incorrect blood types or allergies. A disconcerting 21% of medical identity theft victims report receiving an unexpected collection agency notice before ever seeing an actual bill. You must demand an Accounting of Disclosures from your health provider to see exactly who has accessed your medical file. Resolving this requires contacting both your insurance provider and the specific medical facilities to correct the compromised records before life-threatening medical errors occur.

Can someone steal my identity using just my phone number and email address?

Yes, criminals use a technique known as SIM swapping to hijack your mobile phone number and bypass two-factor authentication codes. By convincing a telecom customer service representative that they are you, fraudsters port your number to a device under their control. Once they control the phone line, they can rapidly reset passwords across your entire digital footprint, including banking and investment accounts. Industry data indicates that SIM swapping attacks increased by over 70% in recent years, proving that basic contact information is highly weaponized. Which explains why relying on SMS-based verification codes is no longer considered a safe security posture for sensitive accounts.

A Definitive Verdict on Modern Identity Protection

The paradigm of waiting for a warning sign before investigating your digital footprint is officially obsolete. We live in an era where data breaches are an absolute certainty, not a statistical probability, meaning your personal data is likely already sitting in a malicious database. The burden of defense has shifted entirely onto the consumer, requiring an aggressive, proactive stance rather than passive reliance on corporate credit monitoring services. If you are not actively auditing your own financial, medical, and governmental records, you are essentially operating on borrowed time. True security requires accepting that the system is inherently broken and taking manual command of your digital sovereignty. Stop hoping for safety; actively demand it through relentless personal scrutiny.